Chinese Tourism Stocks Rally

3 Min. Read Time

Key News

Asian equities were mixed overnight on light volumes.

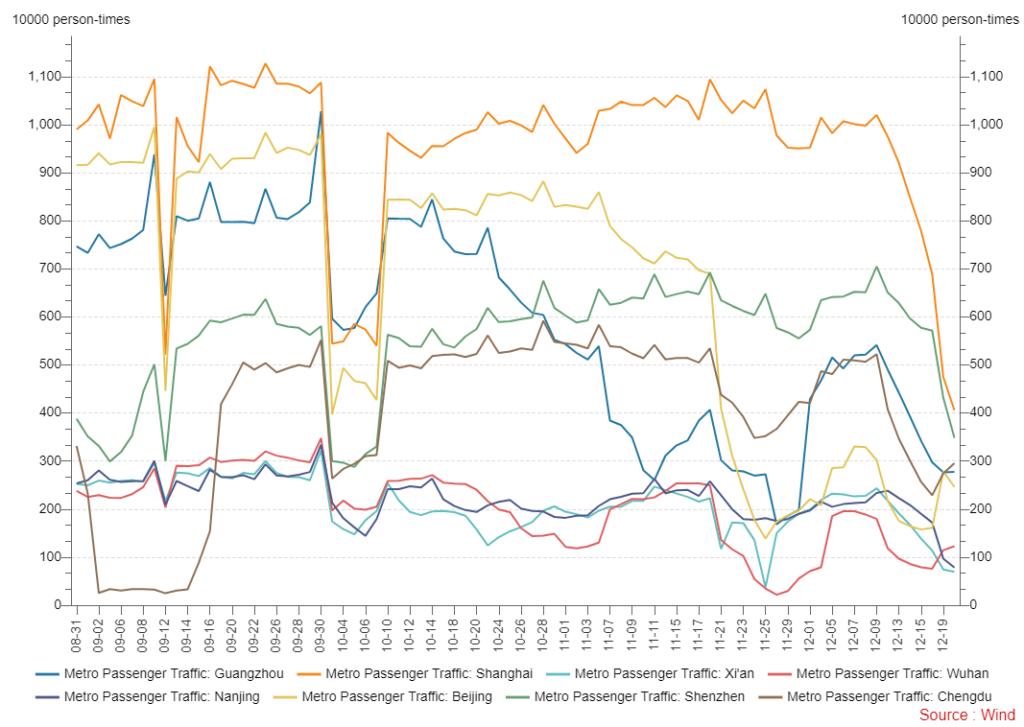

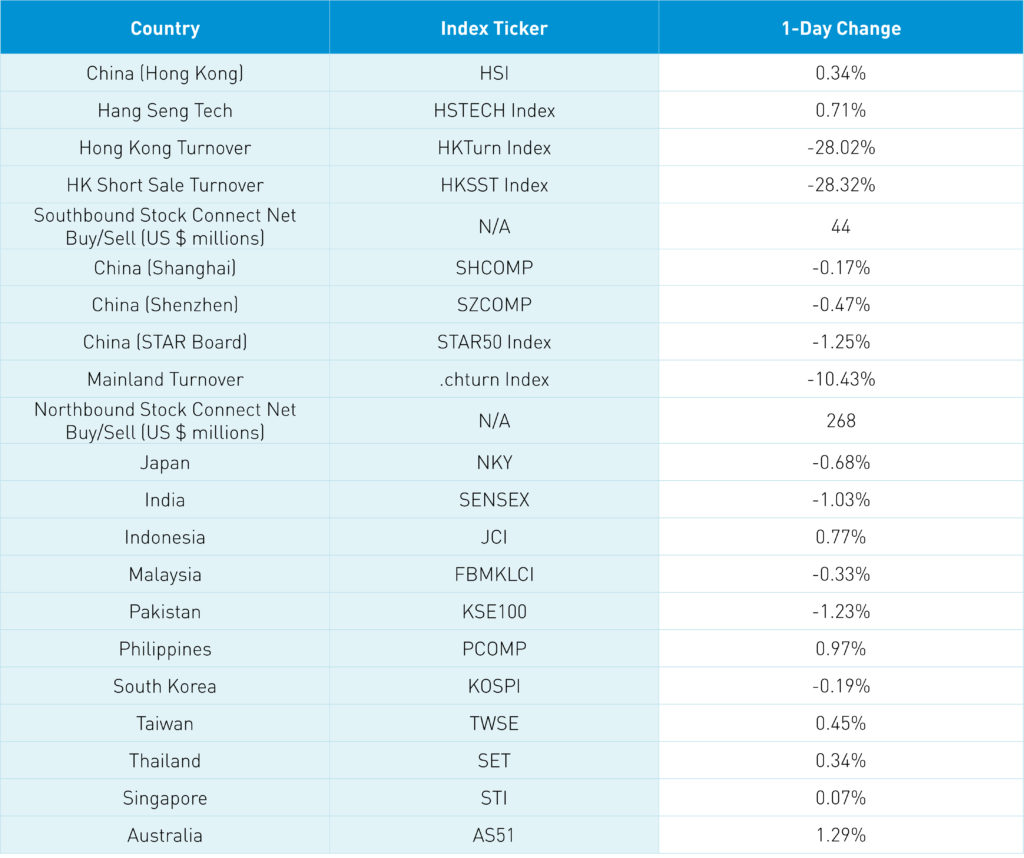

COVID's spread in China is garnering more attention than I would have thought from Western media. 100% COVID is spreading through China as some cities close schools while our Mobility Tracker shows the drop off in traffic and subway usage. While Mainland China has been off the last few days, the market hasn’t collapsed. In fact, since the end of October to yesterday’s close, the S&P 500 is down -1.01%, while the Shanghai Composite gained +11.54%, and the Shenzhen Component finished up +10.10% in US dollars. While COVID concerns weigh on Mainland sentiment, it is worth pointing out that today’s best-performing subsectors in China were airports, which gained +2.07%, and the catering tourism industries, which gained +1.87%. Who else didn’t care? Foreign investors bought a net $268 million worth of Mainland stocks today via Southbound Stock Connect.

Premier Li and the State Council, along with the China Securities Regulatory Commission (CSRC) put out statements following the Central Economic Work Conference (CEWC) pro-consumption push. Hong Kong rebounded today, with healthcare as the top-performing sector, gaining +1.83% overnight.

