Yum China Provides a Look at China’s Consumer, Tik Tok Flip Flops on Food Delivery Launch

3 Min. Read Time

Key News

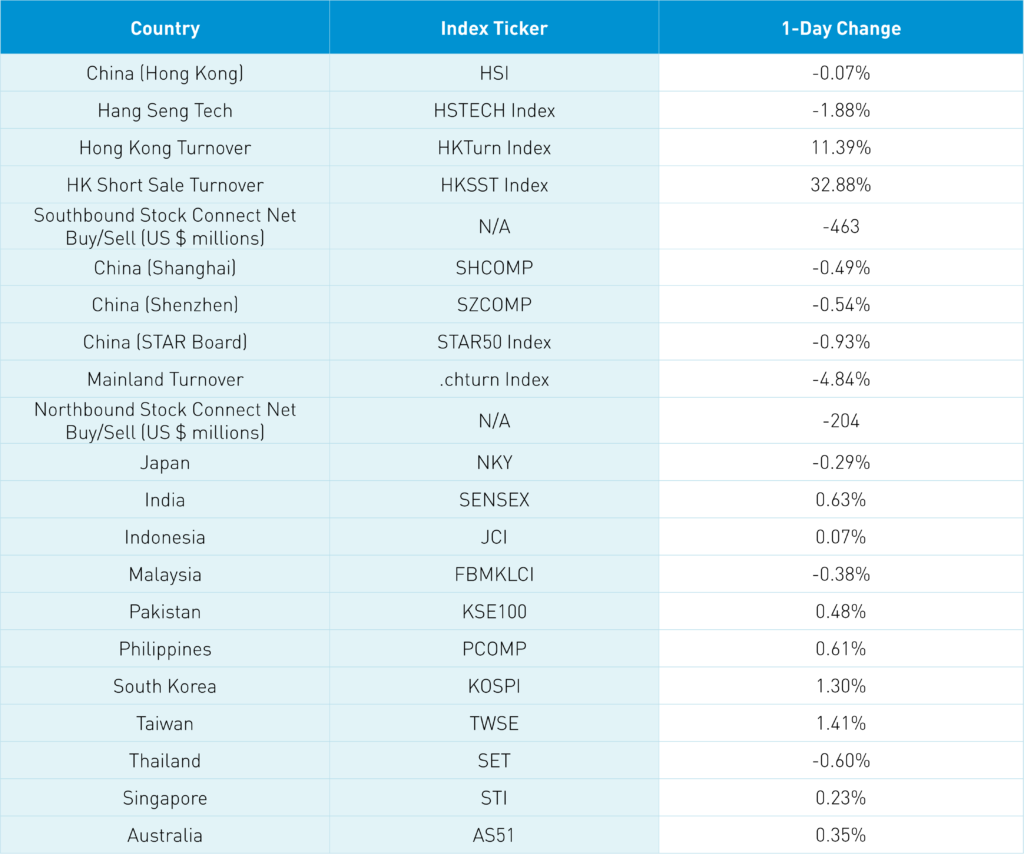

Asian equities were largely higher overnight as Taiwan and South Korea outperformed while China, Hong Kong, Japan, Malaysia, and Thailand posted declines.

