BioNTech mRNA Vaccine Approved in Hong Kong, Week in Review

4 Min. Read Time

Week in Review

- Asian equities started the week lower as the Bank of Japan unexpectedly raised its yield ceiling on government bonds, but gained some ground later in the week as Hong Kong outperformed.

- Releases from China’s Central Economic Work Conference (CEWC) have been trickling in all week, noting a strong pro-growth orientation for China’s government going into 2023 with support measures for consumption, real estate, and electric vehicles (EVs) in the pipeline.

- The reality of reopening continued to take hold in many Chinese cities as many self-isolate during the winter season as COVID cases surge. Meanwhile, tourism stocks, among other reopening plays, continued to rally.

- We have confirmed that China has imported vaccines from BioNTech, meant for the use of foreigners residing in China, and Pfizer’s Paxlovid COVID treatment.

Friday’s Key News

Asian equities were down with an emphasis on growth stocks except for Malaysia and Thailand, following the US equity market’s steep decline yesterday. Volumes were light in Asia, unlike in the US yesterday. CNY was flat overnight, which we watch as a risk barometer.

Early afternoon, German pharma company BioNTech announced that the version of its mRNA vaccine produced by Fosun Pharma (ticker 600196 HK), which gained +3.84% overnight, has been approved in Hong Kong for use by those above the age of 12. Meanwhile, 11,000 doses of their mRNA vaccine arrived in Beijing for German citizens living in China. Remember that reforms in China are incremental, following the “test and expand” mantra. We know that this vaccine will likely be expanded to Mainland Chinese citizens, though it is hard to say exactly when. This development begs the question: where is Pfizer?

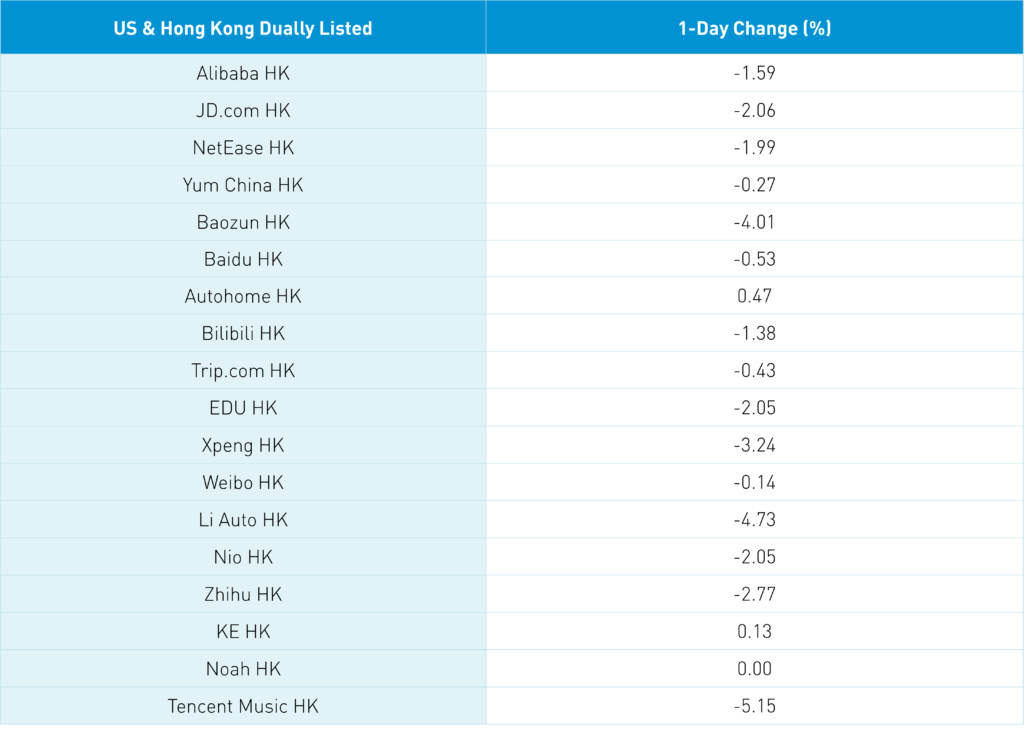

Hong Kong opened lower, and the Hang Seng closed down by -1.51% while the Hang Seng Tech Index fell -2.3% but managed to come back somewhat as Hong Kong’s most heavily traded stocks were Tencent, which fell -1.11%, Meituan, which fell -1.61%, and Alibaba, which fell -1.59%. 17% of Hong Kong’s Main Board volume was short, which is the highest level since the rally started. 29% and 24% of Tencent and JD.com’s volumes were short, though only 16% of Alibaba’s.

