US Dollar Strength & Political Rhetoric Weigh on Markets, Week in Review

3 Min. Read Time

Week in Review

- Asian equities were mostly lower this week, following US equities south as positive internet earnings, which kicked off this week, could not stem the market’s decline.

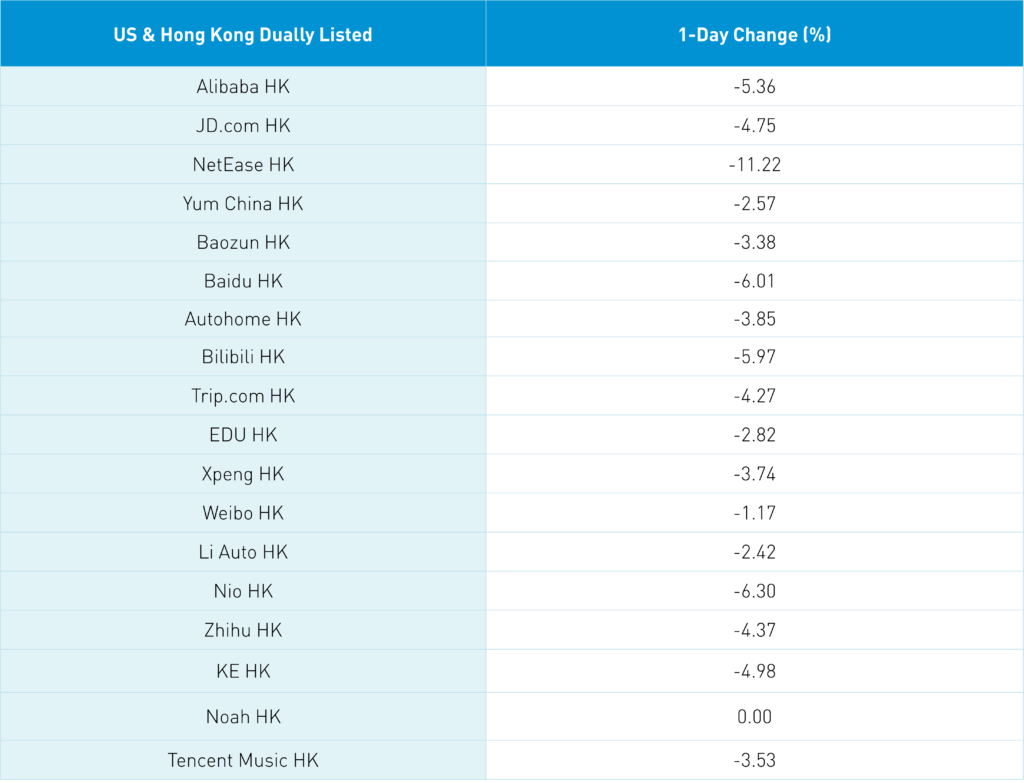

- Alibaba beat estimates on top line revenue and net income, NetEase reported a strong beat on net income, Vipshop beat on net income, and Baidu increased its buyback program by $5 billion through 2025.

- JD.com shares were hit particularly hard this week on concerns about the company’s spending to compete with E-Commerce rival Pinduoduo.

- After the Munich Security Conference last week, new foreign minister Qin Gang commented that China may help seek a peace arrangement in Ukraine.

Key News

Asian equities ended an off week only slightly lower. Japan outperformed after Bank of Japan Governor nominee Kazuo Ueda reiterated the country’s current loose monetary policy stance. The US dollar continued to strengthen as the Asia dollar index fell -0.42% overnight and China’s renminbi (CNY) fell -0.51% to 6.96 CNY per USD from the January 31st level of 6.75.

Political rhetoric did not help sentiment due to Western skepticism of China’s proposed role in mediating a peace process in Ukraine. Meanwhile, Blinken said that China is thinking about military aid to Russia and the US is increasing its troop presence in Taiwan. At the G20 finance minister conference, Janet Yellen’s staff will meet with their Chinese equivalents, a small positive for US-China relations.

The political sentiment and US dollar kept investors on the sidelines as Hong Kong internet stocks underperformed their US-listed counterparts. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.85%, Alibaba, which fell -5.36%, Meituan, which fell -3.38%, Techtronic, which gained +4.4%, Baidu, which fell -6.01%, Hong Kong Exchanges, which fell -2.5%, JD.com, which fell -4.75%, and NetEase, which fell -11.22%.

