Markets Cheer Dynamic Zero COVID, Major City Mobility Tracker, Week in Review

4 Min. Read Time

Week in Review

- Auditors from the US Public Company Accounting Oversight Board (PCAOB) have left Hong Kong, which investors took as a positive sign that they had a successful trip reviewing the audit books of auditors of US-listed Chinese companies.

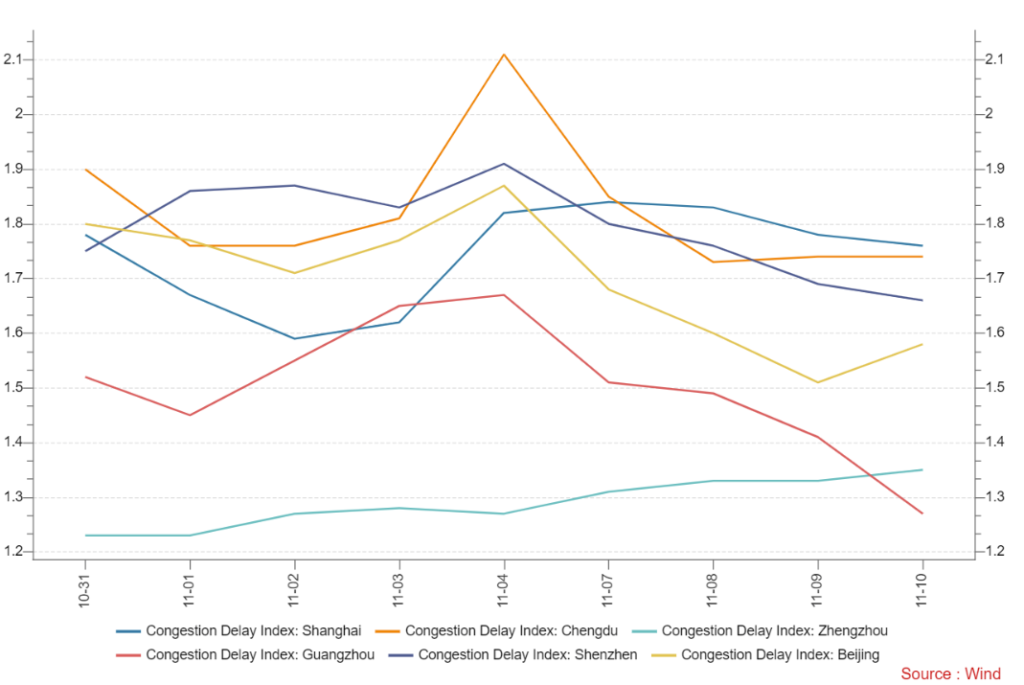

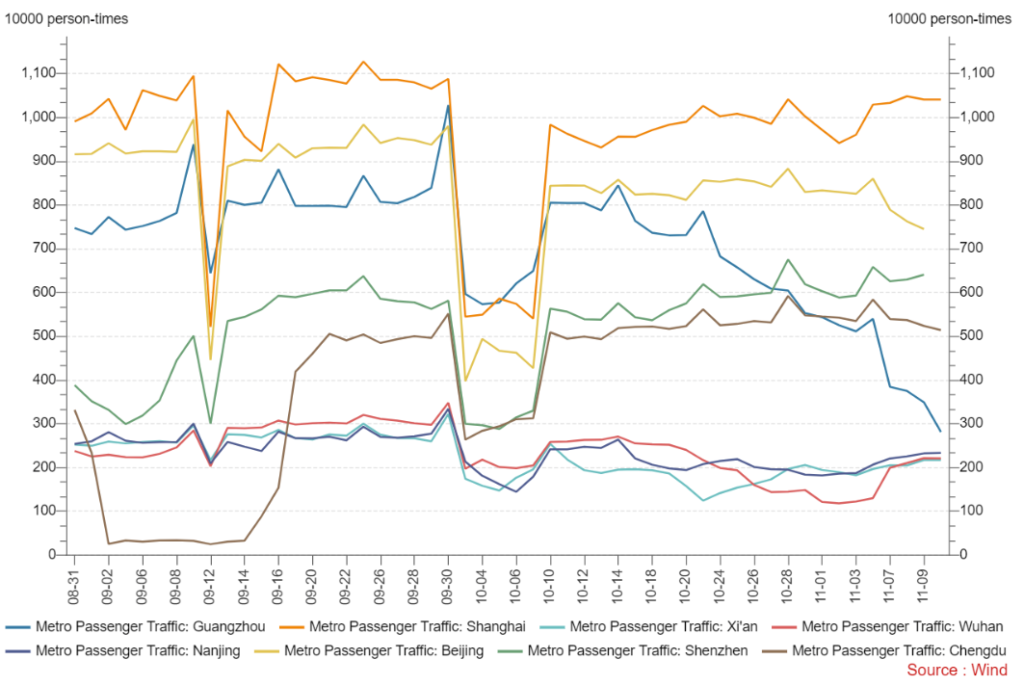

- This week, we witnessed some reprieve from China’s zero COVID policy as cases continued to increase in China without accompanying citywide lockdowns. We will be publishing independent data on traffic in key Chinese cities on a regular basis to check up on the country’s progress in loosening restrictions.

- We learned Thursday that President Biden will meet with President Xi at the sidelines of the G20 summit in Bali, Indonesia.

- Today is Singles Day (11/11), the namesake day of the multi-week sales festival for Chinese E-Commerce platforms. This year, Alibaba’s Tmall Global is partnering with outlet malls across the United States to offer Chinese consumers the same deals they used to get by visiting the outlets in person. We document Tmall’s livestream from Woodbury Commons here in New York in this week’s video.