Healthcare was a top-performing sector in both Hong Kong, gaining +1.99%, and China, gaining +0.89%, as Western media is claiming that 18% of China’s population has been infected with COVID. A Mainland media source noted that the COVID wave should take two months. Our Major City Mobility Tracker indicates that there is a clear impact taking place. Meanwhile, the market continued to be focused on reopening as the first flight from Shanghai to Athens occurred yesterday while Hong Kong’s leader visits Beijing amidst talk of a potential dial-back in travel restrictions between Hong Kong and the Mainland.

Real estate was also a strong performer in both Hong Kong and Mainland China, though without any new news.

Foreign direct investment (FDI) is reported monthly, though only on a year-to-date (YTD) basis. YTD, FDI increased +9.9% versus 14.4% in October. The data would indicate that decoupling is not occurring.

Tim Ferriss interviewed Ed Thorp, who is famous for both blackjack and his hedge fund, twice on his podcast The Tim Ferriss Show, which I highly recommend. Mr. Thorp is highly schooled in mathematics, which led to his success in Las Vegas and running a hedge fund that predicted Warren Buffett’s success in the 1960s. He also discovered Bernie Madoff’s Ponzi scheme in the early 1990s. During the show, there was a discussion on inherent biases, one of which was failing to look at actual data as opposed to editorialization. That is kind of like what happened with today’s China FDI data as the Western media still preaches about decoupling.

The Hang Seng and Hang Seng Tech indexes fell -0.44% and -2.05%, respectively, on volume that was off -21.2% from yesterday, which is 64% of the 1-year average. 190 stocks advanced, while 288 stocks declined. Main Board short turnover declined -13.13% from yesterday, which is 63% of the 1-year average, as 17% of turnover was short. Value and growth factors were both down as small caps outpaced large caps. Healthcare and real estate were the only positive sectors, gaining +2% and +0.71%, respectively, while tech fell -2.09%, consumer discretionary fell -1.77%, and communication fell -1.3%. The top-performing subsectors were insurance, pharmaceuticals, and telecom, while autos, semiconductors, and household products were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $87 million worth of Hong Kong stocks, as Tencent was a moderate net buy, while Meituan and Kuaishou were moderate net sells.

Shanghai, Shenzhen, and the STAR Board closed lower by -0.28%, -0.28%, and -1.12%, respectively, on volume that decreased -11.43% from yesterday, which is 62% of the 1-year average. 1,972 stocks advanced, while 2,580 stocks declined. Value and growth factors were mixed as small caps outpaced large caps. The top-performing sectors were communication, which gained +2.32%, healthcare, which gained +0.91%, and consumer staples, which gained +0.35%. Meanwhile, consumer discretionary fell -1.29%, tech fell -1.01%, and industrials fell -0.93%. The top-performing subsectors were telecom, education, and software, while autos, power generation equipment, and semiconductors were among the worst. Northbound Stock Connect was closed. CNY was flat versus the US dollar. Treasury bonds rallied, and copper fell -0.74%.

