Mainland Rebounds on Zero COVID Dial Back, Healthcare Equipment Loans Raise Sector

2 Min. Read Time

Key News

The US dollar’s parabolic rise has taken a breather, allowing some Asian markets to recover overnight. Mainland China rallied on explicit policy support for equity markets as well as positive signaling and discussion around a potential reopening.

Healthcare was a top performer in both Hong Kong and Mainland China. The National Health Commission announced that it would provide loans to hospitals for medical equipment upgrades.

There are reports that Mainland China may soon shorten the quarantine requirement for visitors, perhaps limited to visitors remaining in cities. Meanwhile, there is some speculation that the whole country will reopen in 2023 or even shortly after the party congress in August. This chatter may have contributed to the rebound in A shares overnight.

The People's Bank of China, China's central bank, injected $25 billion into the financial system through reverse repo operations, following a similar injection yesterday. On the flip side, the central bank also implemented a 20% risk-reserve ratio to help stem the fall of the Renminbi versus the US dollar. This makes it more expensive to sell yuan to buy dollar-based derivatives contracts. The PBOC is attempting to stimulate the economy while keeping the Yuan at a reasonable level versus the US dollar.

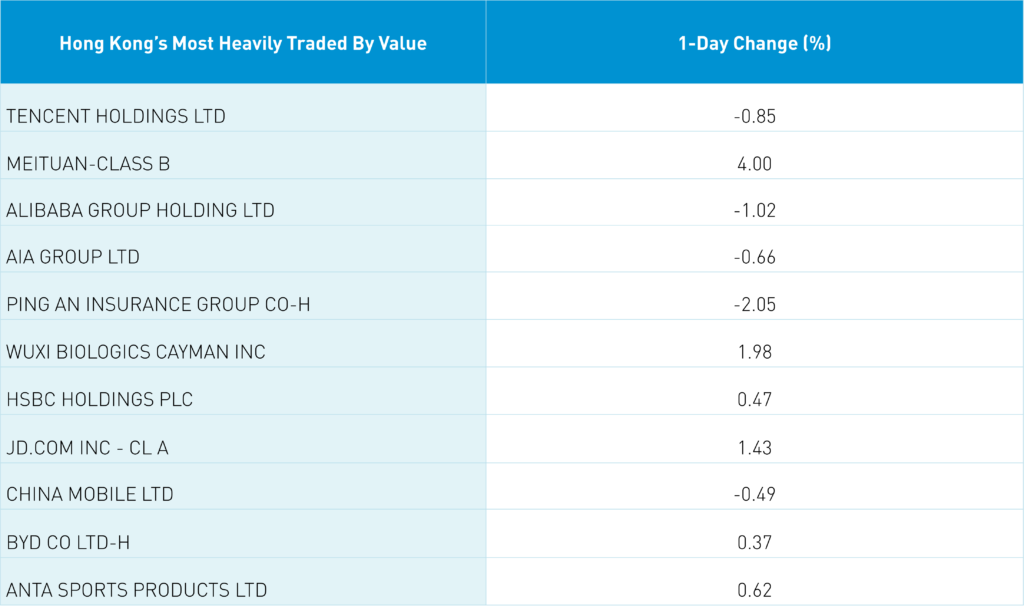

Internet names were mixed overnight on some profit taking, though Meituan and JD.com outperformed as short sale volume remains high. Privately held Tik Tok-owner Bytedance announced a share buy-back worth $3 billion. Alibaba Cloud established a partnership with a South African company to provide cloud computing services in that country. This comes as the Ministry of Commerce announced plans to support cross-border E-Commerce further.

Last night we saw the typical onshore versus offshore disparity as Mainland markets were up sharply while Hong Kong was up less than 1%. Growth stocks fared far better on the Mainland as well.

