State Council Balances Zero Covid & the Economy as Guangzhou Takes Center Stage

3 Min. Read Time

Key News

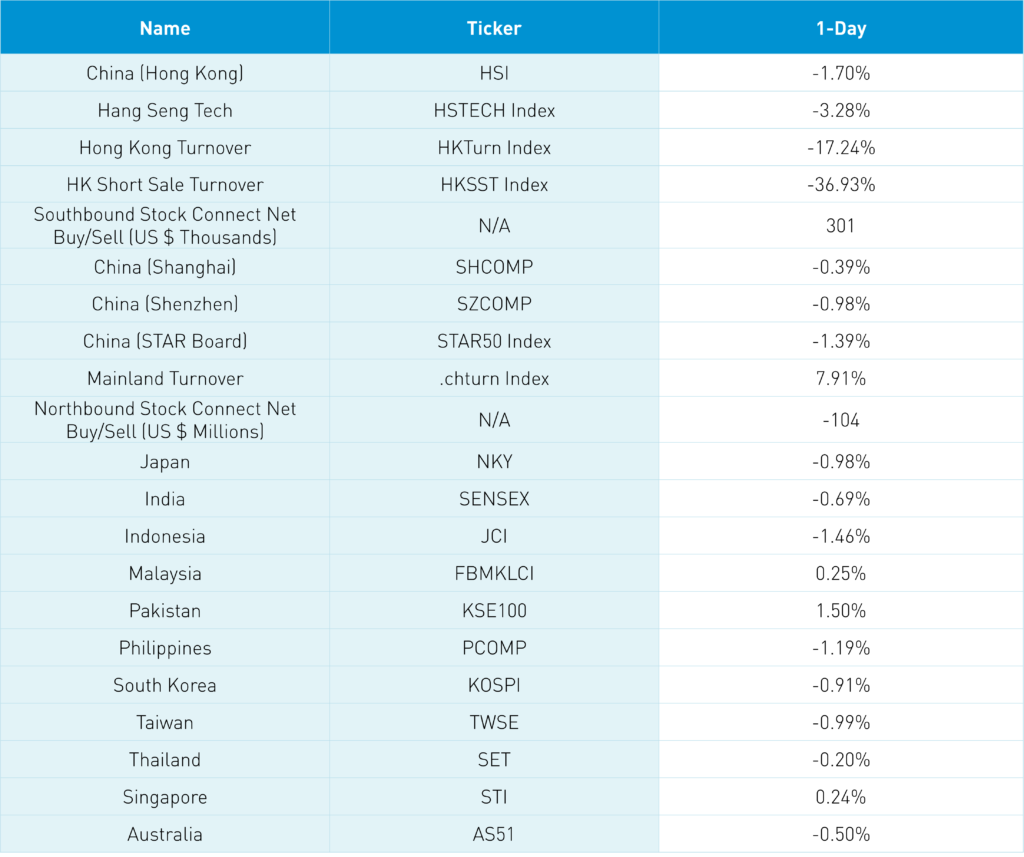

Asian equities were a sea of red, as Singapore and Malaysia managed small gains. The onshore versus offshore dynamic played out again overnight as offshore China, i.e., Hong Kong, fell after yesterday’s steep decline in US-listed China stocks while onshore China, i.e., Shanghai & Shenzhen, was off, but not nearly as much. Hong Kong didn’t fall nearly as much as US-listed Chinese stocks did yesterday, which led to this morning's rebound.

The Public Company Accounting Oversight Board (PCAOB) stated at a conference that they are continuing their audit reviews, having left Hong Kong. This is neither good nor bad, as it isn’t surprising they haven’t decided. It is hard to believe Alibaba, Yum China, and JD.com’s Big Four accountants shouldn’t pass an audit review. Volumes were light in advance of the US CPI print, which likely led shorts to press their bets knowing managers aren’t stepping in to buy the stocks. The crypto collapse is probably an additional factor contributing to risk-off sentiment.