Analysts appeared somewhat shocked, as I was, at Alibaba and NetEase’s stock performance after beating analyst expectations on Q4 earnings. There are concerns that JD.com’s discount plan will weigh on E-Commerce plays against the backdrop of China’s consumer coming back online.

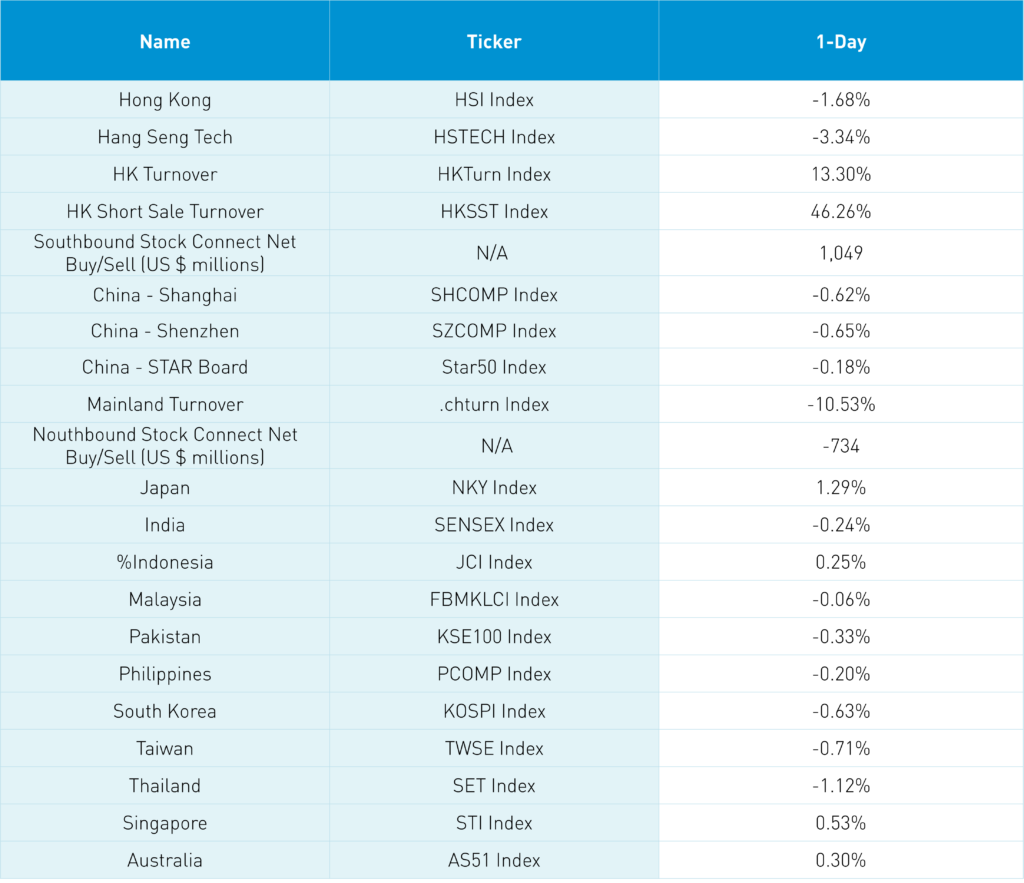

The Hang Seng Index fell -1.68%, closing barely above the 20,000 level at 20,010, as Mainland investors were large buyers of Hong Kong stocks to the tune of a healthy $1 billion as Tencent was a beneficiary via Southbound Stock Connect. After the close, the Hang Seng Index announced no new additions as part of their March rebalance.

