PMIs & Real Estate in Focus, Week in Review

4 Min. Read Time

Week in Review

- Asian equities saw another week of turbulent trading, with growth stocks seeing the brunt of the selling pressure on increasing concerns about global growth and monetary policy.

- Trip.com and other travel-related stocks rallied early in the week as Hong Kong and Macau scrapped quarantine requirements for visitors. Mainland China is expected to follow suit by shortening the duration of requisite visitor quarantines.

- The National Health Commission on Tuesday announced that it would provide loans to hospitals for medical equipment upgrades, sending many health care stocks higher.

- The US dollar’s rise appears to be peaking though the People’s Bank of China (PBOC) continues to make it more difficult to short the Yuan, protecting the currency’s value against the dollar.

Key News

Asian equities closed lower following yesterday’s US equity market meltdown except for India, after the Reserve Bank of India raised interest rates less than expected (0.5% and not 0.75%). Maybe the US Fed should do the same! I found five important items that came to the fore overnight and are worth mentioning, starting with September’s purchasing manager’s index (PMI) release.

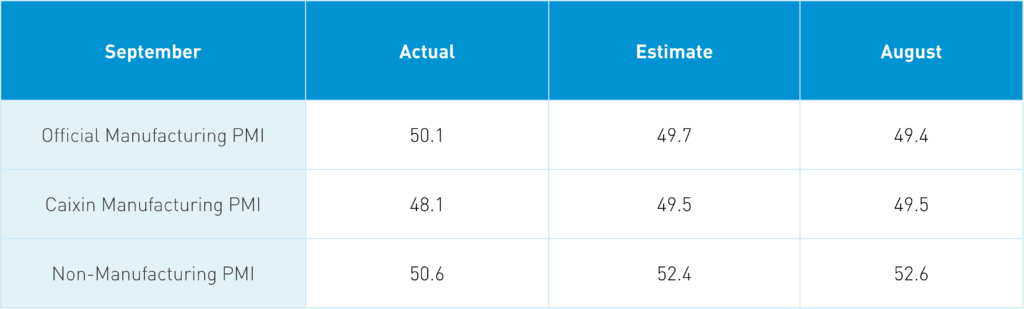

Item 1: PMIs are diffusion indexes meaning that readings above 50 indicate an expansion month-over-month and readings below 50 indicate a contraction. The “official” PMI survey is a large poll conducted by the government’s National Bureau of Statistics (NBS) and is focused on large companies. Meanwhile, the Caixin survey has fewer participants and therefore tends to be more volatile. It is conducted by IHS Markit (S&P Dow Jones bought them a few months ago) and focuses on small and medium-sized enterprises (SMEs). Did you notice all the attention given to the one PMI that was negative? Me too! As we anticipated, export orders are slowing as global stimulus fades, and the slowing global economy creates less demand for the world’s factory. This is why fiscal policy and stimulating consumption is and will continue to be a focus of China’s government. It is worth noting that business expectations were strong though you won’t read that elsewhere. It begs the question: why are companies bullish? Maybe they see more proactive government policies on the horizon.

Item 2: The Ministry of Finance and the State Administration of Taxation stated that those who sell an apartment to buy a new apartment from October 1st, 2022, to December 31st, 2023, will be eligible for individual income tax refunds. Also, 23 cities that have seen home prices fall over the last three months will be allowed to lower the mortgage rate for first-time buyers. These measures sent real estate stocks listed in Mainland China up by +4.39% and +0.6% in Hong Kong, another example of onshore versus offshore sentiment.

Item 3: The SEC fined Deloitte Touch-China $20 million for failing to “…adhere to numerous PCAOB auditing standards, including due professional care of audit evidence, sampling, documentation, internal control over financial reporting, audit supervision, and quality control.” Ouch! In addition to the fine being paid, it shows that the Chinese auditors from the Big Four are aligning themselves with the PCAOB audit review. This is a good sign, in my opinion.

Item 4: CNY appreciated +0.15% versus the US dollar to close at 7.11 versus yesterday’s 7.13 and Wednesday’s 7.20. China’s currency is quoted in CNY per US dollar, making a decline an appreciation as 7.11 renminbi equals $1 versus saying that 1 Renminbi is equal to $0.14. The PBOC is clearly prepared to intervene to stop the Renminbi’s slide. The Asia currency index hit another 52-week low.

