CNY Ignores Western Headlines, Tencent Rises

2 Min. Read Time

| Upcoming Webinar |

| Join us on Thursday, January 12th for our webinar at 10 am EST: Back to Business for China & 2023 Outlook Click here to register. |

Key News

Similar to yesterday, North Asia was off, while South Asia managed small gains on light volumes following the US equity market sell-off yesterday.

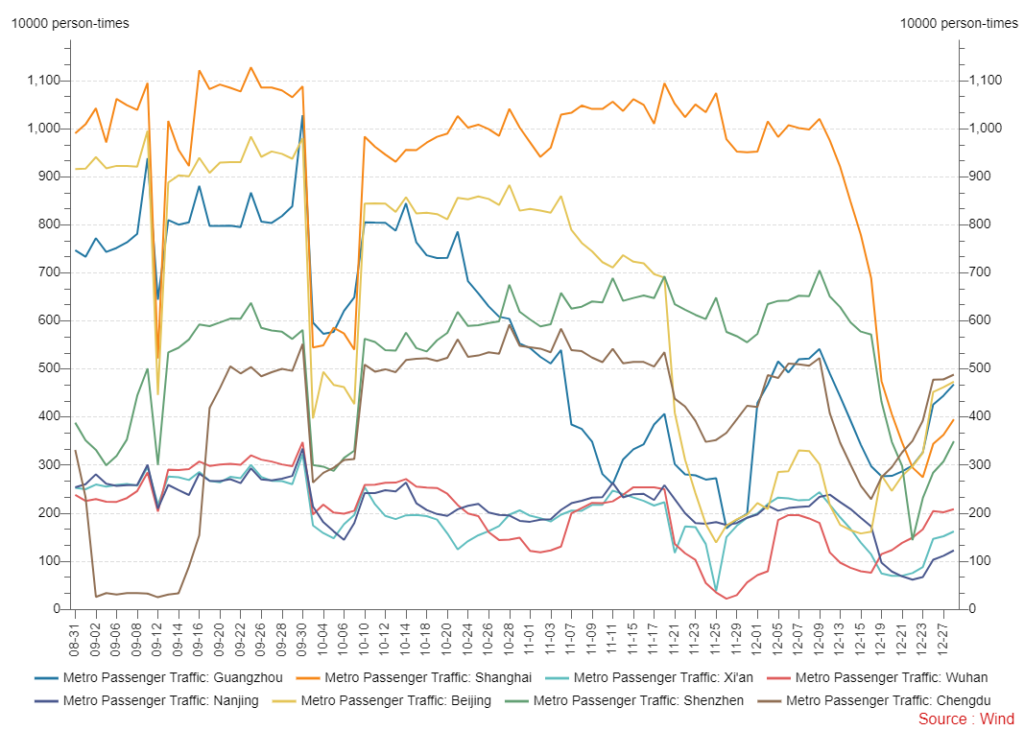

US tech weakness led by Apple’s fall yesterday weighed on growth stocks in the region, with South Korea hit harder than most. Apple’s bad showing had a knock-on effect on its Asia supplier ecosystem, similar to Tesla’s effect on Asia EVs yesterday. Western media headlines are screaming about the spread of COVID in China and outbound traveler testing. 100% COVID is spreading in China though thus far, it appears to be the omicron variant as our Mobility Tracker below continues to show a pick up in city activity. I would point out how stable CNY has been, which appreciated overnight versus the US dollar. If CNY isn’t freaking out, neither should you!

Hong Kong internet stocks were off though not nearly as much as their US ADRs yesterday, which should lead to a bounce back today. Tencent had a strong day, +2.76% following yesterday’s new game announcement though NetEase HK was off -2.88% in Hong Kong while online video plays were off with Bilibili HK -4.91% and Kuaishou -3.35%. Tencent had an even stronger day of net buying via Southbound Stock Connect than yesterday while the company continued to buy back stock. Alibaba HK was off -2.45% though the company announced a new CTO. Mainland markets were mixed as the Standing Committee announced a focus on employment in 2023, while the auto and EV industry received several positives from the Ministry of Commerce.

