Hong Kong Internet Rally Goes Free Solo on the Wall of Worry

3 Min. Read Time

Key News

Asian equities were mixed/mainly lower, as Hong Kong outperformed significantly, India managed a small gain, and the Philippines closed for the Feast of the Immaculate Conception. Asia investors cheered the ten measures that dial back COVID restrictions and the strong statement from the Mainland media following the Politburo meeting, which bears repeating, “… the recovery of consumer demand is particularly critical to economic growth, and consumption is directly related to epidemic prevention policies.”

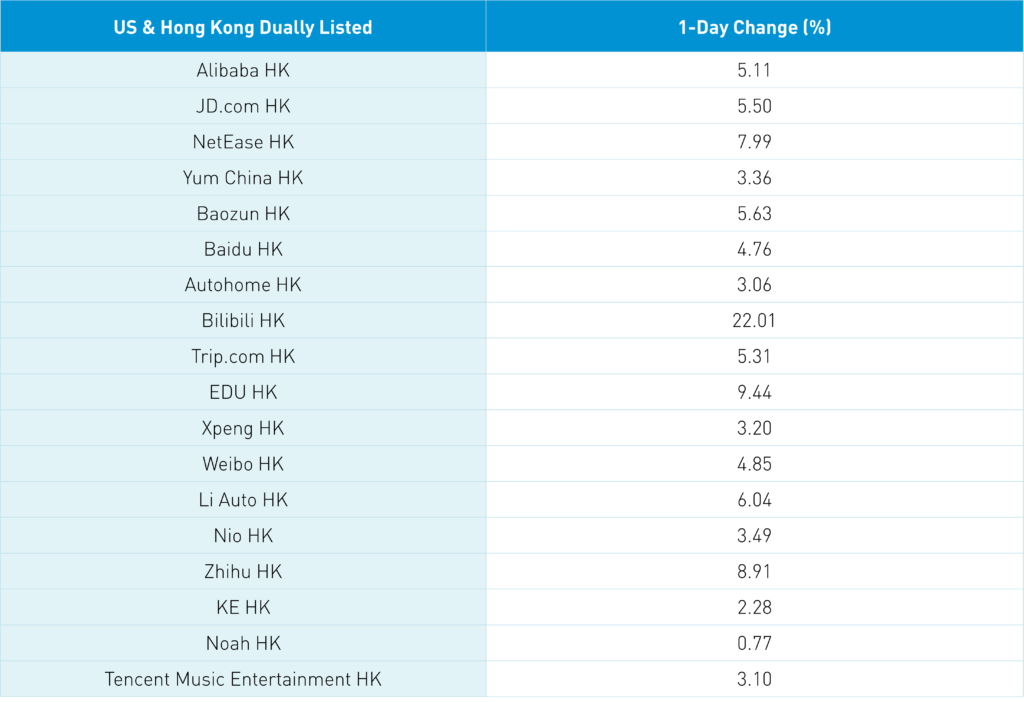

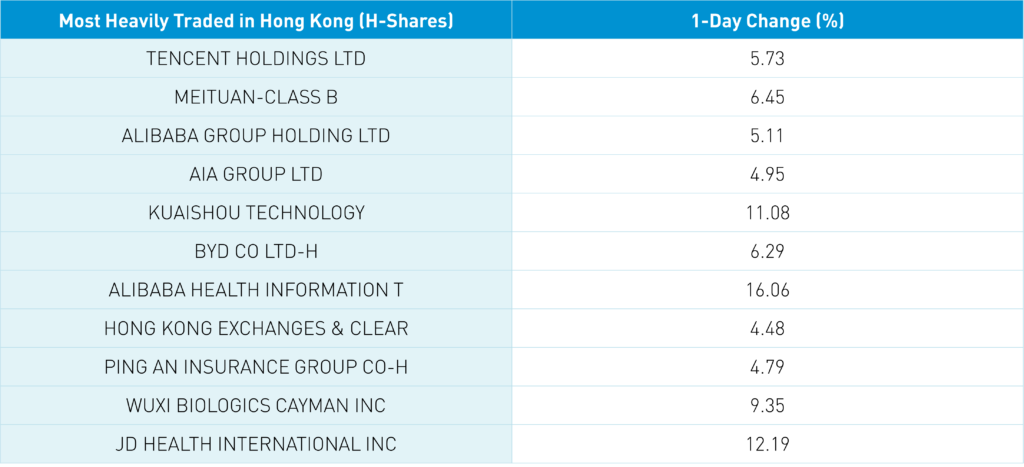

Although a pullback in US-listed Chinese stocks occurred, Hong Kong internet stocks had a strong day, with Hong Kong’s most heavily traded by value, Tencent +5.73%, Meituan +6.45%, and Alibaba HK +5.11%. Several companies had very strong days, such as Kuaishou +11.08%, Alibaba Health +16.06%, JD Health +12.19%, and Bilibili HK +22.01%, indicating shorts are still being run over.