Item 5: Indonesia approved a version of the FDA-approved mRNA vaccine produced by the China-based Walvax Biotechnology, which begs the question: when will it be approved in China? I would guess following the Party Congress this month, which could be a bigger push to further ease Zero Covid/Lives First policy.

Reiterating to our friends in Florida, Georgia, and the Carolinas to stay safe in the wake of Hurricane Ian.

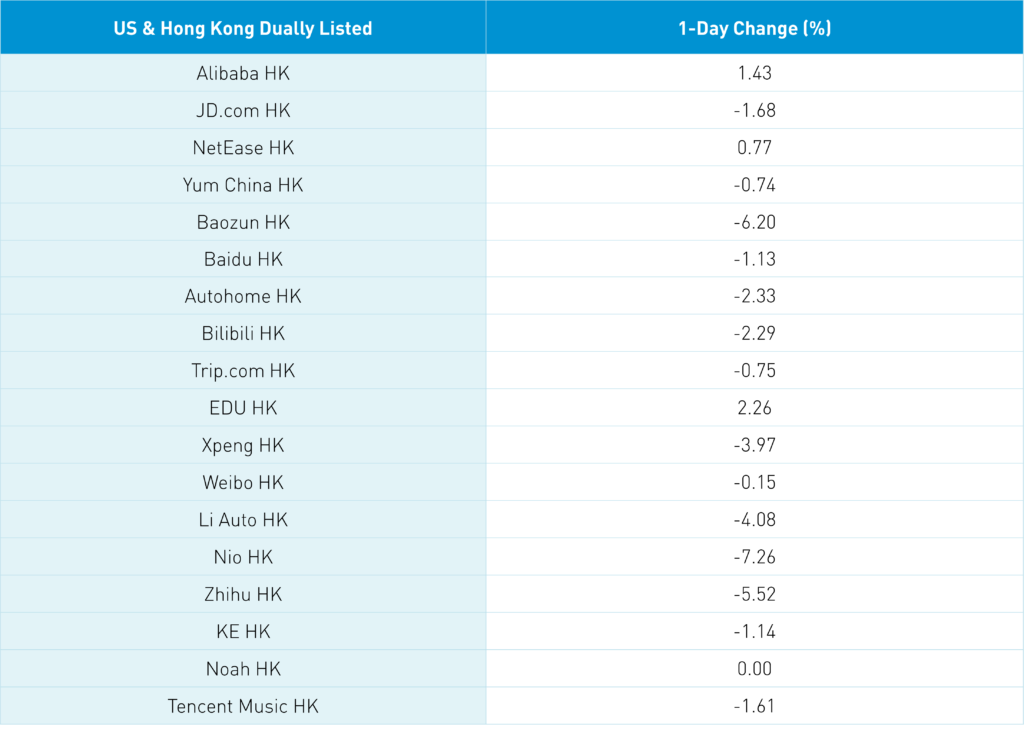

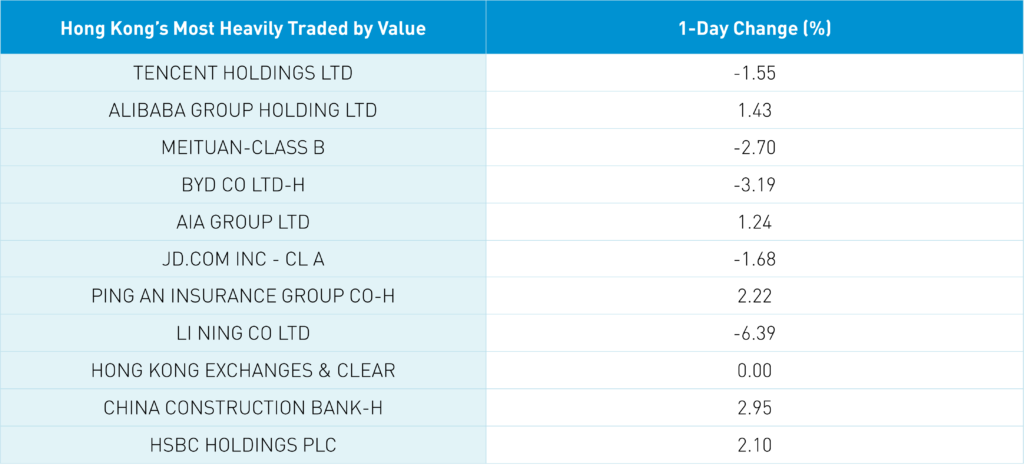

Hong Kong managed to close in the green though Hong Kong-listed internet stocks were off/mixed as Tencent fell -1.55%, Alibaba HK gained +1.43%, Meituan fell -2.7%, JD.com HK fell -1.68%, and Baidu HK fell -1.13%. Short volumes were lower as 29% of Meituan’s trading was short, 11% of Tencent’s, 15% of Alibaba HK’s, and 27% of JD.com’s. Nike’s weak results weighed on discretionary plays and competitors such as ANTA Sports, which fell -4.26%, and Li Ning, which fell -6.39%. I’m told that outdoor activities and exercise became very popular in China during COVID. Mainland China was off in advance of the weeklong holiday next week, with growth stocks underperforming as investors sold stocks to raise cash for their vacation. It is worth noting that the trajectory of Hong Kong’s opening continues unabated.