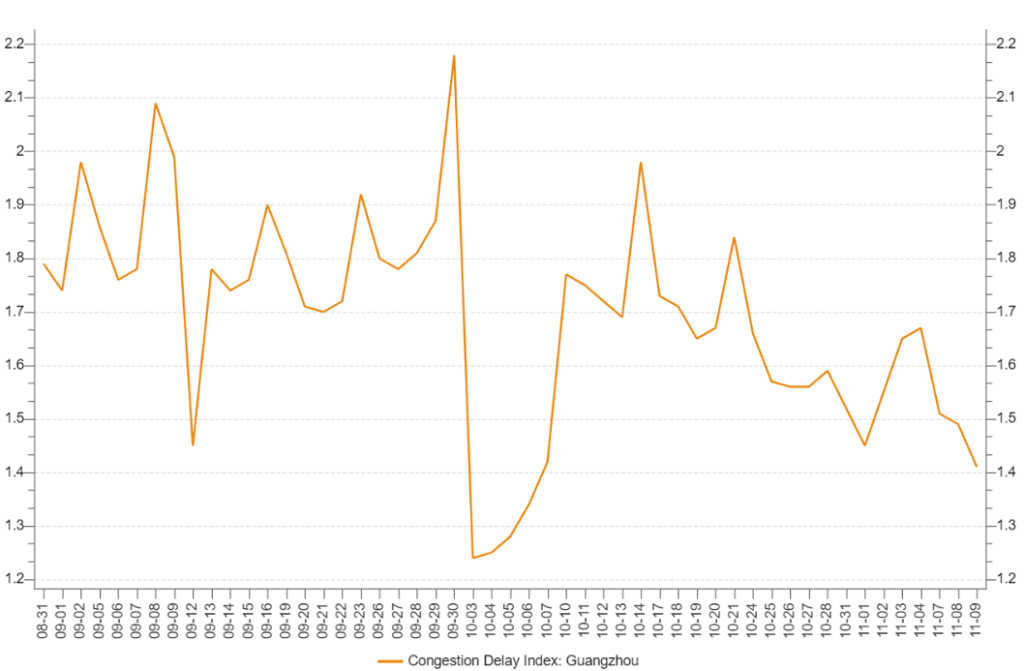

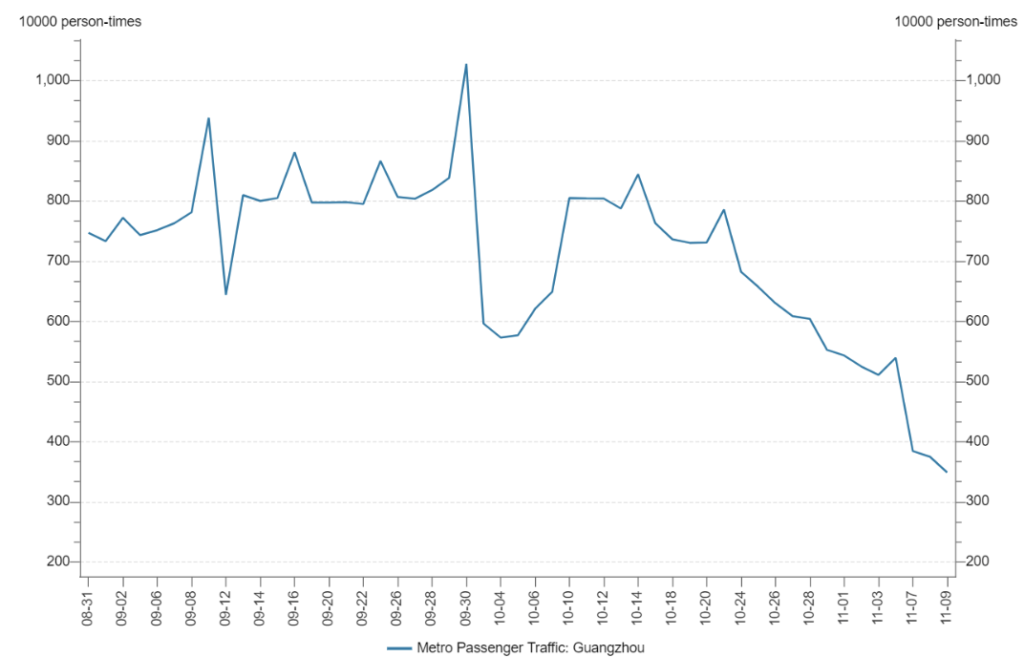

Optimism on China’s adjusted zero covid policy is being tempered as covid cases rise with 1,133 new cases and another 7,691 asymptomatic cases. Maybe local governments underreported covid cases in advance of the Party Congress? The evidence would suggest as cases are up nearly 8X post-Party Congress. The important city of Guangzhou has a significant outbreak though companies and movements are still being allowed. Below are charts tracking the city’s traffic and numbers of subway passengers. Clearly, covid controls are in place as subway traffic is curtailed to limit spread on a crowded train car though street traffic is high as people can drive to work so not a total shutdown thus far. Overnight the Standing Committee acknowledged the growing covid cases stating “unswervingly adhere” to covid protection. They then stated, “…protect the safety and health of people’s lives to the greatest extent, and minimize the impact of the epidemic on economic and social development.” Yes, zero covid, but don’t hurt the economy.

