Alibaba’s Ant Capital Raise, Real Estate Rises on Policy Support

3 Min. Read Time

Key News

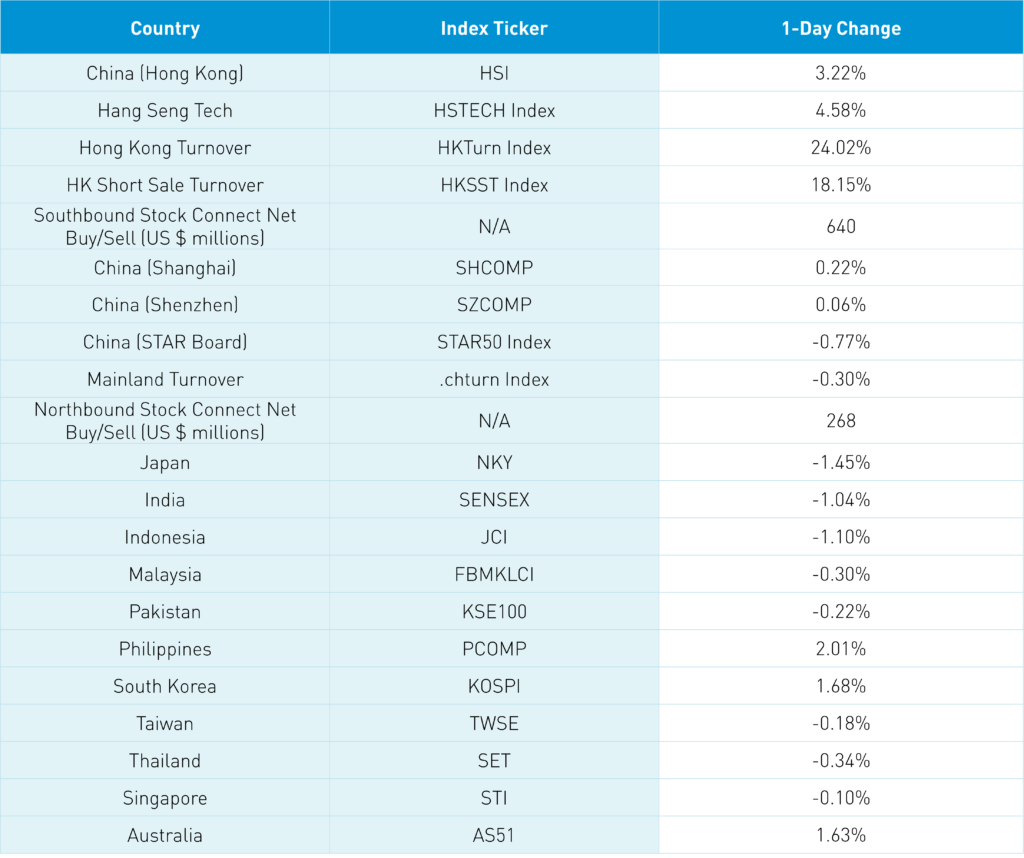

Asian equity markets were mixed as Hong Kong outperformed. South Korea, the Philippines, and Australia outperformed while Japan, India, and Indonesia underperformed.