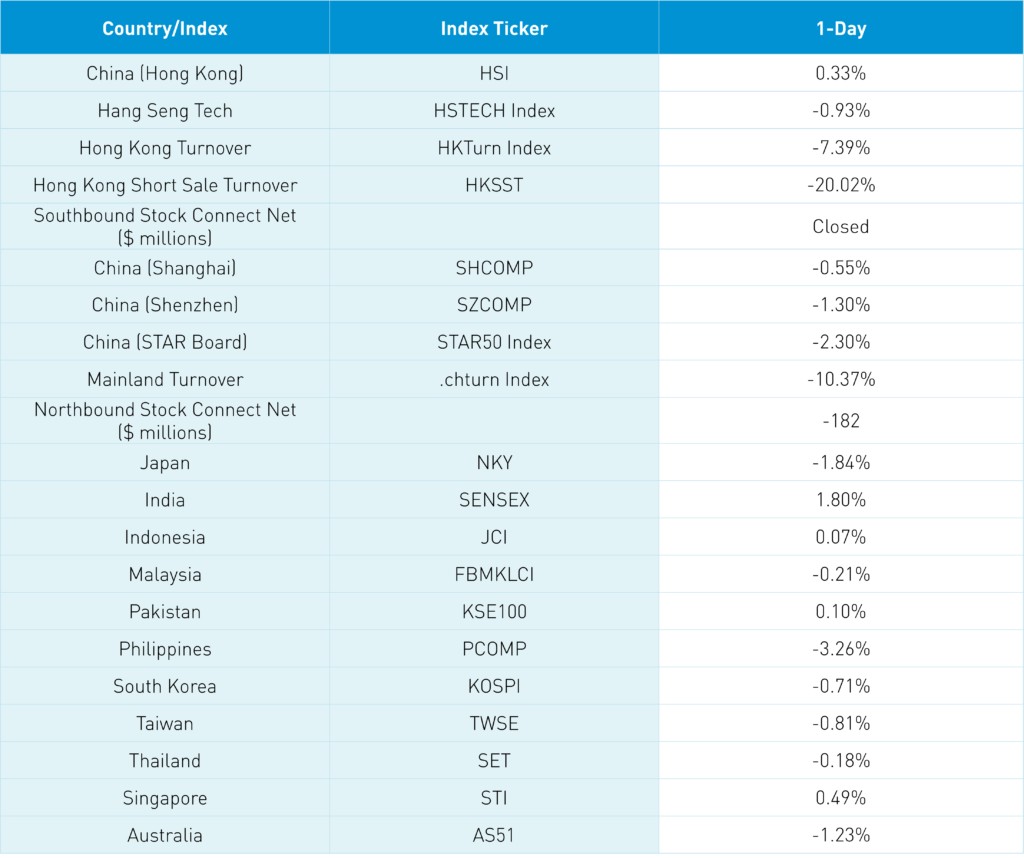

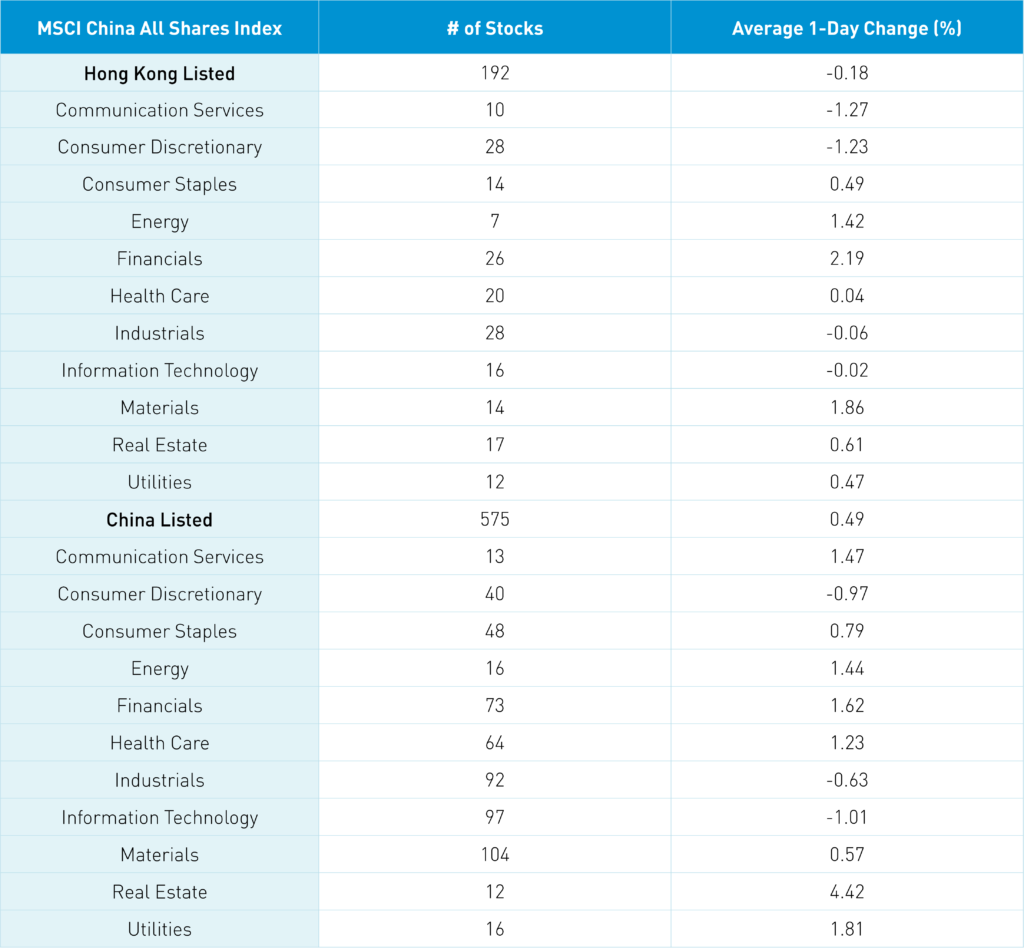

The Hang Seng and Hang Seng Tech indexes diverged to close +0.33% and -0.93%, respectively, on volume that decreased -7.39% from yesterday, which is 67% of the 1-year average. 256 stocks rose while 225 declined. Main Board short sale turnover declined -20% from yesterday, which is 73% of the 1-year average as 18% of trading was short. Value factors outperformed growth factors as small caps outpaced large caps. The top performing sectors were financials, which gained +2.19%; materials, +1.85%; and energy, which gained +1.42%. Meanwhile, communication fell -1.27%, consumer discretionary fell -1.23%, and industrials fell -0.06%. The top-performing subsectors were banks, insurance, and education stocks. Meanwhile, autos, sporting goods, and software were among the worst performing. Southbound Stock Connect was closed overnight.

Shanghai, Shenzhen, and the STAR Board closed -0.55%, -1.3%, and -2.3% on volume that fell -10.37% from yesterday, which is 56% of the 1-year average. 1,574 stocks advanced while 2,886 stocks declined. Value factors outperformed growth while large caps outpaced small caps. The top performing sectors were real estate, which gained +4.39%, utilities, which gained +1.79%, and financials, which gained +1.59%. Meanwhile, technology fell -1.04%, discretionary fell -0.99%, and industrials fell -0.66%. The top-performing subsectors were biotech, traditional Chinese medicine, and real estate, while power generation, auto/auto parts, and semiconductors were among the worst. Northbound Stock Connect volumes were moderate as foreign investors sold -$182 million worth of Mainland stocks. Treasury bonds sold off, CNY appreciated +0.12% versus the US dollar to 7.11 from 7.13, and copper gained +0.48%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.12 yesterday

- CNY per EUR 6.97 versus 6.97 yesterday

- Yield on 1-Day Government Bond 1.49% versus 1.28% yesterday

- Yield on 10-Year Government Bond 2.76% versus 2.75% yesterday

- Yield on 10-Year Chain Development Bank Bond 2.94% versus 2.89% yesterday

- Copper Price +0.48% overnight