Friday's Key News

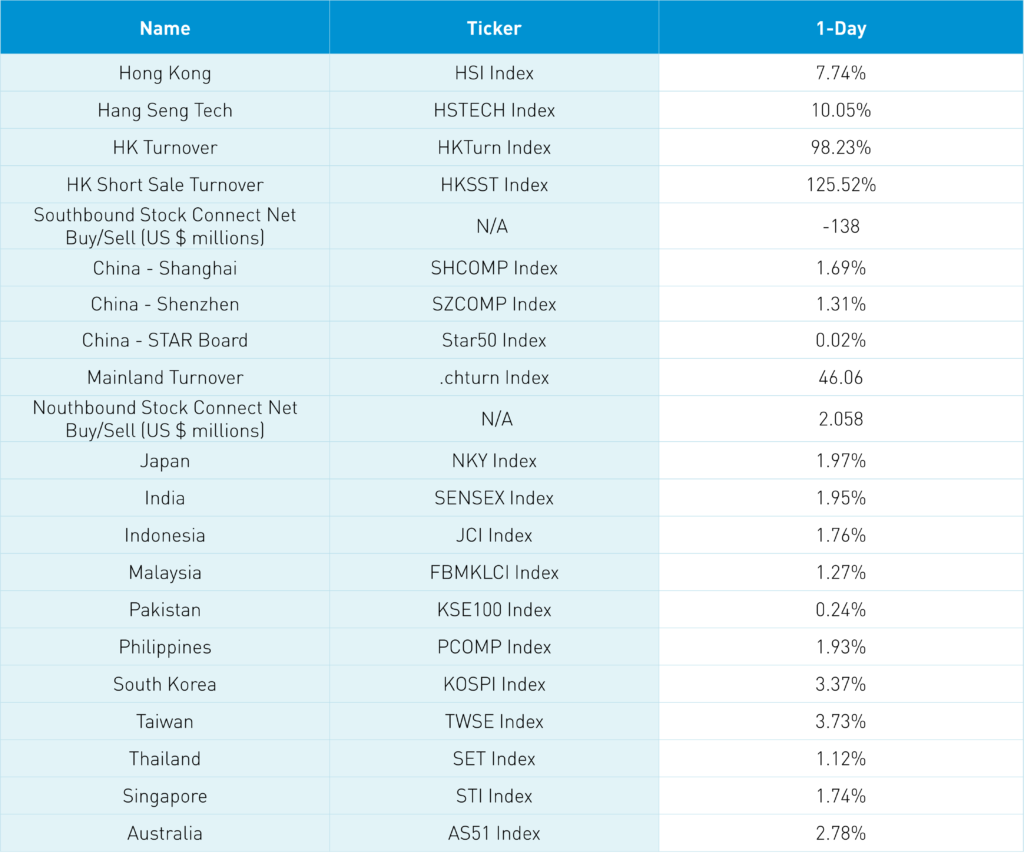

Happy Veterans Day! Asian equity markets were a sea of green overnight as investors cheered yesterday’s US CPI print as the US dollar index fell -0.99%, the Asia Dollar Index gained +0.68%, and the Renminbi gained +0.86% versus the dollar.

Hong Kong and Mainland China outperformed on yesterday’s State Council release on the incremental easing of zero covid policy. Hong Kong got the “nitrous oxide” early in the afternoon as the State Council released twenty points articulating dynamic zero COVID as local officials will be given more control to adjust policies. The government demonstrated that it is aware of citizens’ frustration by eliminating mass COVID testing, eliminating quarantines at a government facility to at-home quarantines for those exposed and for those leaving areas where an outbreak takes place. The government will also stop trying to identify close contacts. Foreign investors cheered another reduction for inbound travelers’ quarantine requirement, dropping it from 7 days to 5 days followed by 3 days at home/hotel. A push for vaccinations with an emphasis on the elderly while drug stockpiling and hospital preparation takes place. Remember that zero COVID will not go away overnight, but rather incrementally. It is worth noting that there were 1,150 new covid cases in China overnight along with another 9,385 asymptomatic cases.

There will be a great deal of attention given to the major city of Guangzhou, which is dealing with an outbreak with 2,583 new cases reported today, of which 2,358 were asymptomatic. The Guangzhou Municipal Commission of Health stated that it will follow the State Council’s twenty points.

Major City Mobility Tracker, Courtesy of Wind

Friday's Key News (Continued)