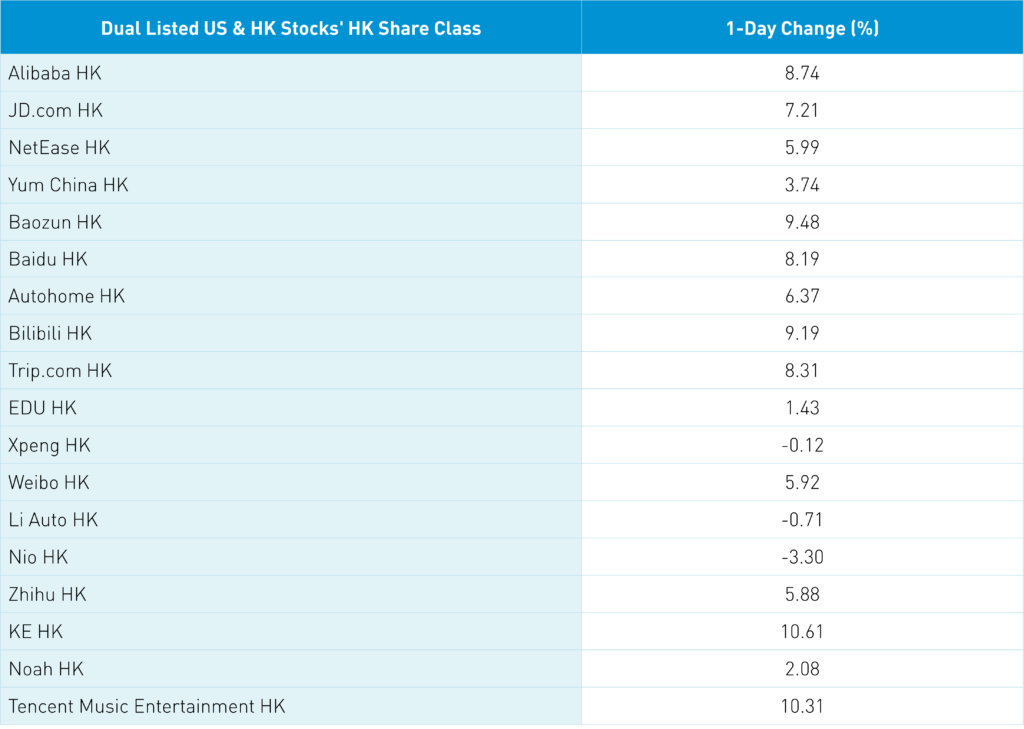

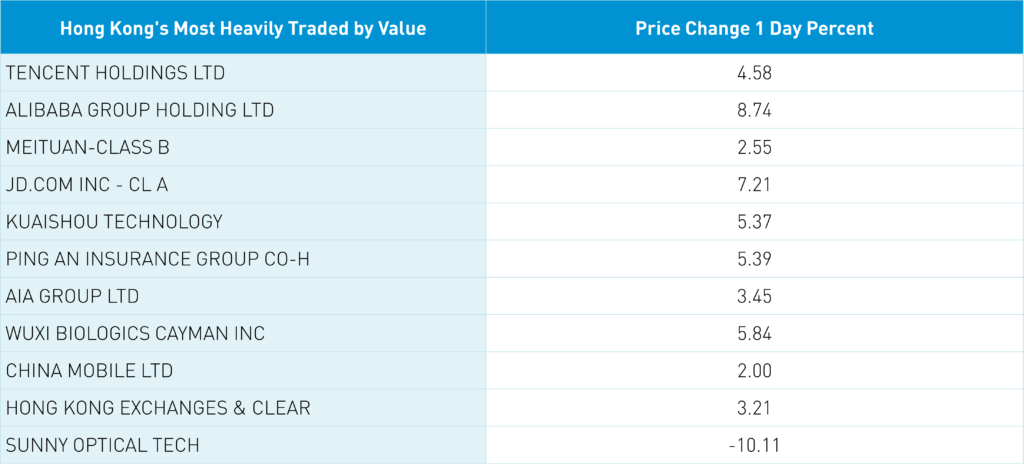

We knew that Hong Kong was going to have a good day after a strong day in US listed China ADRs despite a weak US equity market. There was more than one catalyst today though Alibaba’s Ant Group being approved by the China Banking and Insurance Regulatory Commission (CBIRC) to raise RMB 18.5B ($2.7B) for their consumer finance unit is garnering significant attention. Half of the investment capital will be coming from Ant with the remaining coming from local Chinese investors. China’s internet regulatory cycle has been over for quite some time though so skeptics should put a nail in that coffin. Following the bouncing ball, could an IPO be next? Would seem like logical next step. Hong Kong’s most heavily traded were Tencent +4.58%, Alibaba HK +8.74%, Meituan +2.5%, JD.com HK +7.21%, and Kuaishou +5.37%.