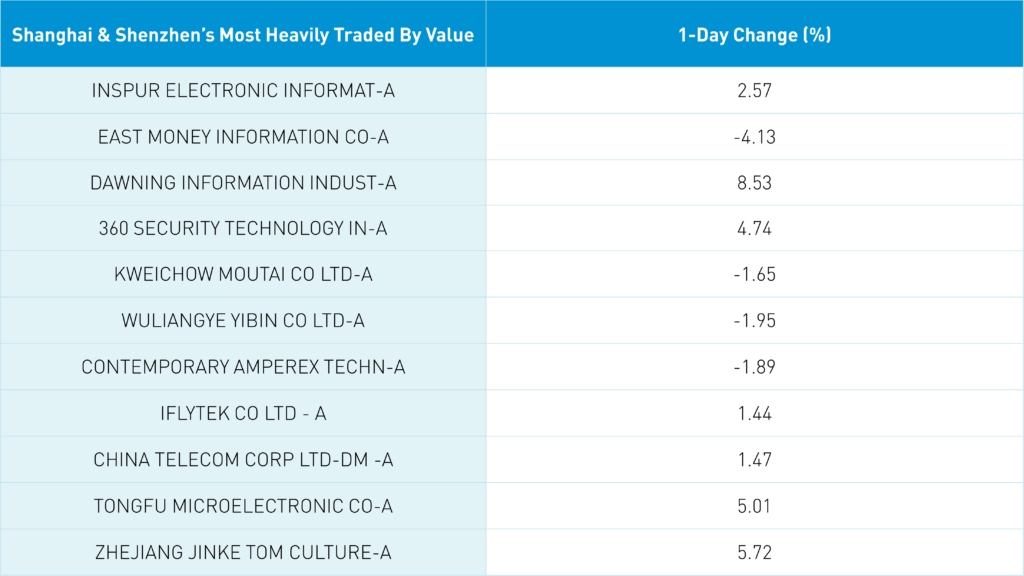

Mainland markets were lower, though not nearly as low as Hong Kong. Foreign investors were net sellers of Mainland stocks overnight as foreign large and mega cap growth and consumer plays underperformed the market on little to no news. Remember the Dual Session policy meetings start next weekend, which will include articulating economic policies for 2023. For the week, foreign investors sold -$587 million worth of Mainland stocks. Shanghai and Shenzhen are still trading in a range with a 3,300 resistance level for the former.

Earnings continue next week with Li Auto reporting on Monday, Weibo and NIO reporting on Wednesday, and Bilibili reporting on Thursday.