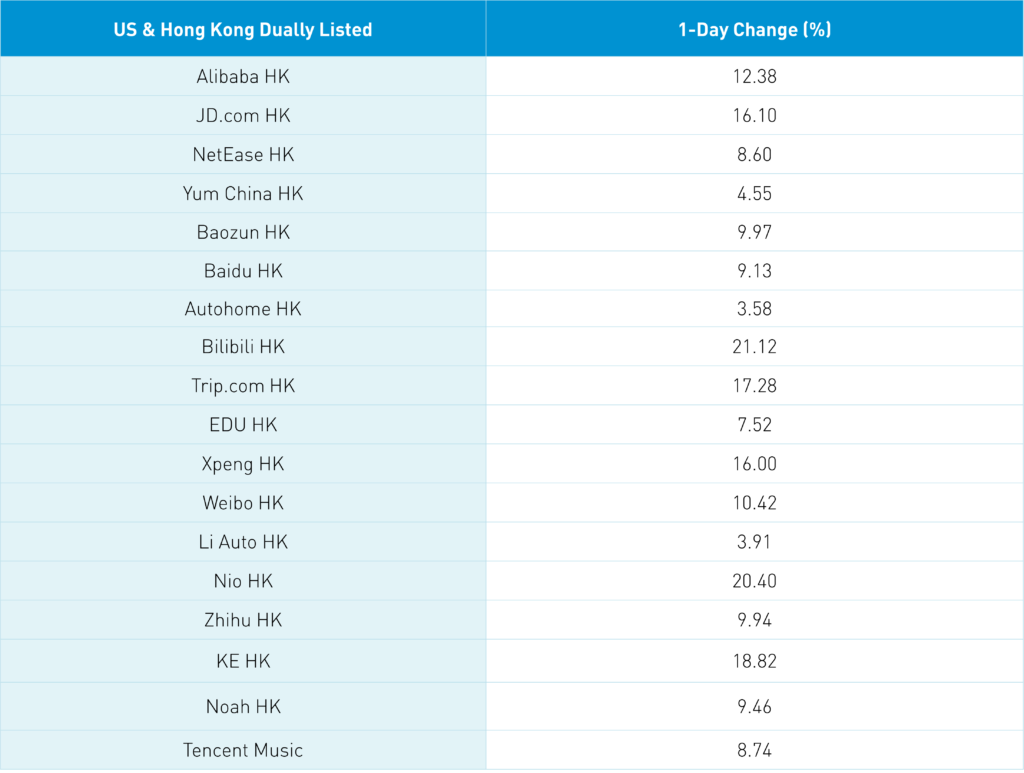

Hong Kong rose more than US-listed China stocks did yesterday, which is leading to a good day for US-listed China stocks today. The Hang Seng Tech Index jumped +10.05% on very high volume. Did short sellers get run over today? Yes, short covering undoubtedly was a factor, as evidenced by Hong Kong outperforming Mainland China, though many investors are underweight the space, which, hopefully, gives the rally legs.

We also have Biden and Xi meeting next week as I am completely baffled by the lack of understanding of how intertwined the US and China economies are, along with the significant performance of US multinational companies’ revenue in China. Did you know Texas is the largest exporting state to China? LNG, gas, and semiconductors are all key exports to China from the state. This is a fact.

