The Importance of Vice Premier Liu He’s Davos Speech

5 Min. Read Time

Key News

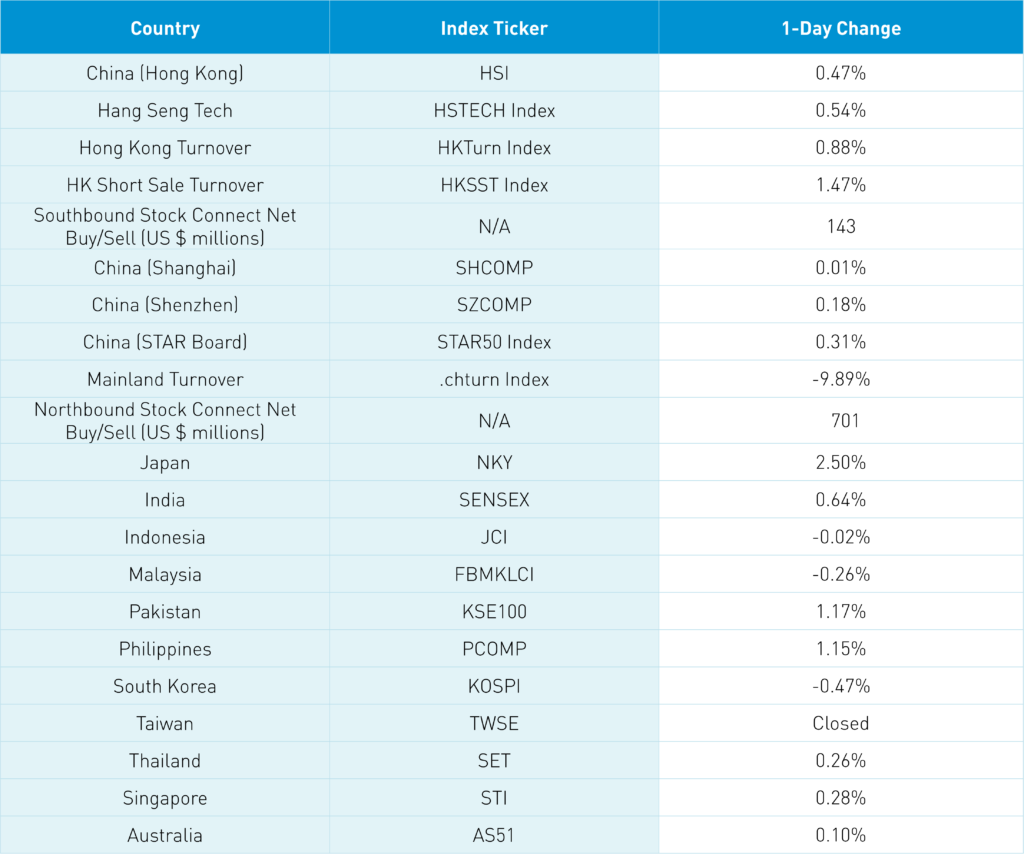

Asian stock markets were largely higher as Japan outperformed as the BoJ reaffirmed its commitment to yield curve control. US-listed Chinese stocks were down yesterday as the Renminbi weakened, which was the only explanation for the steep sell-off.

Profit taking after a strong move along with choppiness and volatility as volumes fall in advance of China’s weeklong holiday next week were likely factors leading to the slight decline as well. Remember that many institutional investors are underweighting the space, which means pullbacks like yesterday are an opportunity for them to rectify their underinvestment.