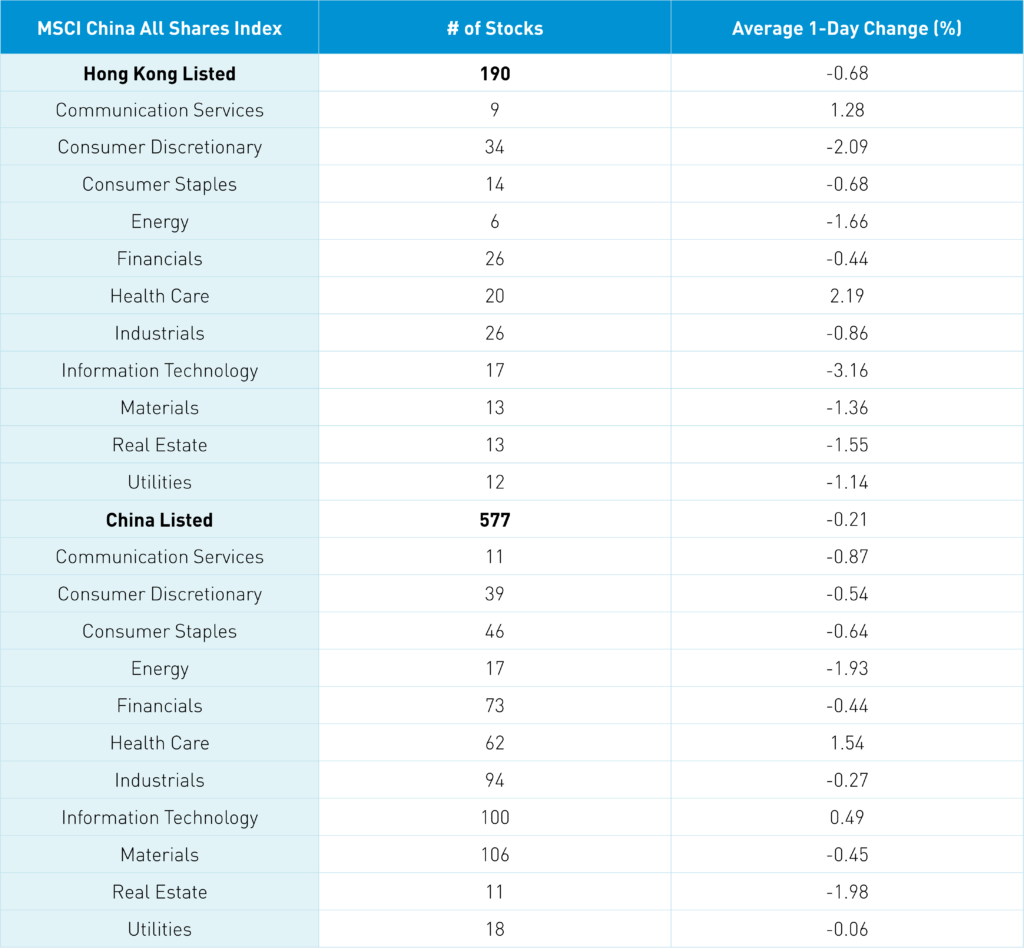

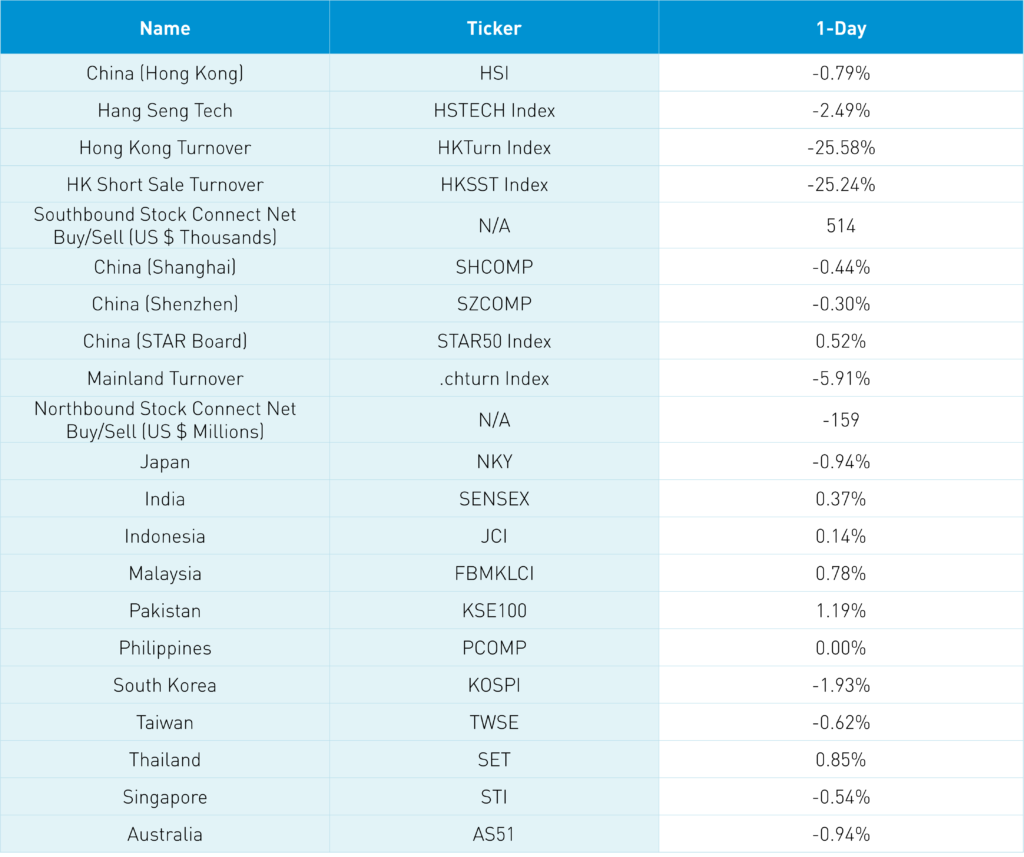

The Hang Seng and Hang Seng Tech fell -0.79% and -2.49% on volume, down -25.58% from yesterday, which is 73% of the 1-year average. 124 stocks advanced, while 373 declined. Main Board short turnover fell -25.21% from yesterday, which is 78% of the 1-year average, as 19% of the Main Board turnover was short turnover. Growth and value factors were mixed as large caps outperformed slightly versus small caps. Healthcare and communication were positive, +2.19% and +1.28%, while tech -3.16%, discretionary -2.09%, and energy -1.65%. The top sub-sectors were pharma, software, and household products, while technical hardware/equipment, semis, and retailers were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $514mm of Hong Kong stocks, with Tencent having an even strong day of net buying than yesterday; Meituan was a small net buy, and Kuaishou a small net sell.

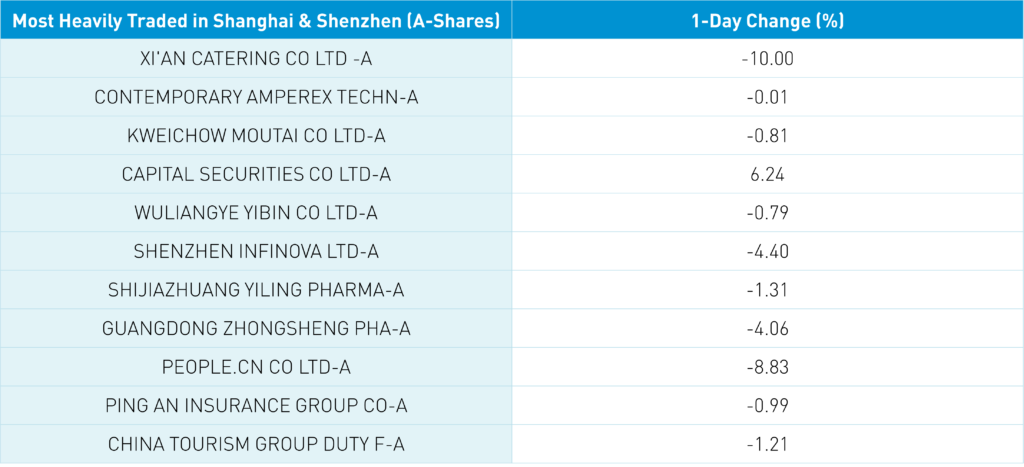

Shanghai, Shenzhen, and STAR Board were mixed -0.44%, -0.3%, and +0.52% on volume -5.91% from yesterday, which is 66% of the 1-year average. 1,491 stocks advanced, while 3,138 stocks declined. Growth factors outperformed value factors as small caps outperformed large caps. Healthcare and tech were the only positive sectors, +1.54%, and +0.49%, while real estate -1.98%, energy -1.93%, and communication -0.87%. The top sub-sectors were pharma, retailing, and aerospace, while real estate, coal, and oil/gas were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$159mm of Mainland stocks. CNY appreciated versus the US dollar +0.27% to 6.96, Treasury bonds rallied, and copper was off -0.3%.

Major Chinese City Mobility Tracker

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.96 versus 6.98 yesterday

- CNY per EUR 7.41 versus 7.43 yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.02% versus 3.03% yesterday

- Copper Price -0.30% overnight