Real Estate Rebounds on Policy Support, China Begins Golden Week Holiday

2 Min. Read Time

Key News

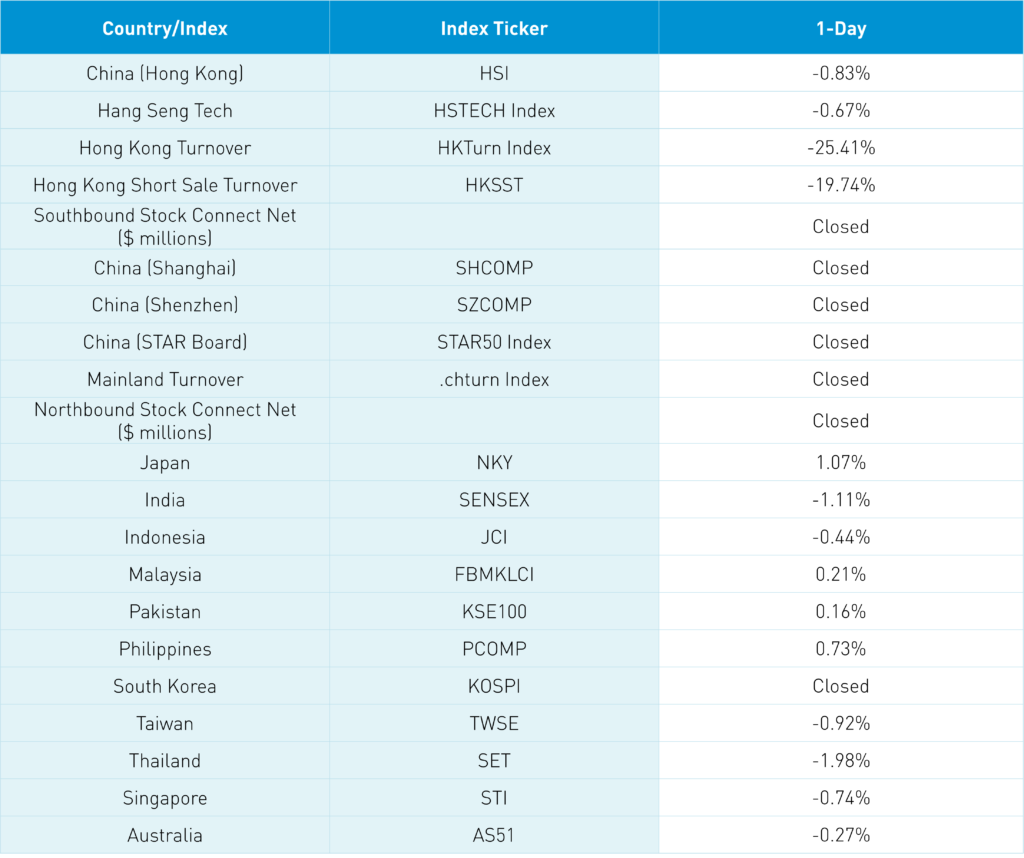

Asian equities were largely off, as Japan outperformed while India and Thailand underperformed.

China is closed this week for the National Holiday, while South Korea was closed today for National Foundation Day. 130 million vacation trips are estimated to be taken this year, less than last year. Many urban dwellers visit their ancestral homes and/or go on vacation.

The Hong Kong market was off though it rose mid-day as the UK canceled its proposed corporate tax cut, leading Hang Seng Index heavyweight HSBC (5 HK) to mitigate losses to close -2.18% versus its intra-day low of -3.52%.

With China on vacation for Golden Week and Hong Kong closed tomorrow, we should anticipate light volumes this week as Hong Kong volumes dropped -25% from Friday to just 50% of the 1-year average. Short selling volumes fell -19% from Friday to 58% of the 1-year average as 20% of Hong Kong’s Main Board turnover was short. Taiwan reportedly raised its short margin requirements, which the Hong Kong Exchange should consider to avoid what I believe is becoming an embarrassing situation. Overnight, 39% of JD.com HK’s turnover was short though Meituan, Tencent, and Alibaba saw short turnover decline.