President Biden confirmed he would meet with President Xi at the G-20 summit while US and China climate folks talk at the global warming conference COP22.

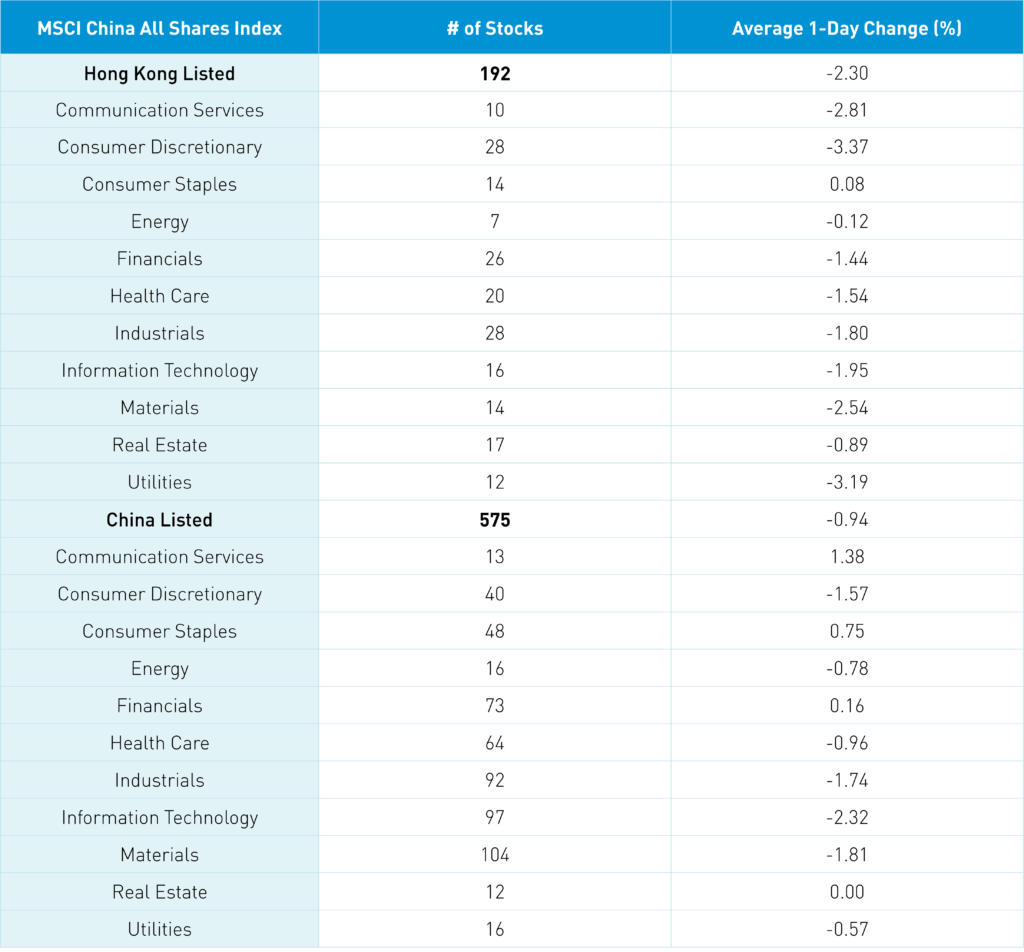

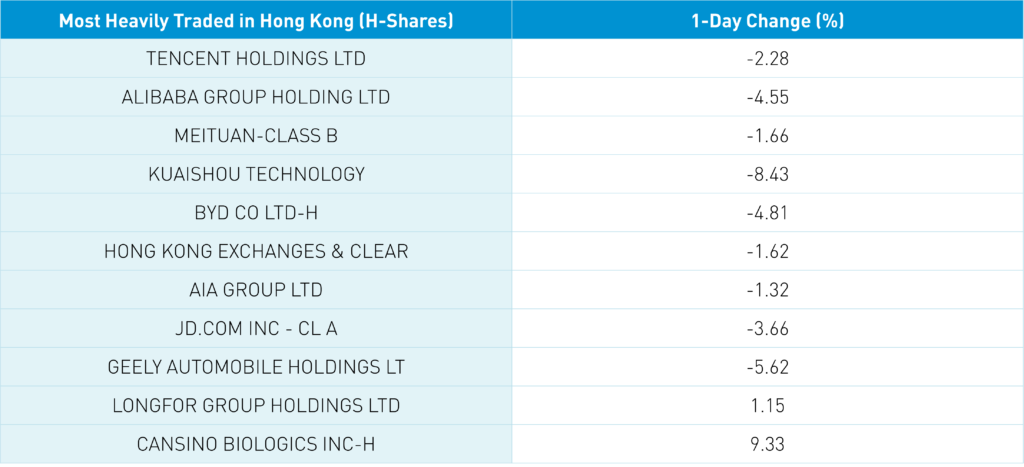

After the close, we had both October aggregate financing and new loans miss expectations, providing another reason to dial back zero covid. Hong Kong’s most heavily traded were Tencent, which fell -2.28%, Alibaba HK, which fell -4.55%, and Meituan, which fell -1.66% as concerns about Singles Day volumes weigh on e-commerce. Popular growth stocks were off in both Hong Kong and China, though Mainland investors bought the dip via Southbound Stock Connect. Breadth was much better in China than in Hong Kong, as Mainland investors are not as pessimistic. NIO’s pre-US market open financial results should help the EV space. Foreign investors were small sellers of Mainland stocks via Northbound Stock Connect. CNY was off slightly versus the US, though it had a strong day versus the Euro.

Today at 5 pm, MSCI announces their Semi-Annual Index Review, which is the Super Bowl for index geeks!

Data from Wind

The Hang Seng and Hang Seng Tech fell -1.7% and -3.28% on volume -17.24% from yesterday, which is 74% of the 1-year average. 69 stocks advanced, while 432 declined. Main Board short turnover declined -36.91% from yesterday, which is 53% of the 1-year average, as 12% of turnover was short turnover. Value factors outperformed growth factors as large caps “outperformed” small