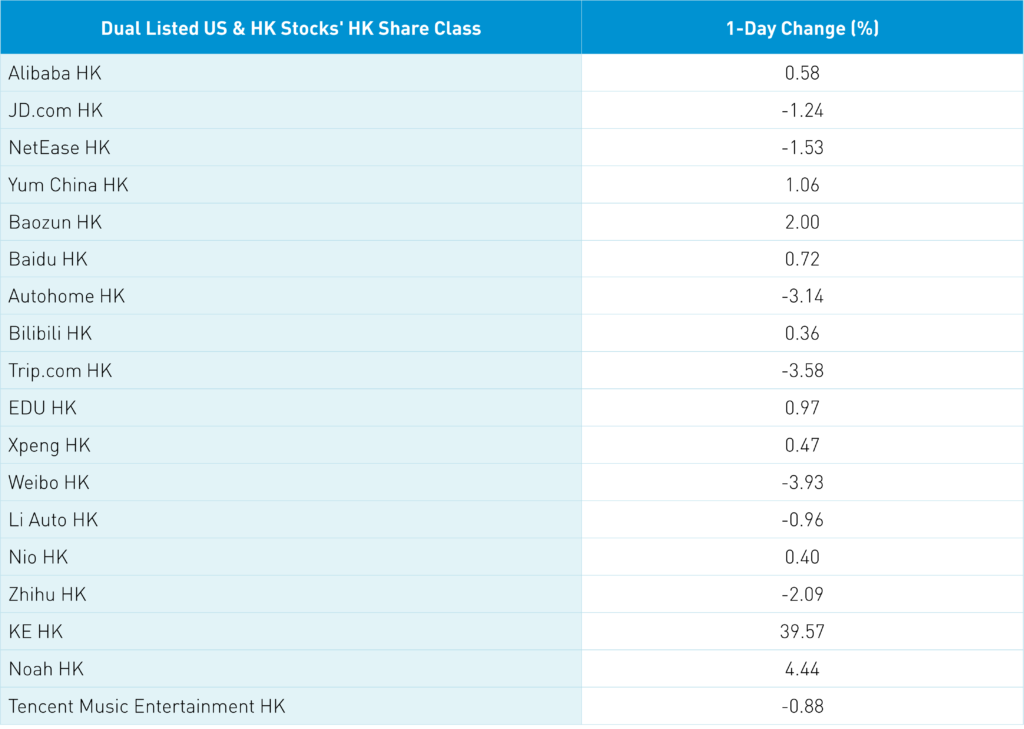

Unfortunately, Hong Kong internet stocks couldn’t take the baton from US listed China ADRs’ strong move Tuesday as Hong Kong’s most heavily traded were Meituan -6.48% on news that Tik Tok’s China equivalent would launch a rival restaurant delivery operation in March, Tencent +0.58% on new games coming, Alibaba HK -1.24% as spillover from the Tik Tok news, Baidu -3.14% as AI chat bot profit taking, and Kuaishou -6.16% after the company shut down 500k accounts due to rules violations.

Mainland investors were sellers of Hong Kong stocks via Southbound Stock Connect with a healthy -$463 million with Meituan whacked. Yicai Global is reporting that Tik Tok is denying the delivery operation story this morning. Interesting considering how big Hong Kong declined! After the strong move the last few months, we are getting the inevitable pullback/correction as the Hang Seng nears the 21k level. A catalyst will be the Q4 financial results from the companies due to their Q1 forecast.

Last night, Yum China reported after the US close missing revenue expectations but beating on net income and EPS. The company’s release provides a clear picture of the Q4 disruptions as workers called in sick and customers stayed home. The company stated that according to government statistics, the number of domestic travelers and related tourism spending during the 7-day CNY holiday increased approximately 20% and 30% year over year, respectively, but remained over 10% and 30% below the 2019 level, respectively. Performance at our transportation and tourist locations was better than the statistics indicated. Overall same-store sales for the comparable CNY holiday also increased mid-single digit year over year but remained below the 2019 level.

As the country enters the new phase of COVID response, we are cautiously optimistic. The overall business environment and consumer sentiment have improved but near-term uncertainties remain. Consumers tend to be more careful with spending after holidays.” So, the rebound is real as the consumer comes back online incrementally. In the analyst Q&A, CEO Joey Wat stated “…the Chinese new recovery is encouraging. The momentum is good. And we also saw good recovery across the region.”

Premier Li had a speech emphasizing the economy though didn’t appear to be a market mover. President Biden’s State of the Union focused on competition versus war which is good. Interesting article from The Strait Times on Chian’s softer tone in advance of next year’s President election there (link on Twitter @ahern_brendan). Worth noting the two parties in Taiwan win every other election thus a pro-China win would be expected. The article notes a Taiwan official is visiting China this week with food imports being eliminated and potentially the opening up of flights again. Mainland markets were off as well on no news as the 3,200 level on the Shanghai should be watched as support. Foreign investors were small net sellers overnight.

In November 2022 China launched their version of an Individual Retirement Account (IRA) though they call it a personal pension. Thus far, 19 million people have established accounts allocating RMB 14 billion. A small step to Chinese households increasing their 1% of wealth to Mainland stocks. Not a typo: 1% of household wealth is in stocks!

The Hang Seng and Hang Seng Tech fell -0.07% and -1.88% respectively on volume +11.39% from yesterday which is 92% of the 1-year average. 214 stocks advanced while 277 declined. Main Board short turnover increased +32.87% from yesterday which is 80% of the 1-year average as 15% of turnover was short turnover. Value factors outperformed growth factors as large caps beat small caps. Top sectors were utilities gaining +1.88%, industrials closing higher +0.87%, and health care finishing +0.7% while discretionary fell -1.96%, tech closed lower -0.72%, and communication finished -0.15%. Top sub-sectors were household products, utilities, and transportation while retail, healthcare equipment, and auto were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$463 million of Hong Kong stocks with Meituan a healthy sell, Tencent a very small sell, and Kuaishou a moderate sell.

Shanghai, Shenzhen, and STAR Board eased -0.49%, -0.54%, and -0.93% respectively on volume -4.84% from yesterday which is 89% of the 1-year average. 1,322 stocks advanced while 3,320 stocks declined. Value and growth factors were both off as small caps “outperformed” large caps. Real estate and healthcare were the only positive sectors gaining +0.57% and +0.3% as communication fell -1.76%, tech down -0.78%, and staples closing lower -0.77%. Top sub-sectors were shipping, airports, and fertilizer while telecom, precious metals, and internet were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$204 million of Mainland stocks. CNY was off versus the US dollar -0.03%, Treasury bonds sold off slightly, while copper and steel rallied.