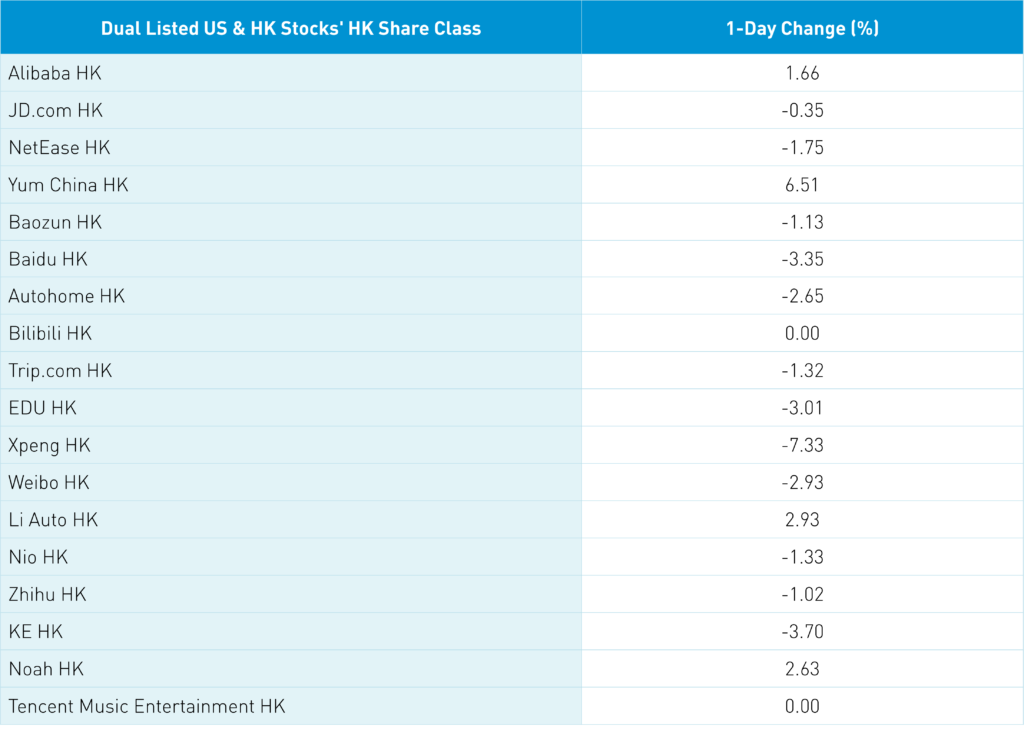

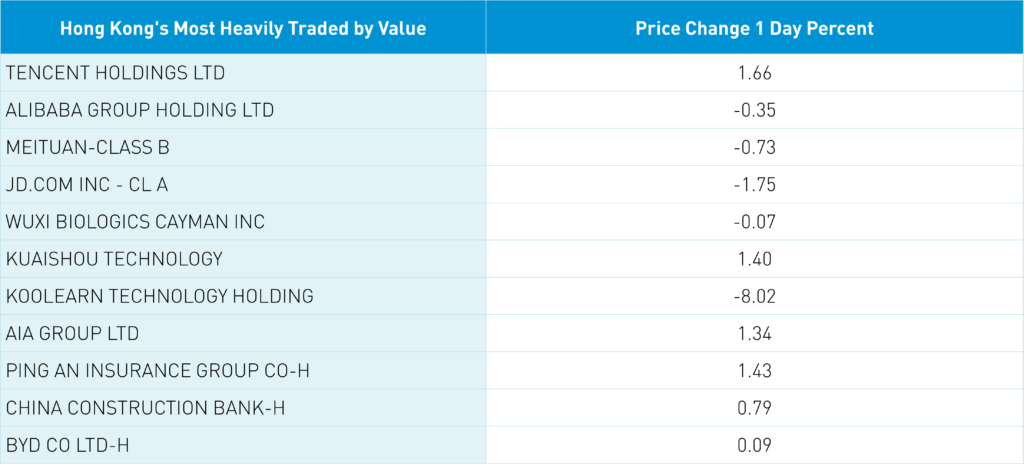

Overnight Tencent gained +1.66% and NetEase gained +6.51% on new online game approvals while Hong Kong-listed internet stocks were down, but not nearly as much as their US counterparts' fall yesterday. Alibaba HK was off -0.35% overnight versus the US ADR -1.56%, JD.com HK -1.75% versus US ADR -5.72%, Baidu HK -2.65% versus the US ADR -6.02%, which is why we should see a rebound in US trading this morning. We also had CNY appreciate +0.27% versus the US dollar to 6.75 CNY per USD from 6.78 yesterday, which should be a tailwind for the ADRs.

Hong Kong-listed electric vehicle stocks were off except for BYD, which gained +0.09%. Hong Kong short sellers have been fairly quiet of late.