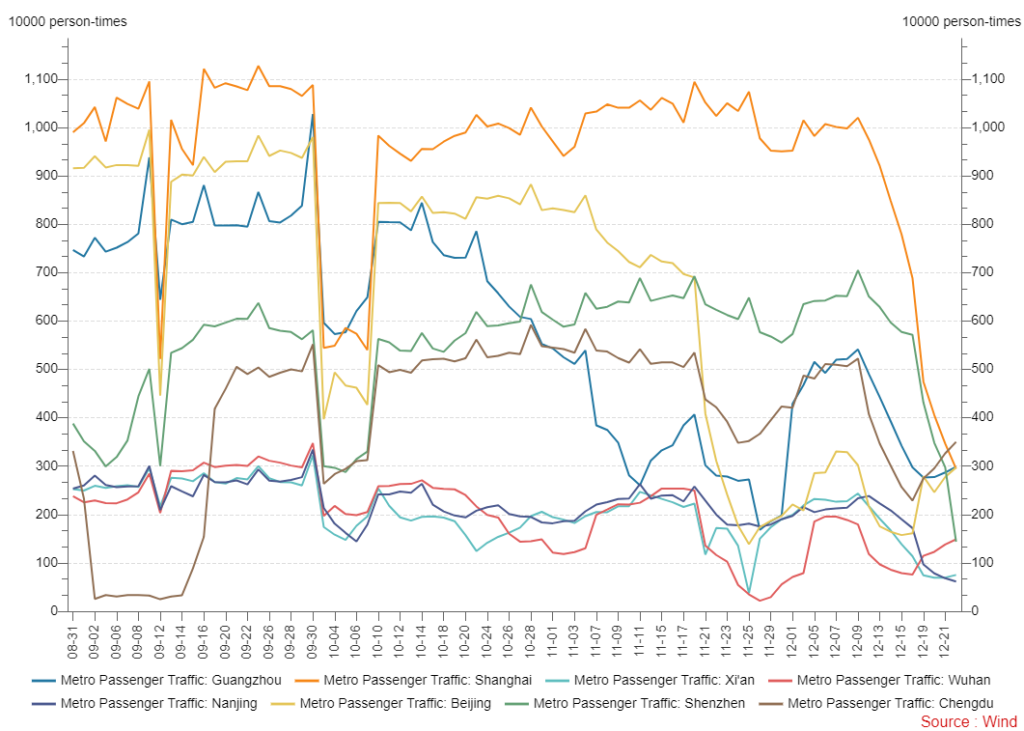

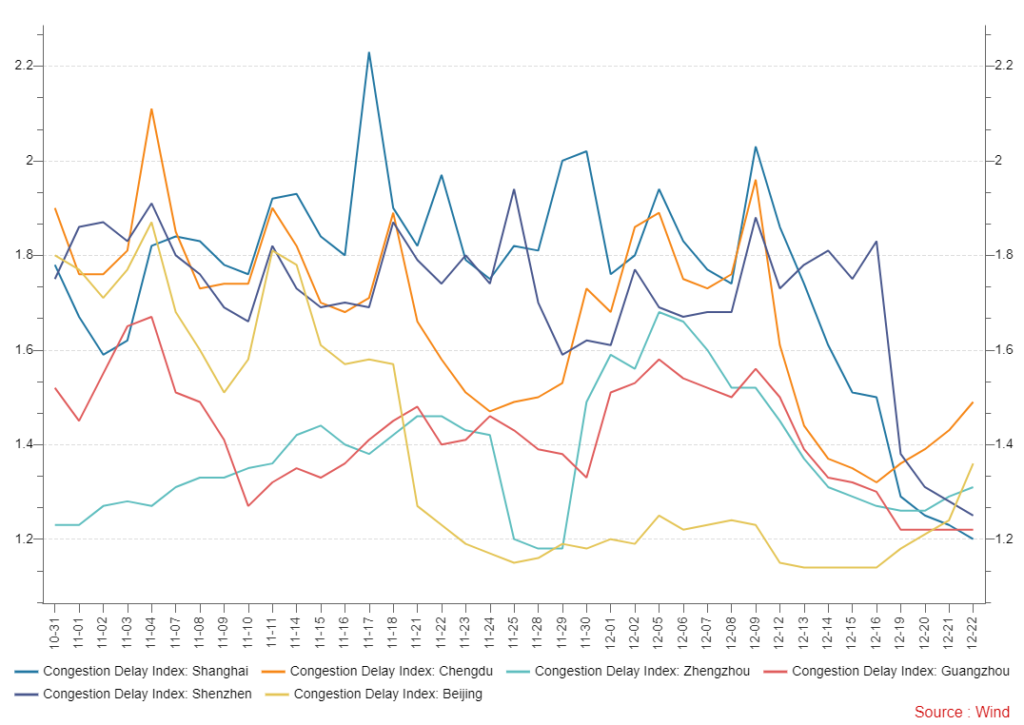

China Major City Mobility Tracker

Traffic trends appear to have bottomed for the most part, though metro usage is still anemic. China is a big country geographically, so we’ll see divergence across cities in different stages.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.99 versus 6.99 yesterday

- CNY per EUR 7.41 versus 7.40 yesterday

- Yield on 1-Day Government Bond 0.90% versus 0.90% yesterday

- Yield on 10-Year Government Bond 2.83% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 2.99% versus 3.01% yesterday

- Copper Price -0.74% overnight