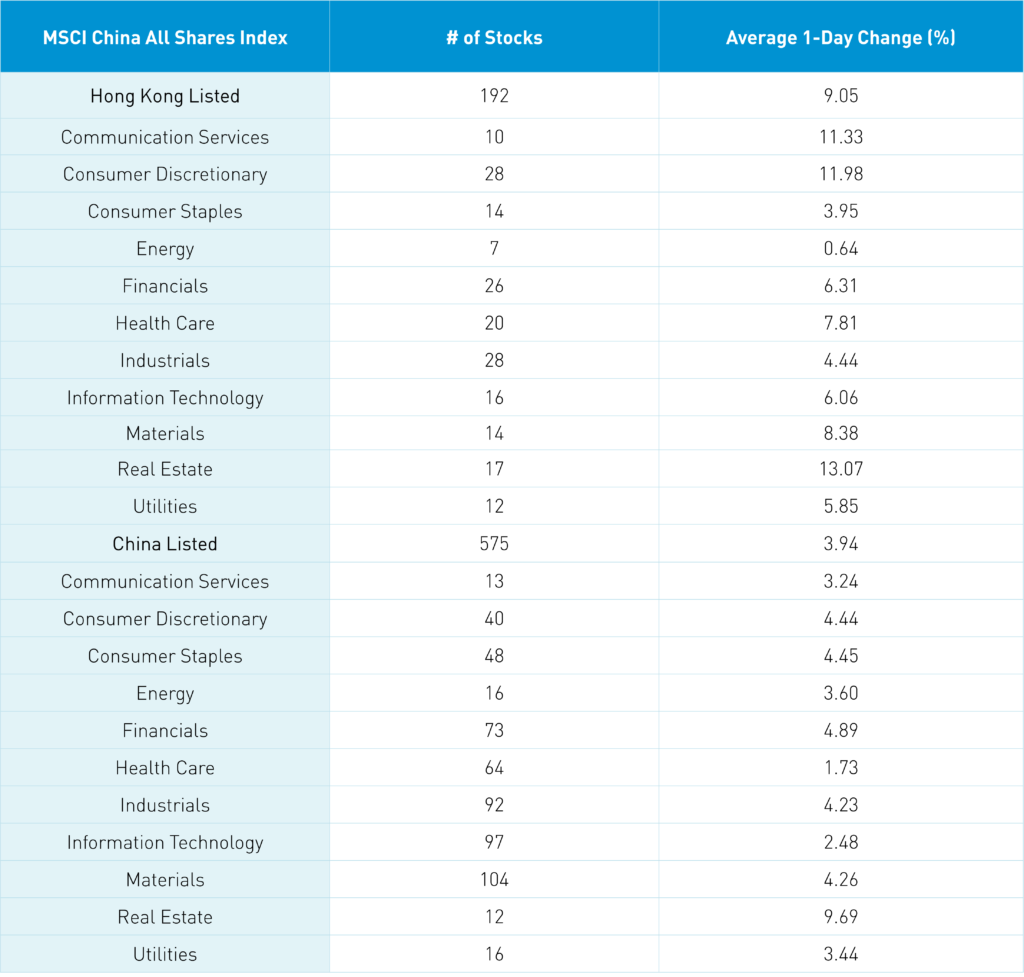

It is interesting that Mainland investors took small profits in Hong Kong stocks today as Southbound Stock Connect saw a small net outflow today. Foreign investors bought a healthy $2 billion worth of Mainland stocks via Northbound Stock Connect. Mega-cap growth stocks, which are both domestic and foreign favorites, had a strong day. Real estate was the best sector in both Mainland China, where it gained +9.98%, and Hong Kong, where it gained +13.17% as Mainland media noted the Association of Financial Institutional Investors will support the sector following the PBOC’s statement of support. The most contrarian trade in the world is Chinese real estate developer bonds, which can be scooped up for tasty yields of well over 10%.

Today is Singles Day, China’s famous E-Commerce sales festival. Expectations appear light Alibaba topping last year’s +$3 trillion worth of goods sold might not happen. Nonetheless, the sales will still represent huge hauls for E-Commerce companies.

This will be a big week for earnings with Tencent, Alibaba, NetEase, and JD.com are all reporting!

MSCI released their pro-forma for the end of November Semi-Annual Index Review, which requires passive asset managers to rebalance their index funds and ETFs, so they mimic the refreshed benchmarks. China had 36 securities added and 34 deleted, while India had 6 additions and South Korea had 1 addition and 10 deletions. China is still by far the largest country in the MSCI Emerging Markets Index with 723 of its 1,389 holdings being China-based, at a weight of 30.2%. Asia is 76.5% of EM market capitalization.