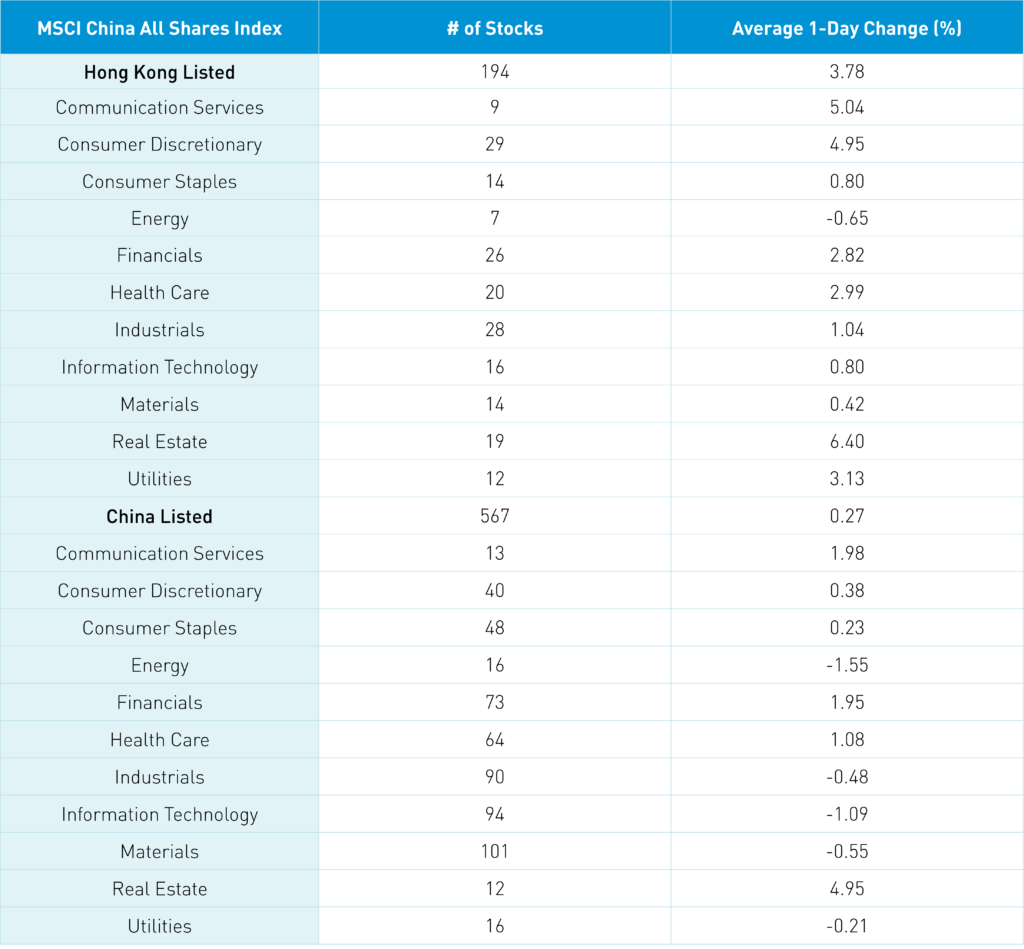

Today’s best performing sector in both Hong Kong +6.4% and China +4.89% was real estate after policy supporting property developers was announced by the Financial Stability and Development Committee which oversees financial regulators. The objective appears to push sales higher by supporting developers financially. Another positive that garnered attention in China more so than outside of China was from the Ministry of Finance’s Liu Kun who reiterated economic support through fiscal deficit and monetary support. He was quoted in Mainland media as stating “…that expanding fiscal policies includes efforts to coordinate the fiscal revenue, deficit, and interest subsidies and appropriately increase fiscal spending.” Remember central banks globally are tightening while China is easing.