Mainland China managed small gains as the Vice Premier’s speech at the World Economic Forum in Davos garnered significant attention from Mainland financial media. In 2023, the Vice Premier stated China will “…continue to implement a proactive fiscal policy and a prudent monetary policy…focus on expanding domestic demand…welcome more foreign investment to China, and prevent and defuse economic and financial risks.” Sounds good to me! The government will “…unswervingly support the development and growth of the private economy…persist in opening up to the outside world…”. The speech included a deep dive into real estate due to its importance to the economy as “loans related to the real estate industry account for nearly 40% of bank credit, real estate related income accounts for 50% of local comprehensive financial resources, and real estate accounts for 60% of urban residents’ assets. Since the second half of 2021, China’s real estate market has experienced a sharp decline in prices and sales. Real estate companies generally have poor liquidity and deteriorated balance sheets, and induvial leading companies are facing major risks.”

It is not surprising that real estate stocks were off in both Mainland China and Hong Kong, though the speech then pivots to the measures to prevent real estate from becoming a financial crisis. The speech focuses on domestic consumption and addresses foreign concerns on common prosperity, which he said was not “welfarism”. He ends by speaking to the government’s effort to be a global citizen.

Today, the Vice Premier will meet with Treasury Secretary Yellen in Zurich, while Secretary of State Blinken is rumored to be visiting China in the first week of February.

Foreign investors added $701 million in Mainland stocks via Northbound Stock Connect for the eleventh straight day as there has only been one outflow day in 2023. Clearly, foreign investors are pivoting and raising their China investments. Are you? Mainland China's stock market could increase in value based on what Chinese investors think about China, which is likely a positive view following the resolution of Zero COVID and real estate issues. Foreign investments in Hong Kong and US-listed Chinese stocks are likely to increase thanks to not only the resolution of these two issues, but also an improvement in the US-China political relationship. Remember our "Post Party Congress Policy Pivot on the Big Three: US-China political relationship, zero covid, and real estate."

Yesterday, we reported that retail sales were down by -1.8% in December and -0.2% year-over-year for 2022. Within the data is an interesting insight if you dug into the report as online retail sales increased by 4.4% in December and 6.2% in 2022. Excluding auto sales and restaurants, China’s percentage of retail sales that occurred online increased to 34.2% from 32.3% in 2022. Impressive!

I just finished Morgan Housel’s book The Psychology of Money. I recommend it because it is an easy and digestible read lacking in jargon. It also uses interesting and relatable anecdotes to get points across and reiterates key actionable investing advice. The unbreakable portfolio and compounding messages were great reminders for me, though I very much enjoyed Chapter 17 "The Power of Pessimism" and Chapter 18 "When You’ll Believe in Anything." The chapters are quick and direct so don’t be intimidated by the high number of chapters, as the book is only 238 pages. The Power of Pessimism notes how the media and our brains often focus on the negatives rather than the positives, progress is slow and difficult to measure but setbacks are fast. We can all relate to the idea that “…pessimists often extrapolate present trends without accounting for how markets adapt.” Human beings are smart, problem solvers literally built on evolving! Think about all of the headlines on China’s population decline, which assume that the Chinese government will sit around and do nothing. That is unlikely! Chapter 18 has the great sub-title “Appealing fictions, and why stories are more powerful than statistics.” We find narratives and data points to reinforce rather than oppose or challenge our beliefs. Why? Because it would be hard work to challenge our views and do the research. So, why bother? These chapters resonate with me based on my work in China, as I’m sure you understand. It is a good read regardless of your China opinions!