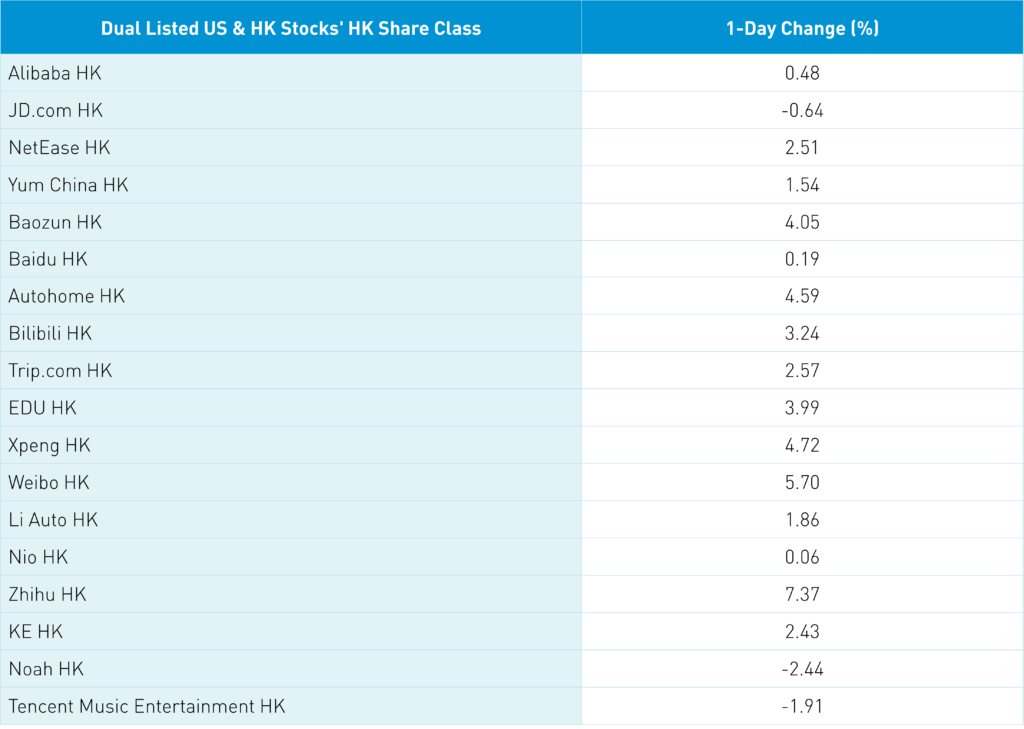

Reuters reported this morning that BioNTech’s vaccine has been shipped to China. The vaccine is meant for use by foreigners residing in China. The vaccine may be rolled out to China's general population in short order. Hong Kong’s most heavily traded stocks were Tencent, which gained +0.52%, Alibaba, which gained +0.48%, and Meituan, which fell -0.74%, with internet names largely higher, except for JD.com, which fell -0.64%.

Last Friday’s index rebalances of the Nasdaq 100 dropped Baidu and NetEase from the index as their market cap is no longer among the top 100 largest companies listed. I’m told that the FAANG index dropped Alibaba and Baidu at their last rebalance. An ETF provider dropped Tencent, Baidu, and Weibo from their EM and China ETFs at the end of October! Of course, we had a pension plan announce they will cut their China position in half a month ago. Having been in the passive/index business for twenty-two years, I’ve seen these moves all the time, which are contrarian! History doesn’t repeat itself, but it does rhyme! S&P 500 adds Yahoo in 1999... tech crashes. Financials become +20% of the S&P 500 in 2008… financial crisis. Hang Seng adds tech stocks to the Hang Seng Index in 2020... China tech crashes. Growth stocks become nearly 30% of S&P 500… growth crashes/value rallies. US energy stocks become “non-investable” in 2021… energy stocks are the best performer in 2022. Chinese property developers become 50% of Asia High Yield Index... property market crashes. Indices delete China stocks from their indices...

The Hang Seng and Hang Seng Tech gained +0.34% and +0.71% on volume, down -28.02% from yesterday, which is 56% of the 1-year average. 281 stocks advanced, while 168 declined. Main Board short turnover -28.39% from yesterday, which is 47% of the 1-year average, as 15% of turnover was short turnover. Growth factors outperformed value factors as large caps outperformed small caps. The top-performing sectors were healthcare, which gained +1.83%, materials +1.44%, and financials +0.70%, while real estate fell -0.16%. Top sub-sectors were pharma, telecom services, and consumer services, while household products, auto, and utilities were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $44 million of Hong Kong stocks, with Kuaishou a moderate sell, and Tencent and Meituan small net buys.

