Happy New Year As Electric Vehicle & Auto Companies Celebrate Policy Support, Week in Review

3 Min. Read Time

Week in Review

- Asian equities had a bumpy week as reopening, and the spread of COVID in China continued to capture headlines, and US equities came back from the Christmas holiday to declines.

- The National Health Commission announced Monday that inbound visitors to China will no longer be required to quarantine for five days at a government facility, but only three days at home beginning on January 8th. Meanwhile, outbound international travel from China appears to have picked up again.

- Multiple game approvals this week benefitted game developers, including Tencent and Meituan, as the former’s Hong Kong-listed shares saw heightened buying via Southbound Stock Connect.

Friday’s Key News

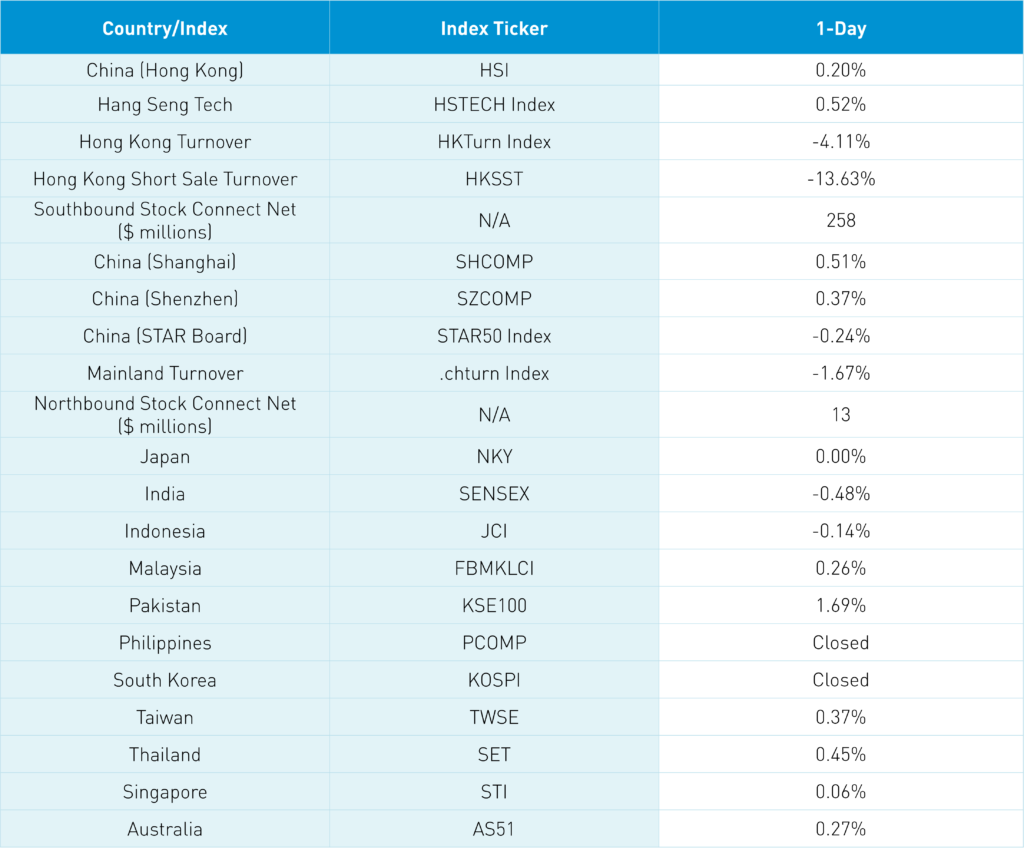

Asian equity markets ended the week and the year on a positive note though South Korea was closed for early New Year’s celebrations, and the Philippines was closed for Rizal Day, in memory of national hero Jose Rizal, who was executed on this date in 1896 for inciting a revolt against the Spanish.

CNY had a strong day, gaining nearly +1% versus the US dollar to close at 6.89 CNY per USD, while the Asia dollar index gained +0.57% and the Yen gained +0.85% versus the US dollar.