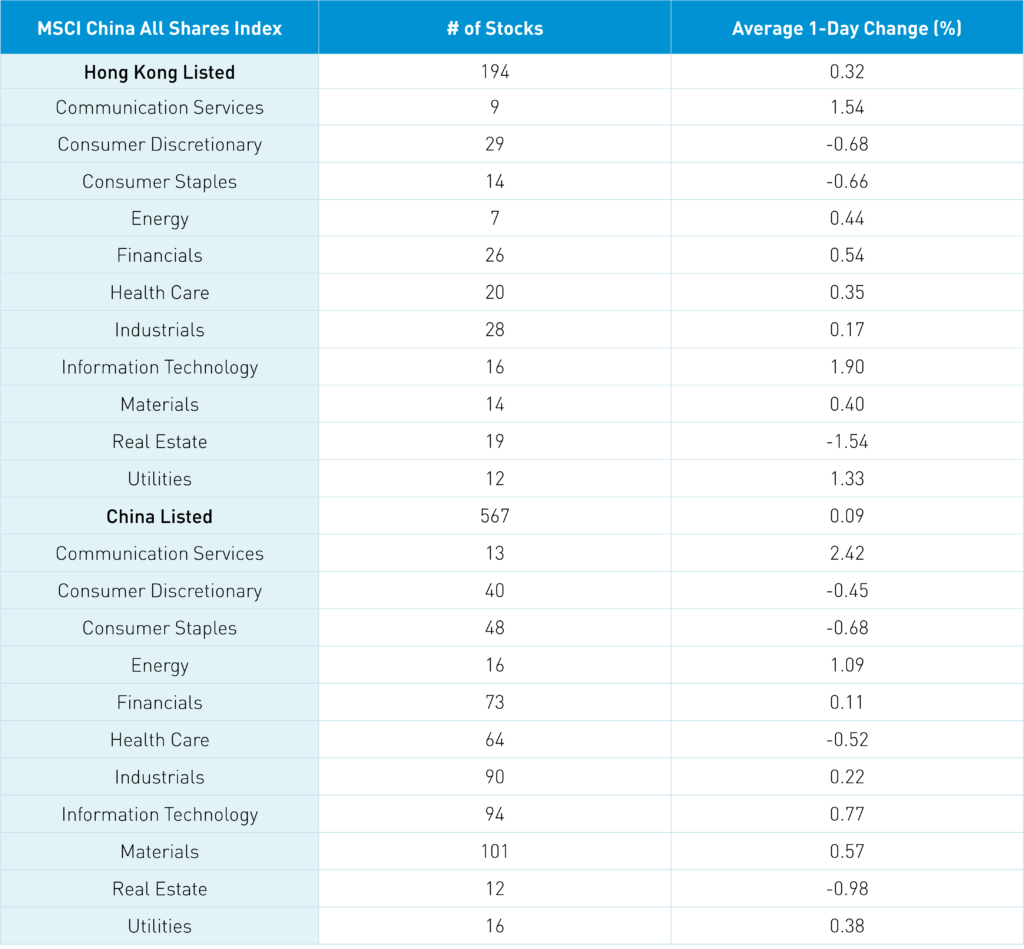

The Hang Seng and Hang Seng Tech gained +0.47% and +0.54% on volume +0.88% from yesterday which is 101% of the 1-year average. 250 stocks advanced while 229 stocks declined. Main Board short turnover increased +1.36% from yesterday which is 89% of the 1-year average as 15% of turnover was short turnover. Value and growth factors had a good day as large caps outpaced smalls significantly. Top sectors were tech +1.9%, communication +1.54% and utilities +1.33% while real estate -1.54%, discretionary -0.68% and staples -0.66%. Top sub-sectors were semis, technical hardware/equipment and software while retailing, business services and food/beverage/tobacco were among the worst. Southbound Stock Connect volumes were light as mainland investors bought $143mm of HK stocks with Meituan a moderate net buy, Tencent a small net and Kuiashou a small net sell.

Shanghai, Shenzhen and STAR Board gained +0.01%, +0.18% and +0.31% on volume -9.89% from yesterday which is 70% of the 1-year average. 2,894 stocks advanced while 1,638 declined. Growth and value factors were mixed as small caps outpaced large caps. Top sectors were communication +2.42%, energy +1.09% and tech +0.77% while real estate -0.98%,staples -0.67% and healthcare -0.51%. Top subsectors were diversified financials, software and telecom while forest industry, food and household products were among the worst. Northbound Stock Connect volumes were light/moderate as foreign investors bought $701mm of mainland stocks. CNY gained +0.27% versus the US dollar to close at 6.75, Treasury curve steeepend and Shanghai copper gained +1.66%.