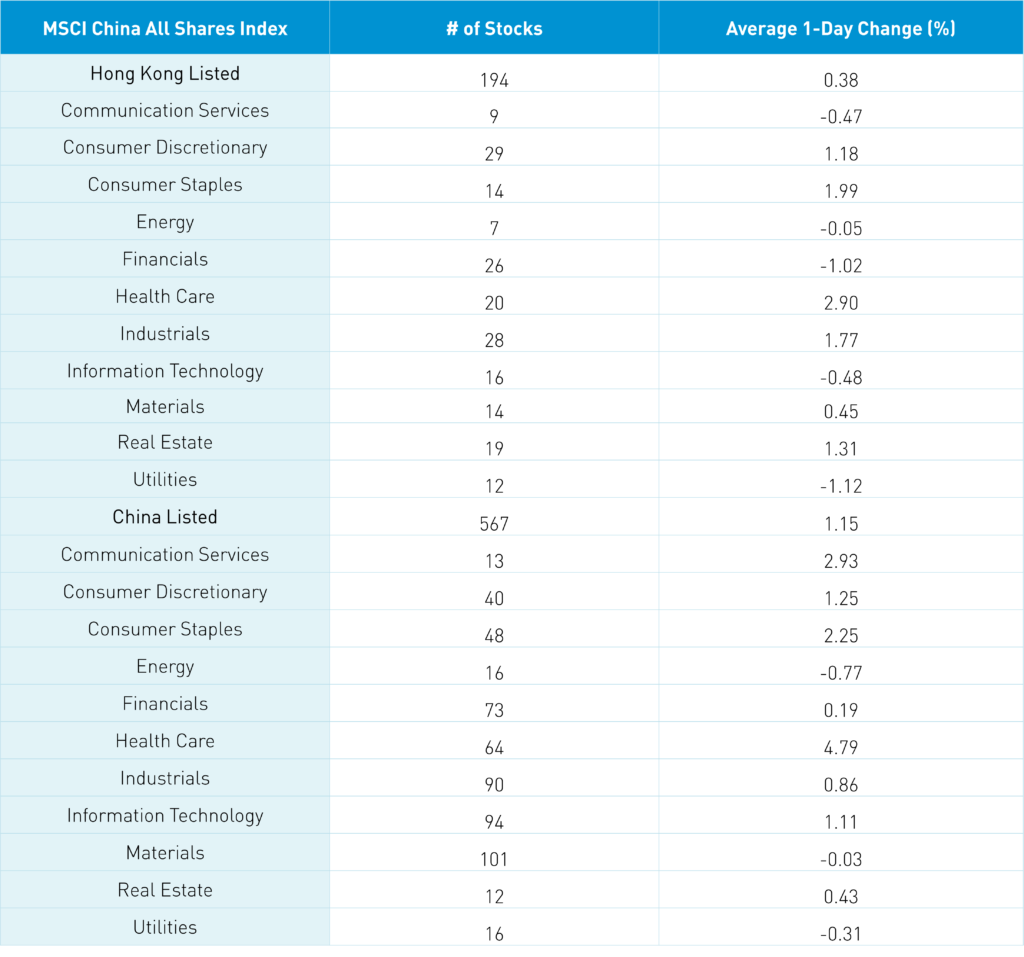

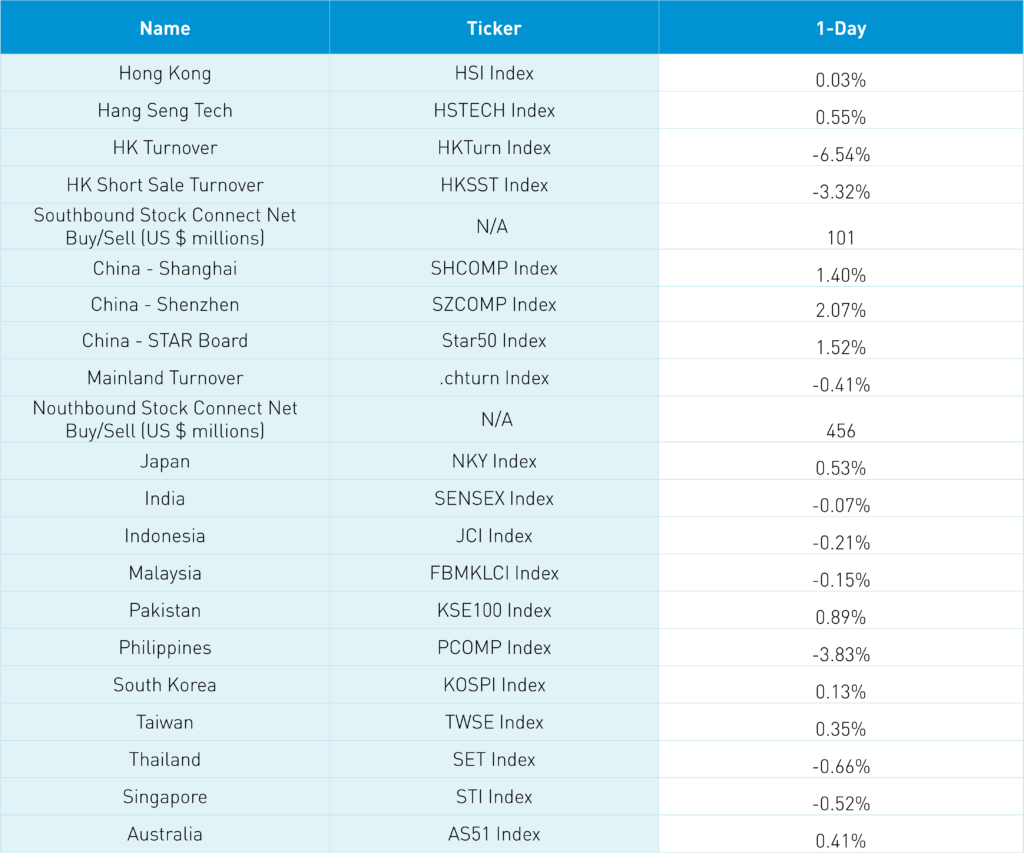

The Hang Seng and Hang Seng Tech gained +0.03% and +0.55% on volume -6.54% from yesterday, which is 77% of the 1-year average. 318 stocks advanced while 166 stocks declined. Main Board short sale turnover declined -3.32% from yesterday, which is 91% of the 1-year average, as short trading accounted for 20% of total trading. Growth and value factors were mixed as large caps underperformed small caps. Top sectors were healthcare +2.9%, staples +1.99%, and industrials +1.77% while utilities -1.12%, financials -1.02%, and tech -0.48% were down. Top sub-sectors included online education, pharma, and travel related, while gas, REITs, and Apple ecosystem underperformed. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $101 million of Hong Kong stocks, with Tencent a strong buy, Meituan a moderate/strong buy, and Li Auto a small buy.

Shanghai, Shenzhen, and the STAR Board gained 1.4%, 2.07%, and 1.52%, respectively, on volume that decreased -0.41% from yesterday, which is 66% of the 1-year average. 3,902 stocks advanced, while 713 declined. Top sectors were healthcare +4.81%, communication +2.96%, and staples 2.28% while energy -0.74%, utilities -0.28%, and materials -0.01% were down. The top-performing subsectors were medical devices, travel-related stocks, and generic drugs, while coal, lithium mining, and solar were among the worst. Northbound Stock Connect volumes were moderate/light as foreign investors bought $456 million of Mainland stocks today. Treasury bonds rallied, CNY eased -0.5% versus the US $ to 7.17, while copper rallied James Bond style +0.07%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.17 versus 7.16 yesterday

- CNY/EUR 6.91 versus 6.89 yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.72% yesterday

- Yield on 10-Year China Development Bank Bond 2.84% versus 2.85% yesterday

- Copper Price +0.07% overnight