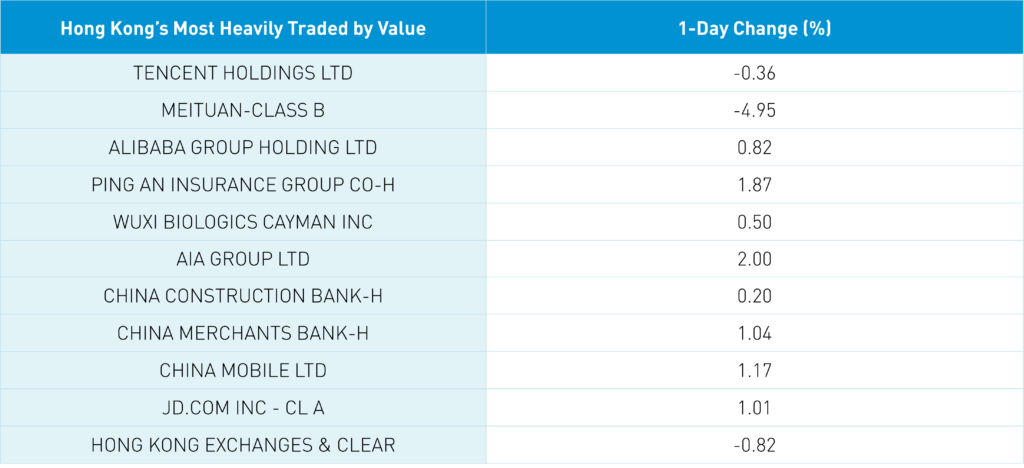

Hong Kong managed a small gain, though internet stocks did not gain nearly as much as their US-listed counterparts did yesterday. Unfortunately, US-listed China stocks are having a down day today. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.36% in another moderate net buying day from mainland investors, Meituan, which fell -4.95%, and Alibaba, which gained +0.82%.

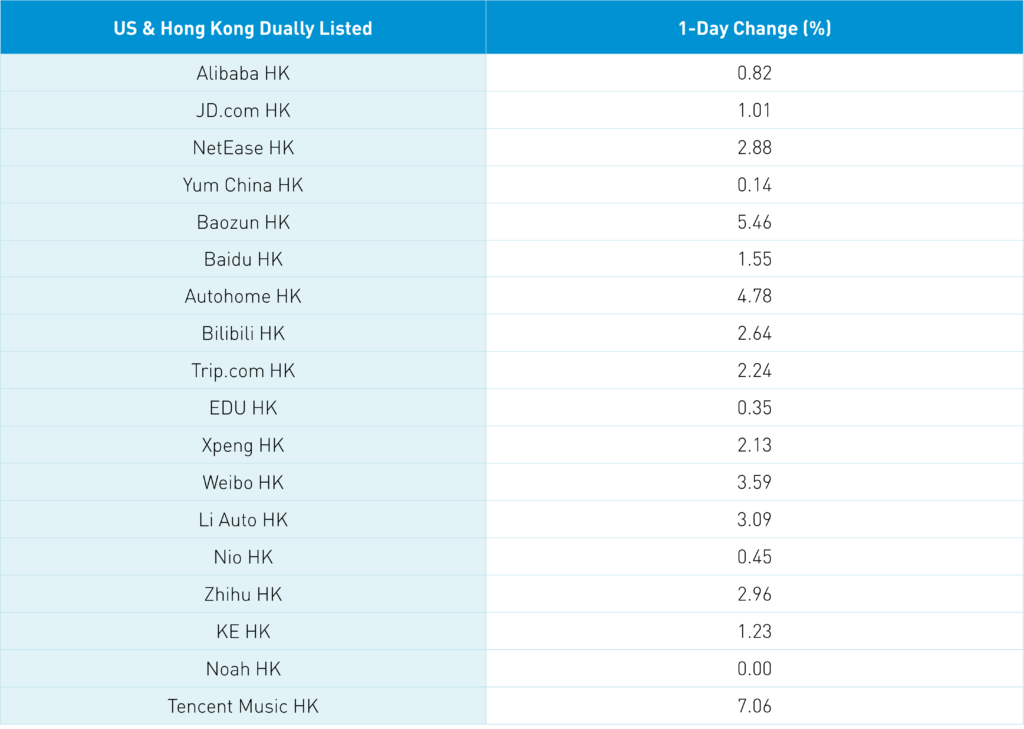

Autos & electric vehicles (EVs) had a good day following yesterday’s Ministry of Commerce report, with BYD +0.84%, Geely Auto +0.35%, NIO +0.45%, Li Auto +3.09%, and Xpeng +2.13%.

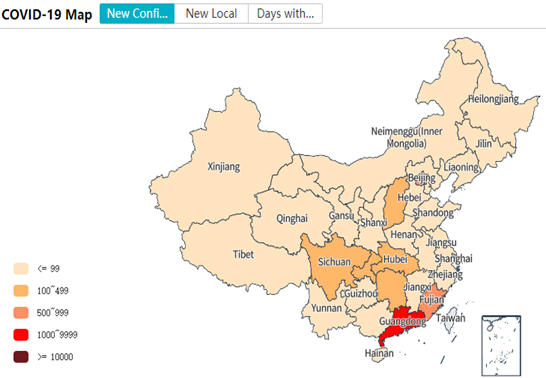

The Hang Seng couldn’t close above the 20,000 level. Meanwhile, real estate was the top-performing sector in Hong Kong, gaining +2.65% and +1.52% in China on supportive comments from the PBOC. Asia’s US dollar high-yield bond market is a great way to play this rebound, in my opinion, though I have very few co-investors! Hong Kong short sellers have been relatively quiet over the last two months, though we’ve seen a small uptick in activity over the last week. Mainland China posted small gains on little news, as all sectors were up for the day. The COVID outbreak is still quite fierce in Southern China as we added a map showing new Covid cases while the situation moderates in Northern China.