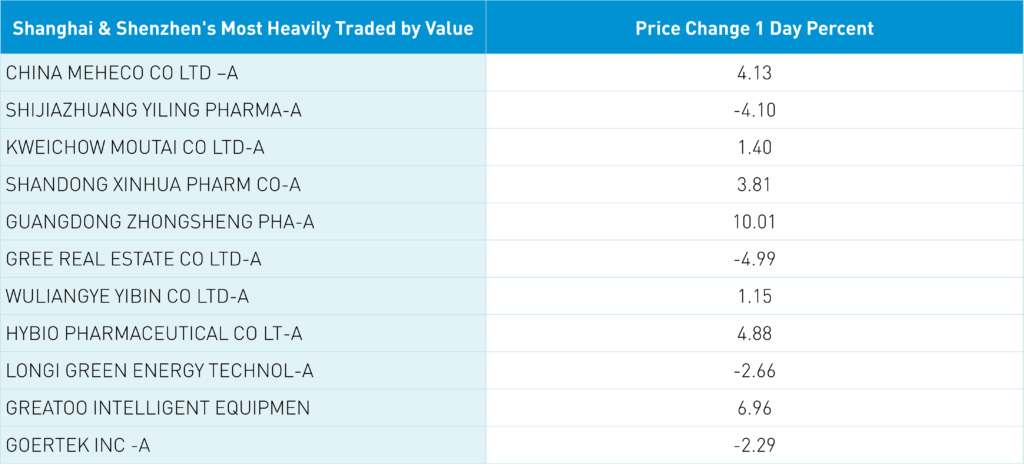

Shanghai, Shenzhen, and STAR Board were off -0.17%, -0.47%, and -1.25%, respectively, on volume that was down -10.43% from yesterday, which is 47% of the 1-year average. 1,272 stocks advanced, while 3,347 stocks declined. Value factors outperformed growth factors, while large caps outperformed small caps. The top-performing sectors were consumer staples, which gained +1.07%, communication services, which gained +0.93%, and financials +0.23% while tech -1.4%, industrials -0.64%, and energy -0.53%. The top-performing subsectors were airports, the catering and tourism industry, and liquor, while motorcycles, auto parts, and semis were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $268 million worth of Mainland stocks overnight. CNY fell versus the US dollar, -0.26% to 6.98, Treasury bonds rallied, and copper gained +0.74%.

Major Chinese City Mobility Tracker

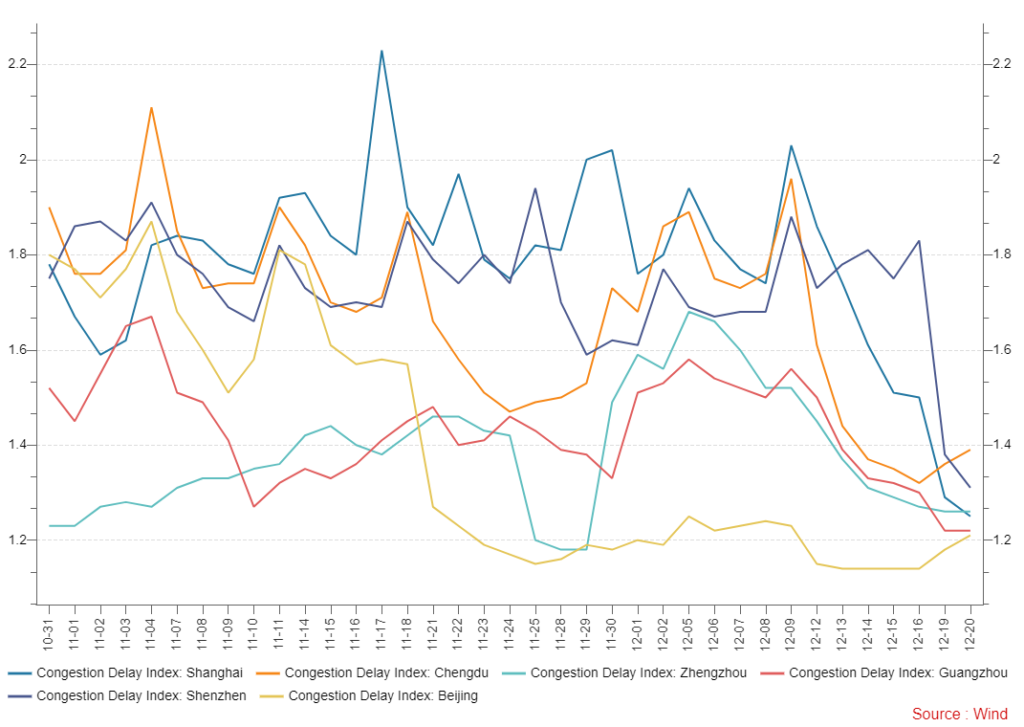

A few green shoots, but we are still in the thick of China’s COVID spike.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.98 versus 6.97 yesterday

- CNY per EUR 7.41 versus 7.40 yesterday

- Yield on 10-Year Government Bond 2.86% versus 2.87% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.03% yesterday

- Copper Price +0.74% overnight