I mentioned yesterday that CNY, China’s currency, has been stable, indicating a conducive environment for Chinese stocks. Watching financial television earlier this week, when asked, the four professional portfolio managers on the show all said China was “uninvestable.” Good! Stay on the sidelines as the pain trade is higher with CEWC and the potential for an ADR delisting solution providing potential catalysts! Worth noting that accelerating the ADR delisting was not included in the defense budget (NDAA), according to a DC source. Mainland China was flat overnight, with real estate outperforming as the CSRC Vice Chairman Li Chao and Shanghai Stock Exchange General Manager Cai Jianchun spoke about accelerating the rollout of REITs at a conference. Issuing REITs would provide another financing tool for distressed property developers. From a news perspective, President Xi visited Saudi Arabia and Hello Group (ticker MOMO) beat analyst estimates on revenue and adjusted net income though adjusted EPS was missing. There were 4,031 new COVID cases and 17,134 asymptomatic cases though our Major City Mobility Tracker is showing a pick-up in subway traffic (see below).

Sun Yu of Bridgewater’s China team, the world’s largest hedge fund, garnered attention in Mainland media for an interview in which she noted a fairly pessimistic outlook for the US, Europe, and the UK due to credit liquidity tightening and the risk of stagflation though “China is completely different. China is (in) the stage of liquidity improvement and economic support. In the future, policies are more supportive of the economy, and the future growth comes from domestic consumption and technology development…it is more attractive to stocks.”