How are you positioned going into 2023? According to Bloomberg’s poll of economists, China’s GDP is forecasted to be 4.8% with a 2.3% CPI, while the US GDP forecast is 0.3% with a 4% CPI. According to Steve Holden’s Copley Fund Research, “Over the past three quarters, global equity managers have been underweight China. Average weights are sitting at the bottom of the 10-year range, with 18% of funds holding no exposure at all.” According to EPFR data, active EM funds had a 2.4% underweight to China as of the end of November. The pain trade is higher!

Happy New Year!

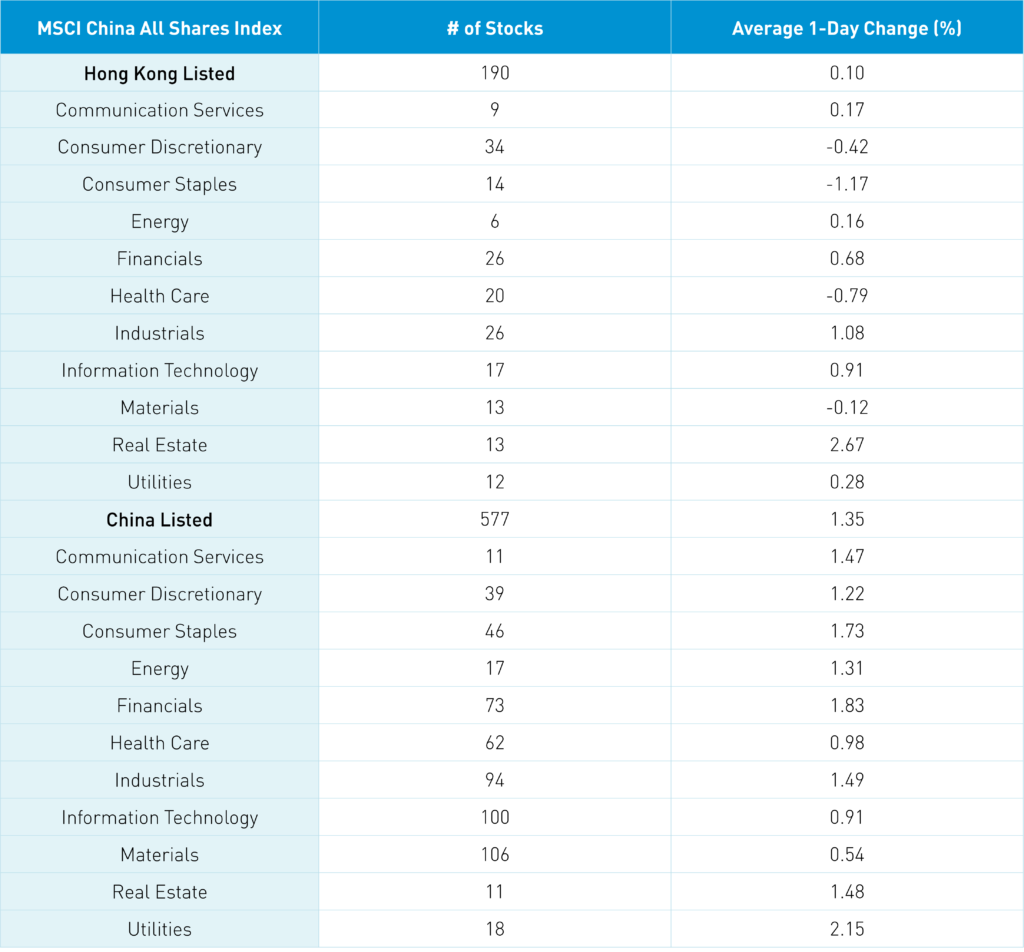

The Hang Seng and Hang Seng Tech indexes gained +0.2% and +0.52%, respectively, on volume that fell -4.11% from yesterday, which is 70% of the 1-year average. 353 stocks advanced, while 136 stocks declined. Main Board short selling turnover declined -13.63% from yesterday, which is 67% of the 1-year average as 17% of turnover was short turnover. Growth and value factors were mixed as small caps outpaced large caps. The top-performing sectors were real estate, which gained +2.67%, industrials, which gained +1.08%, and tech, which gained +0.91%. Meanwhile, consumer staples fell -1.17%, healthcare fell -0.79%, and consumer discretionary fell -0.42%. The top-performing subsectors were media, food/staples, and insurance, while retail, food/beverage/tobacco, and pharmaceuticals were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a healthy $849 million worth of Hong Kong stocks as Tencent was a moderate net buy, Kuaishou was a small net buy, and Meituan was a small net sell.