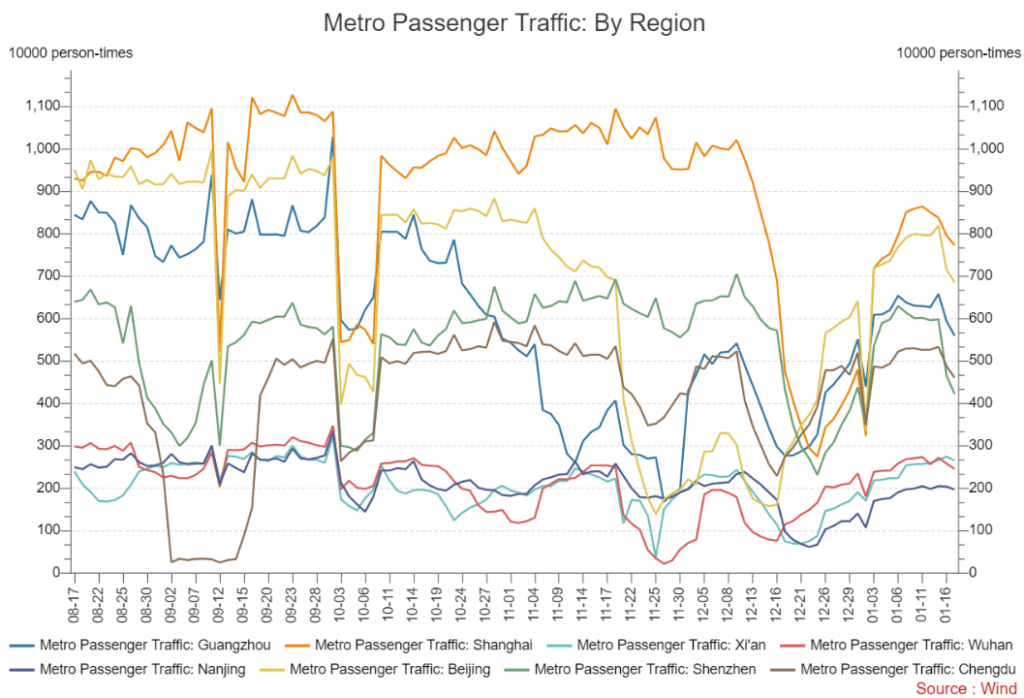

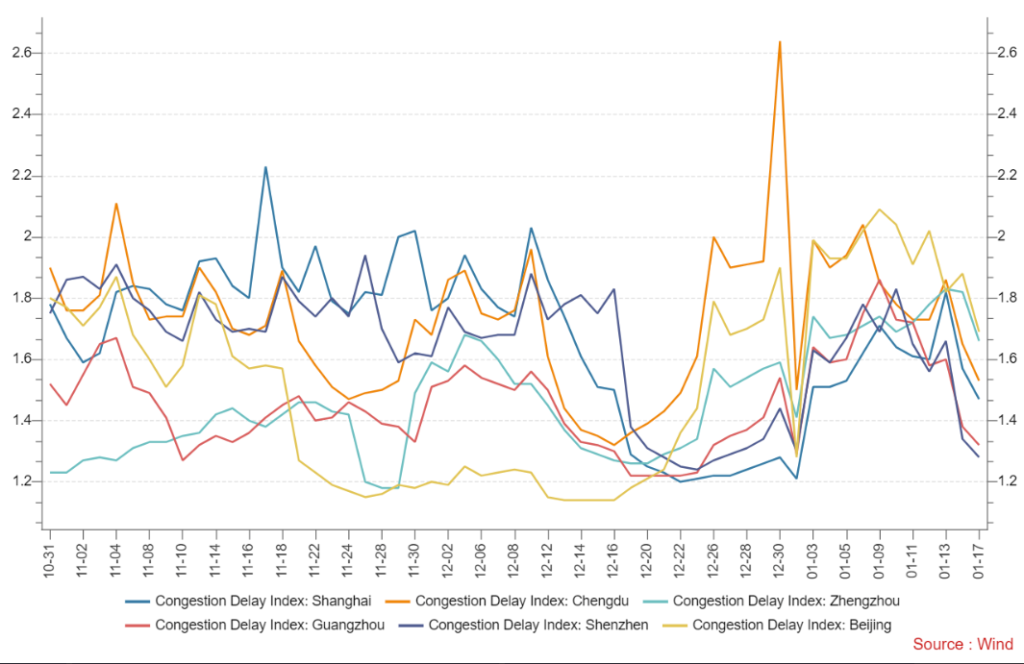

Major Chinese City Mobility Tracker

Traffic and metro usage is falling as citizens head out for their Chinese New Year vacations.

Last Night's Performance

Last Night's Exchange Rates, Prices, & YIelds

- CNY per USD 6.75 versus 6.78 yesterday

- CNY per EUR 7.32 versus 7.35 yesterday

- Yield on 10-Year Government Bond 2.92% versus 2.90% yesterday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.06% yesterday

- Copper Price +1.66% overnight