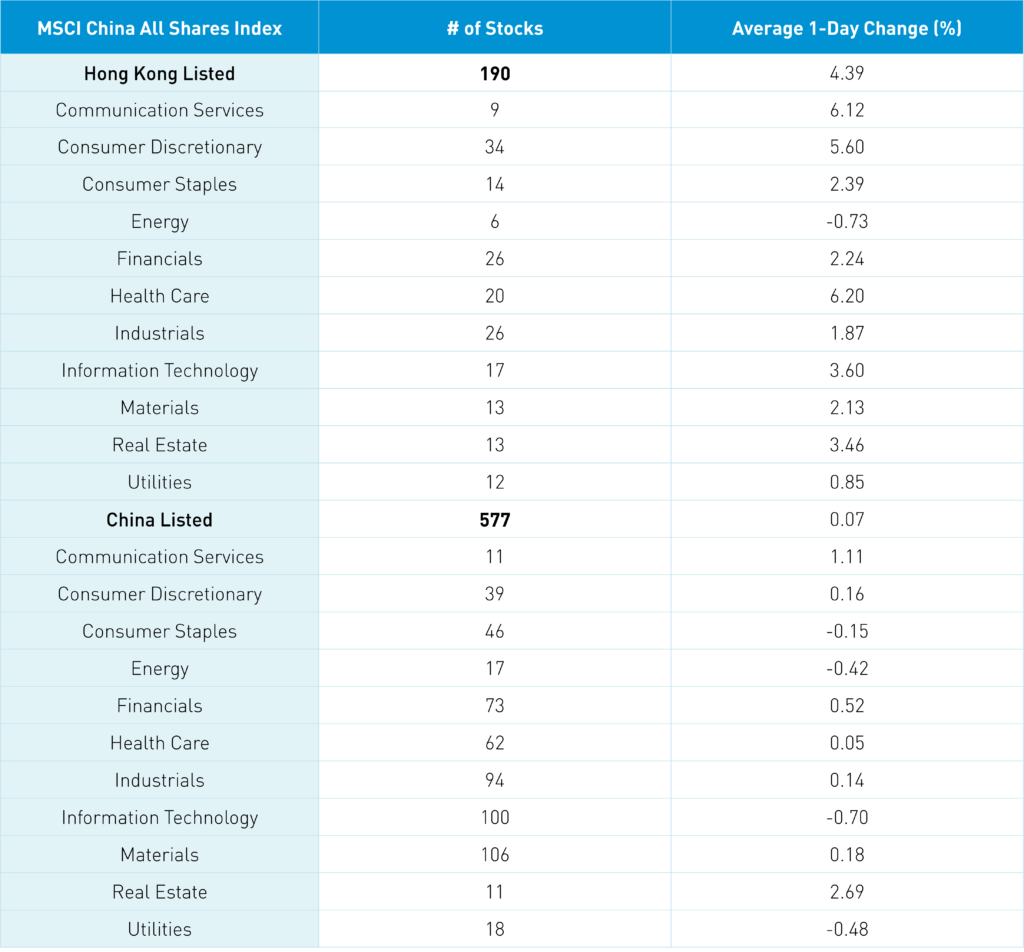

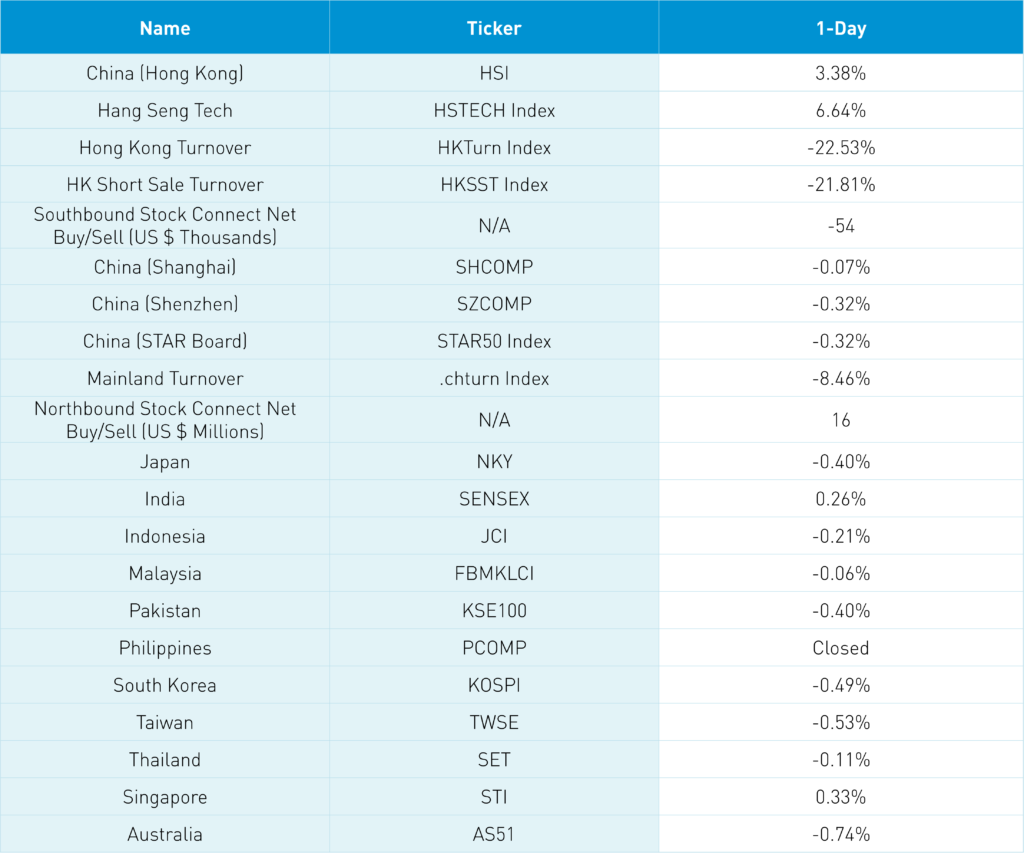

The Hang Seng and Hang Seng Tech gained +3.38% and +6.64% on volume -22.53% from yesterday, which is 130% of the 1-year average. 454 stocks advanced, while 46 stocks declined. Main Board short turnover declined -21.81% from yesterday, which is 111% of the 1-year average, as 15% of turnover was short turnover. Growth factors edged out value factors though mixed, as small caps outperformed large caps. The top sectors were healthcare +6.2%, communication +6.12%, and discretionary +5.6%, while energy was the only down sector -0.73%. The top sub-sectors were healthcare equipment, consumer services, and software, while telecom and energy were off. Southbound Stock Connect volumes were elevated/nearly 2X the 1-year average as Mainland investors sold -$54mm of Hong Kong stocks with Tencent, Meituan, Kuaishou, and XPeng, all small net buys.

Shanghai, Shenzhen, and STAR Board were off -0.07%, -0.32%, and -0.32% on volume -8.46% from yesterday, which is 91% of the 1-year average. 1,602 stocks advanced, while 3,005 stocks declined. Value factors outperformed growth factors, while large caps outpaced small caps. The top sectors were real estate +2.68%, communication +1.09%, and financials +0.51%, while tech -0.71%, utilities -0.49%, and energy -0.44%. Top sub-sectors were real estate, education, and household products, while diversified financials, agriculture, and computer hardware were among the worst. Northbound Stock Connect volumes were moderate/high as foreign investors bought $16mm of Mainland stocks with a preference for Shenzhen/growth stocks over Shanghai/value stocks. CNY was off slightly versus the US dollar -0.05% to 6.97, the Treasury yield curve steepened, and copper gained +0.24%.

Major Chinese City Mobility Tracker

Traffic trends have remained stable though subway traffic continues to uptick. The latter indicates higher tolerance for comingling on crowded subway cars.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.97 versus 6.98 yesterday

- CNY per EUR 7.32 versus 7.33 yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.87% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.02% yesterday

- Copper Price +0.24% overnight