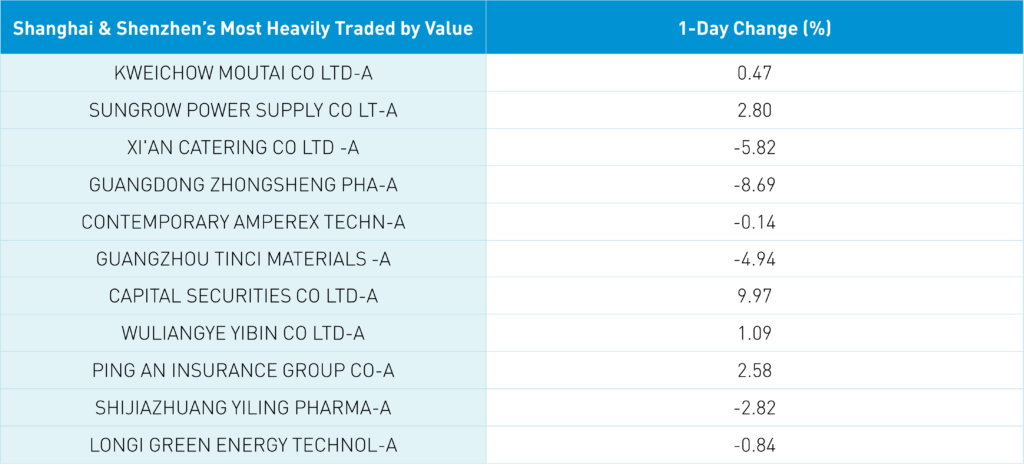

Shanghai, Shenzhen, and the STAR Board converged to close +0.51%, +0.37%, and -0.24%, respectively, on volume that fell -1.67% from yesterday, which is 65% of the 1-year average. 3,190 stocks advanced, while 1,399 stocks declined. Value factors outperformed growth factors, while large caps outperformed small caps. All sectors were positive as utilities gained +2.15%, financials gained +1.82%, and consumer staples gained +1.73%. The top performing subsectors were insurance, cultural media, and internet, while fine chemicals, base metals, and telecom were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $13 million worth of Mainland stocks. CNY had a strong day versus the US dollar, gaining +0.95% to close at 6.90 CNY per USD, the treasury curve flattened slightly, and copper fell -0.3%.

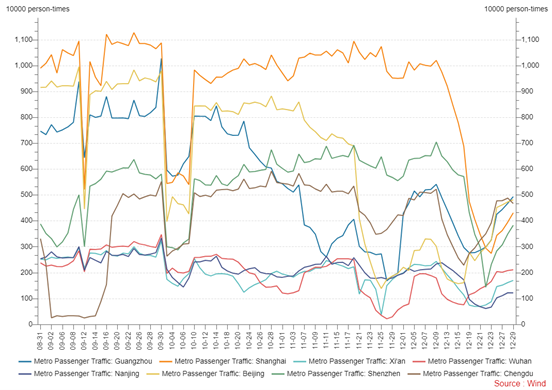

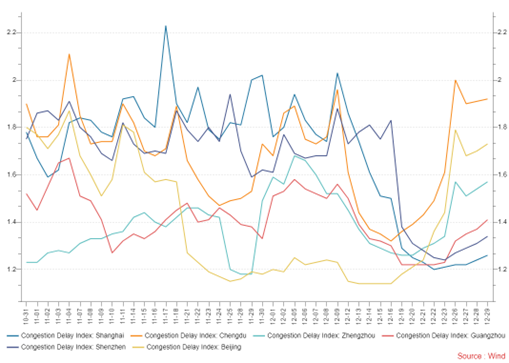

Major Chinese City Mobility Tracker

The uptrend in traffic is firmly in place, while subway usage comes back slower. The outbreak in Southern China continues while the situation improves in Northern China.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.90 versus 6.96 yesterday

- CNY per EUR 7.36 versus 7.42 yesterday

- Yield on 1-Day Government Bond 1.05% versus 0.72% yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.84% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.02% yesterday

- Copper Price -0.30% overnight