The Hang Seng and Hang Seng Tech indexes jumped +7.74% and +10.05%, respectively, on volume that increased +98.23% from yesterday, which is 148% of the 1-year average. 490 stocks advanced while 23 declined. Main Board short selling increased +125.66% from yesterday, which is 121% of the 1-year average, as 14% of turnover was short turnover. Value factors edged out growth factors as small caps outpaced large caps. All sectors were positive as real estate gained +13.08%, consumer discretionary gained +11.99%, and communication services gained +11.35%. The top-performing subsectors were retailers, software, and consumer durables. Southbound Stock Connect volumes were very high at 2X the average as Mainland investors sold -$138 million worth of Hong Kong stocks as Kuaishou was a very small net sell along with Tencent.

Shanghai, Shenzhen, and the STAR Board gained +1.69%, +1.31%, and +0.02%, respectively, on volume that increased +46.6% from yesterday, which is 126% of the 1-year average. 2,707 stocks advanced while 1,836 declined. Value factors outpaced growth factors as large caps outpaced small caps. All sectors were positive, led by real estate, which gained +9.87%, financials, which gained +5.07%, and consumer staples, which gained +4.63%. The top-performing subsectors were real estate, precious metals, and household products while airports, biotech, and leisure goods were among the worst. Northbound Stock Connect volumes were high as foreign investors bought a net $2 billion worth of mainland stocks today. Treasury bonds sold off as CNY gained +0.86% versus the US dollar to close at 7.10 versus yesterday’s 7.19 as copper gained +1.44%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.10 versus 7.19 yesterday

- CNY per EUR 7.32 versus 7.31 yesterday

- Yield on 1-Day Government Bond 1.20% versus 1.22% yesterday

- Yield on 10-Year Government Bond 2.74% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.87% versus 2.83% yesterday