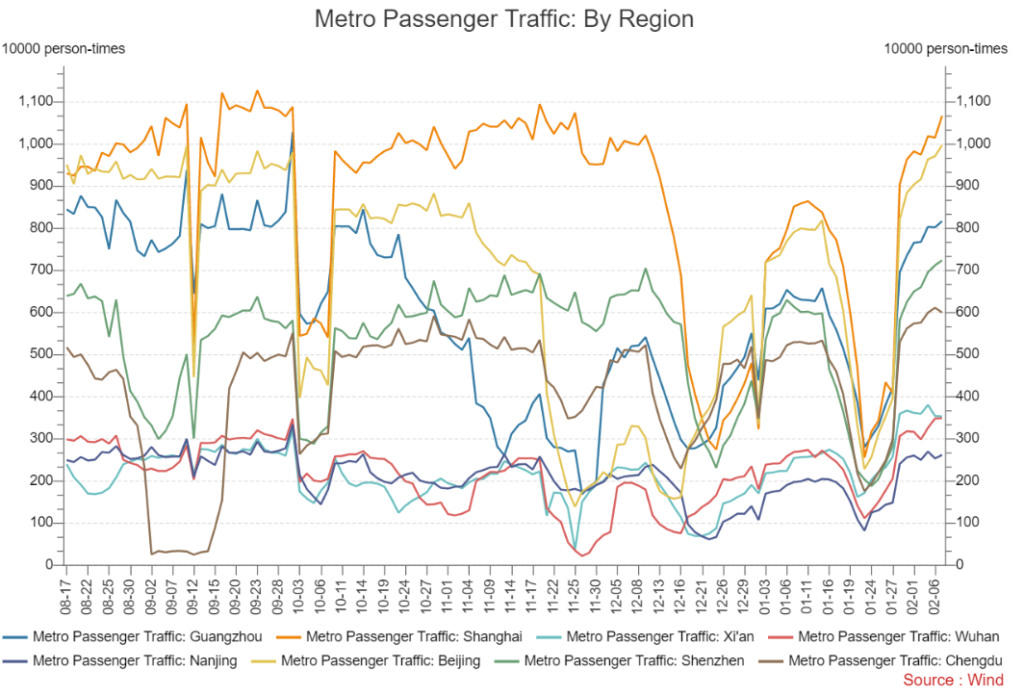

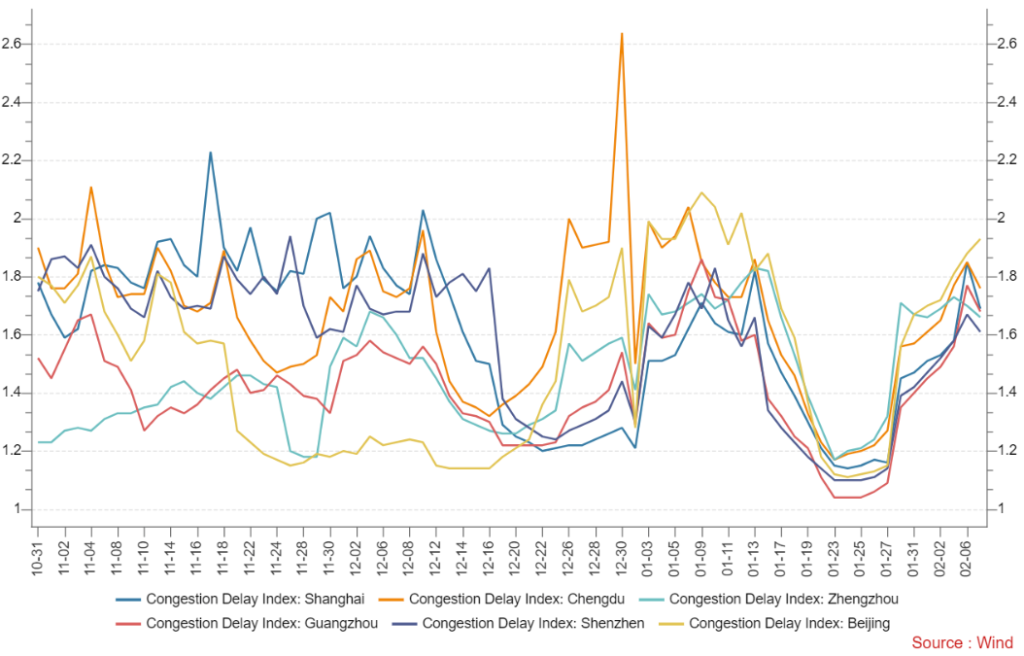

Major Chinese City Mobility Tracker

The rebound is real.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.78 versus 6.79 yesterday

- CNY per EUR 7.29 versus 7.27 yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.90% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.05% yesterday

- Copper Price +0.28% overnight

- Steel Price +0.15% overnight