Reopening plays were strong as traffic and subway usage rebounds after the New Year’s holiday as COVID is clearly all over China. Mainland investors bought a healthy $640 million of Hong Kong stocks today with Kuaishou being a strong net buy today. Shanghai and Shenzhen posted modest gains of +0.22% and +0.06% though CNY gained +0.5% versus the US dollar to close at 6.88. If you followed CNY, our favorite risk barometer, you didn’t get shaken out of the rebound by Western media’s negative coverage of China’s reopening and COVID spread. Apple’s China ecosystem was weak in both Hong Kong with Sunny Optical HK -10.11% and in China with Luxshare Precision -9.99% as the company’s stock falls. Tesla’s poor performance also weighed on the China EV and clean tech sector as its stock slides. Tesla’s declining market share in China hasn’t garnered much attention, though one could argue it is the canary in the coal mine. Hat tip to our friend Matt for pointing this out to us.

I stumbled across an interesting headline from an Asia media source titled “Dollar’s demise about to explode Asia’s 2023” followed by “Negative growth, high inflation, unsustainable debt and poison politics in the US will all drive investors to dump the dollar”. Wow! Not a view highlighted by the US financial media is it? Everything is about an equity rebound and which stocks to buy on the dip. I am not rooting for a US stock market fall. I point this out as the US is 61% of the MSCI All Country World Index (as of end of November) which is a very high weight after a strong decade of performance. Are investors positioned for the potential outperformance of non-US equities? Global funds remain underweight to China, which could make the pain trade higher.

Hang Seng and Hang Seng Tech gained +3.22% and +4.58% respectively on volume +24.02% from yesterday which is 119% of the 1-year average. 421 stocks advanced while 82 stocks declined. Main Board short turnover increased +18.08% from yesterday which is 106% of the 1-year average as 15% of turnover was short turnover. Growth factors outpaced value factors as small caps outperformed large caps. Top sectors were real estate +6.4%, communication +5.04%, and discretionary +4.95% while energy was the only negative sector down-0.65%. Top sub-sectors were media, retailing, and software while energy and technical hardware were the only negative sectors. Southbound Stock Connect volumes were moderate/high as Mainland investors bought $640 million of Hong Kong stocks with Kuaishou a large net buy, Tencent a moderate net buy, and Meituan a small net buy.

Shanghai, Shenzhen, and STAR Board were mixed +0.22%, +0.06% and -0.77% on volume -0.3% from yesterday which is 85% of the 1-year average. 3,766 stocks advanced while 1,794 stocks declined. Top sectors were real estate up +4.93%, communication gaining +1.96%, and financials finishing higher +1.93% while energy fell -1.57%, tech finished lower -1.1%, and materials was down -0.57%. Top sub-sectors were household products, forest industry, and paper industry while coal, power generation, and electric power were among the worst. Northbound Stock Connect volumes were light/moderate as foreign investors bought $268 million of Mainland stocks. CNY had a strong day +0.5% versus the US dollar closing at 6.88, Treasury bonds rallied, and copper hit for -0.96%.