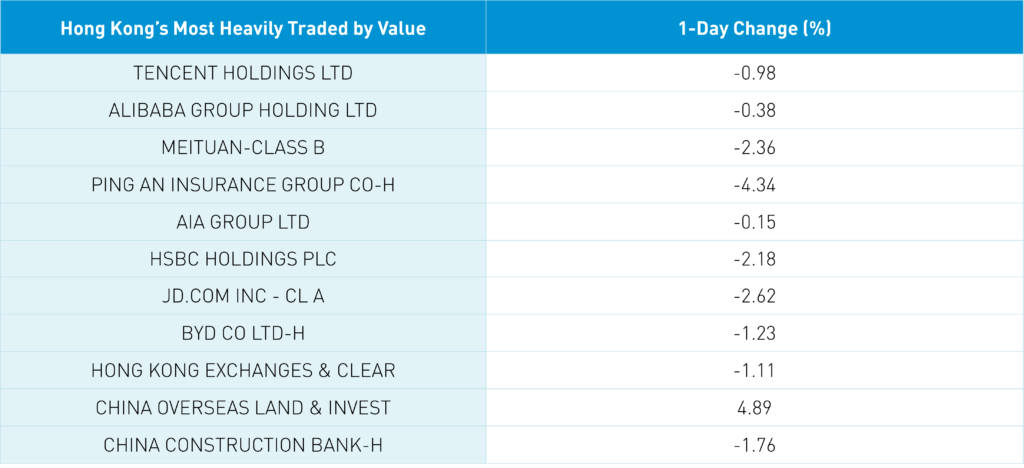

Real estate was Hong Kong’s top performing sector overnight, gaining +5.02% as online real estate agent KE Holdings HK (2423 HK) gained +8.99% following the release of multiple supportive policies on Friday. It should be very clear to investors that housing and the Evergrande situation have the full attention of China’s government. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.98%, Alibaba HK, which fell -0.38%, and Meituan, which fell -2.36% on no news.

September car sales data was released overnight. Nio HK gained+2.22% after delivering 10,878 vehicles, which is +29% year over year (YoY), XPeng HK fell -0.22% after selling 8,468 vehicles (+15% YoY), and Li Auto HK, which fell -0.39% after selling 11,531 vehicles (+5.6% YoY). It is worth noting that BYD (1211 HK) fell -1.23% despite selling 201,259 vehicles, of which 94,941 were EVs (+161% YoY).

Bilibili HK (9626 HK) gained +0.67% after making Hong Kong its primary exchange, which should pave the way for a Southbound Stock Connect inclusion in November.

On Friday, we noted Deloitte-China paying a fine to the SEC for several infractions during their audits. If Deloitte-China wasn’t going to audit US-listed Chinese companies in the future, why would they pay the fine?

The Hang Seng and Hang Seng Tech indexes were off -0.83% and -0.67%, respectively, on volume that decreased -25.41% from Friday, which is 50.77% of the 1-year average. 218 stocks advanced while 273 stocks declined. Main Board short selling turnover fell -19.74%, which is 58.96% of the 1-year average, as short selling accounted for 20% of total turnover. Growth and value factors were mixed as small caps outperformed large caps. The top performing sectors were real estate, which gained +5.02%, materials, which gained +1.66%, and health care, which gained +0.61%. Meanwhile, financials fell -2.45%, utilities fell -2.34%, and consumer discretionary fell -1.13%. The top-performing subsectors were online education, property management, and semiconductors. Meanwhile, banks, insurance, and household products were among the worst. Southbound Stock Connect was closed overnight.

Shanghai, Shenzhen, and the STAR Board are closed this week.

Last Night’s Exchange Rates, Prices, & Yields

Mainland China’s fixed income and currency markets were closed overnight.