caps. Staples was the only positive sector, +0.08%, while discretionary -3.36%, utilities -3.18%, and communication -2.81%. Food was the only positive sub-sector, while auto, retailers, and software were among the worst. Southbound Stock Connect volumes were moderate as Mainland investors bought $301mm of Hong Kong stocks, with Tencent, Meituan, and Kuiashou small net buys.

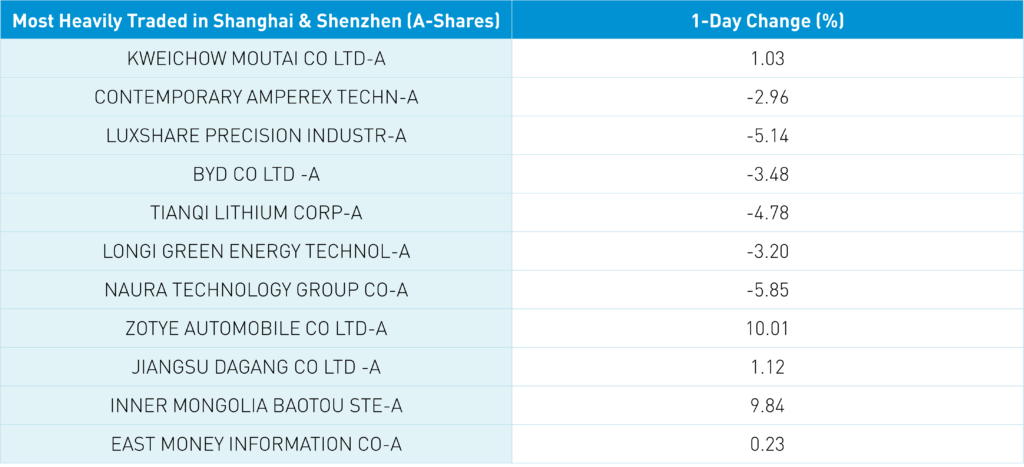

Shanghai, Shenzhen, and STAR Board were off -0.39%, -0.98%, and -1.39% on volume +7.91% from yesterday, which is 86% of the 1-year average. 1,721 stocks advanced, while 2,811 stocks declined. Value factors outperformed growth factors as large caps outperformed small caps. Top sectors included communication +1.4%, staples +0.77%, and financials +0.18%, while tech -2.3%, materials -1.79%, and industrials -1.72%. Top sub-sectors included media, internet, and airports, while motorcycles, industrial machinery, and fine chemicals were among the worst. Northbound Stock Connect volumes were light/moderate as foreign investors sold -$104mm of Mainland stocks. Treasury bonds were off with 10 Year yield at 2.7%, and CNY was off -0.19% versus the US dollar to 7.25 though CNY had a strong day versus the Euro while copper was +0.68%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.25 versus 7.25 yesterday

- CNY per EUR 7.22 versus 7.29 yesterday

- Yield on 10-Year Government Bond 2.70% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.82% yesterday

- Copper Price +0.68% overnight