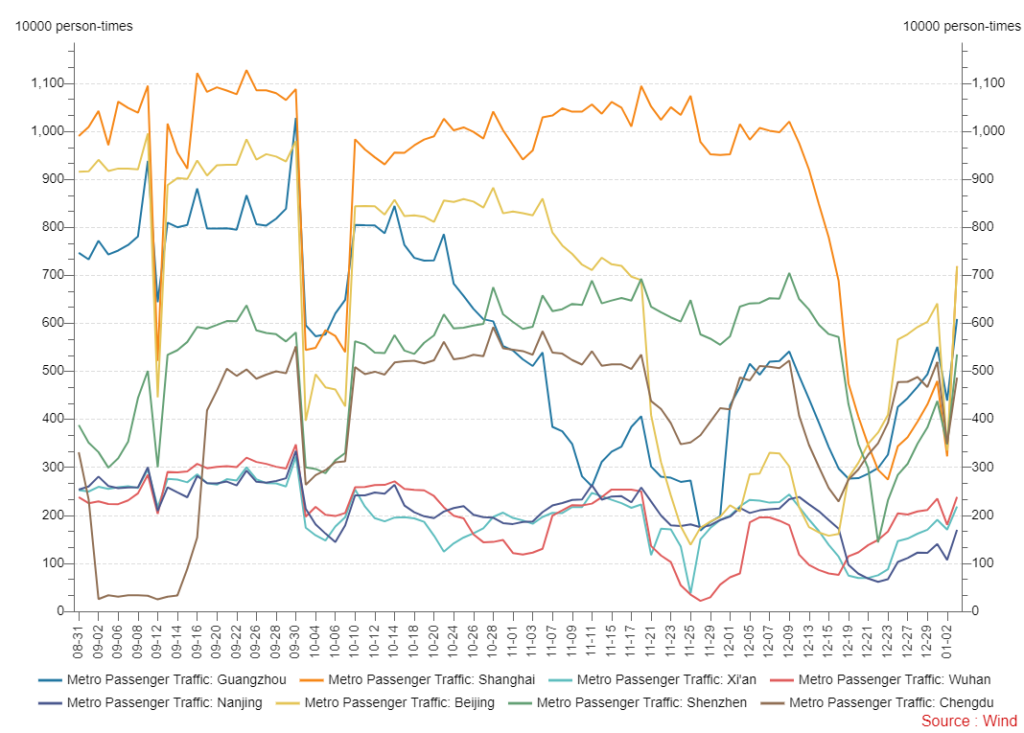

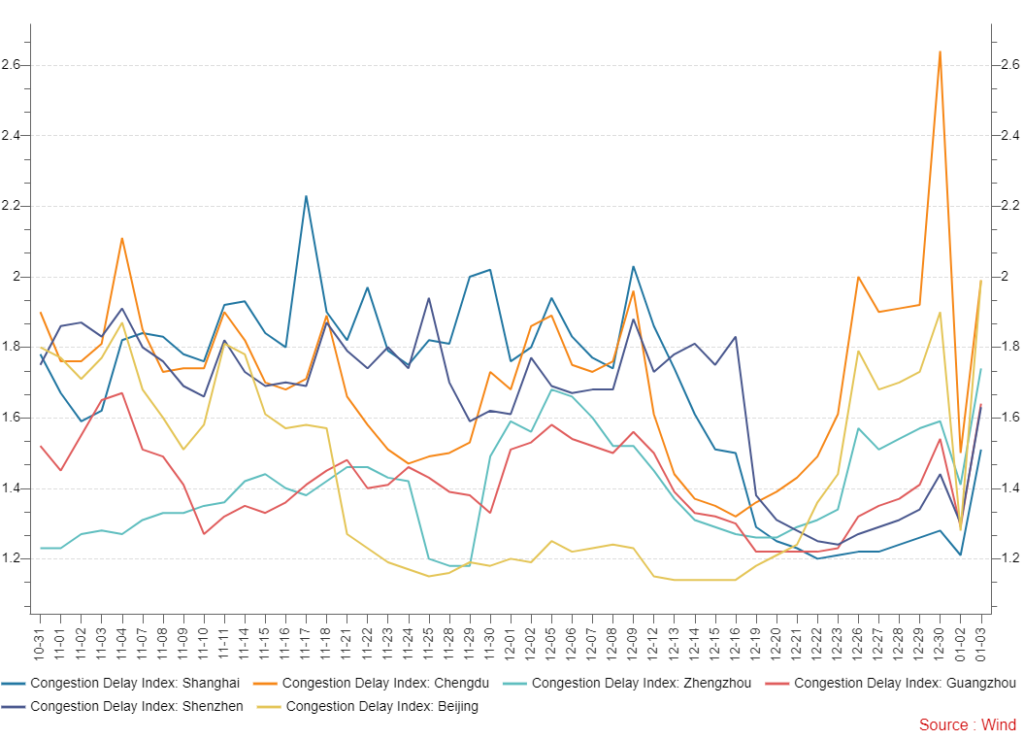

Major Chinese City Mobility Tracker

Post New Year’s rebound continues as folks head back to work. 100% COVID is in China, though it is a big country so where cities are in their cycle is varied. Key observation is the rebound is occurring. Yes, knocking on wood.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.91 Yesterday

- CNY per EUR 7.29 versus 7.28 Yesterday

- Yield on 10-Year Government Bond 2.81% versus 2.82% Yesterday

- Yield on 10-Year China Development Bank Bond 2.94% versus 2.97% Yesterday

- Copper Price -0.96% overnight