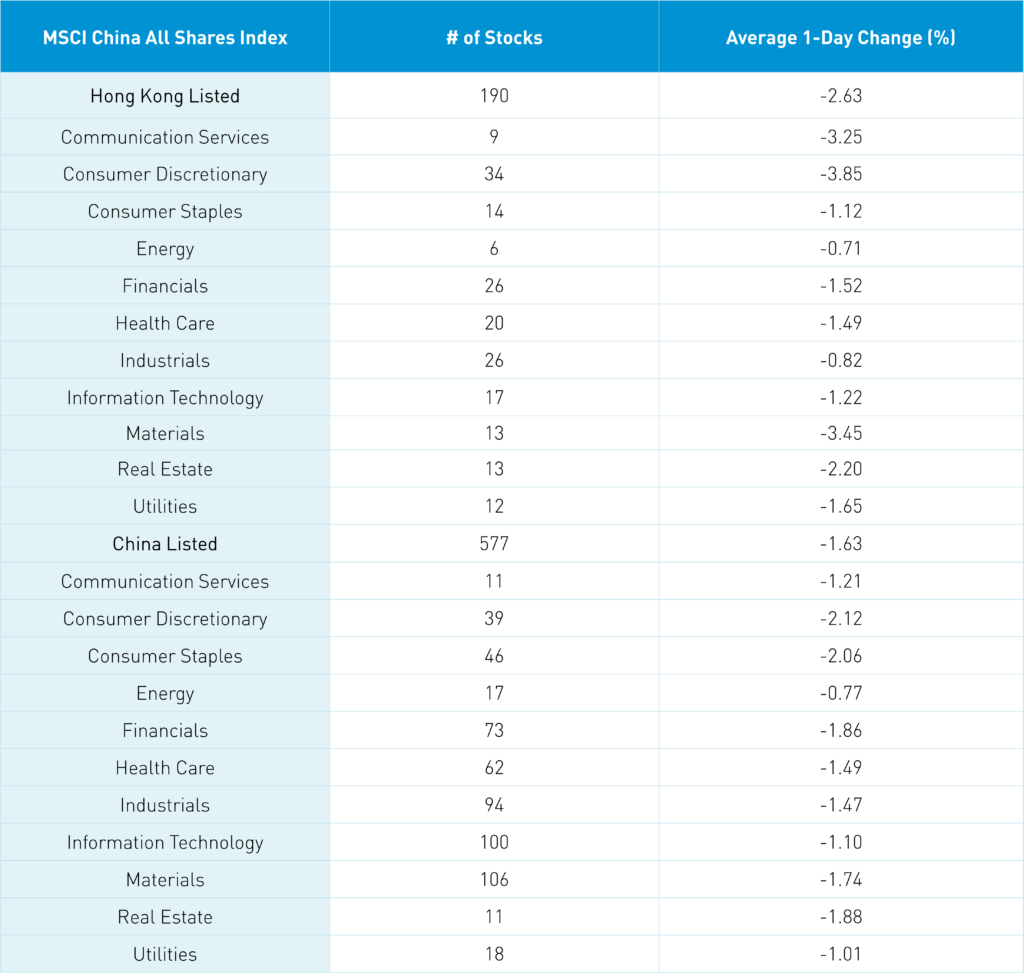

The Hang Seng and Hang Seng Tech indexes fell -1.68% and -3.34%, respectively, on volume that increased +13.3% from yesterday, which is 92% of the 1-year average. 79 stocks advanced, while 419 stocks declined. Main Board short turnover increased +46.23% from yesterday, which is 93% of the 1-year average, as 17% of turnover was short turnover. Value factors outperformed growth factors as large caps “outperformed” small caps. All sectors were down, as consumer discretionary fell -3.85%, materials fell -3.45%, and communication services fell -3.25%. The top-performing subsectors were semiconductors and consumer services. Meanwhile retail, media, and autos were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought a healthy $1 billion worth of Mainland stocks as Tencent was a strong net buy, Meituan was a small net buy, and Kuaishou was a small net sell.

Shanghai, Shenzhen, and the STAR Board fell -0.62%, -0.65%, and -0.18%, respectively, on volume that decreased -10.53% from yesterday, which is 80% of the 1-year average. 1,662 stocks advanced, while 2,914 stocks declined. Growth and value factors were mixed as small caps “outperformed” large caps. All sectors were negative as consumer discretionary fell -2.14%, consumer staples fell -2.07%, and real estate fell -1.9%. The top-performing subsectors were computer hardware, aerospace/military, and internet. Meanwhile, motorcycles, education, and precious metals were among the worst. Northbound Stock Connect volumes were moderate as foreign investors sold -$734 million worth of Mainland stocks. CNY fell -0.48% versus the US dollar to 6.96 CNY per USD, Treasury bonds rallied while Shanghai copper and steel fell.

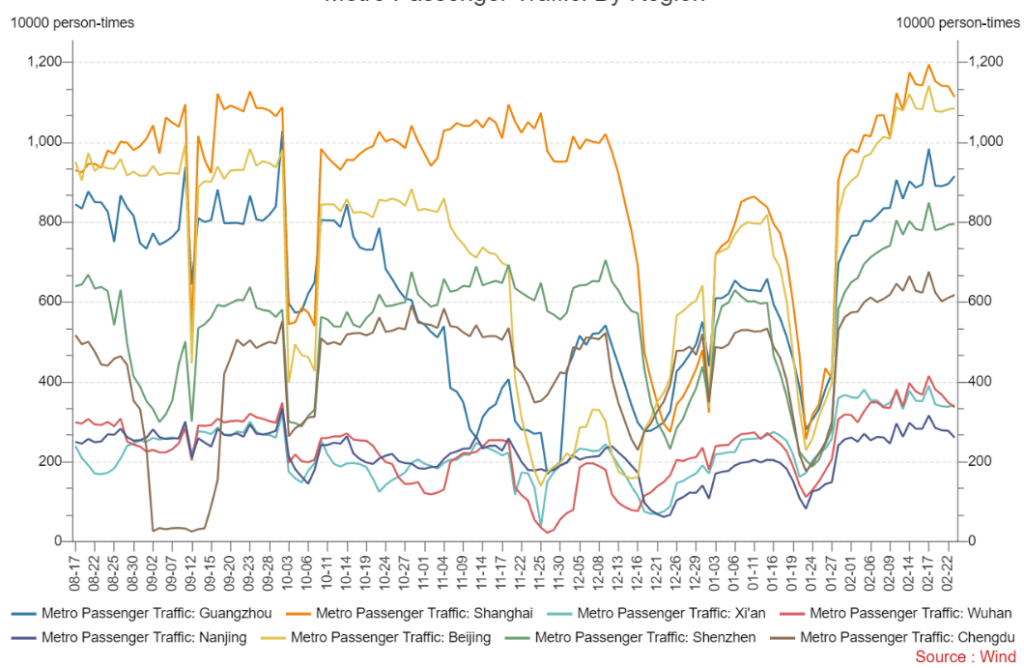

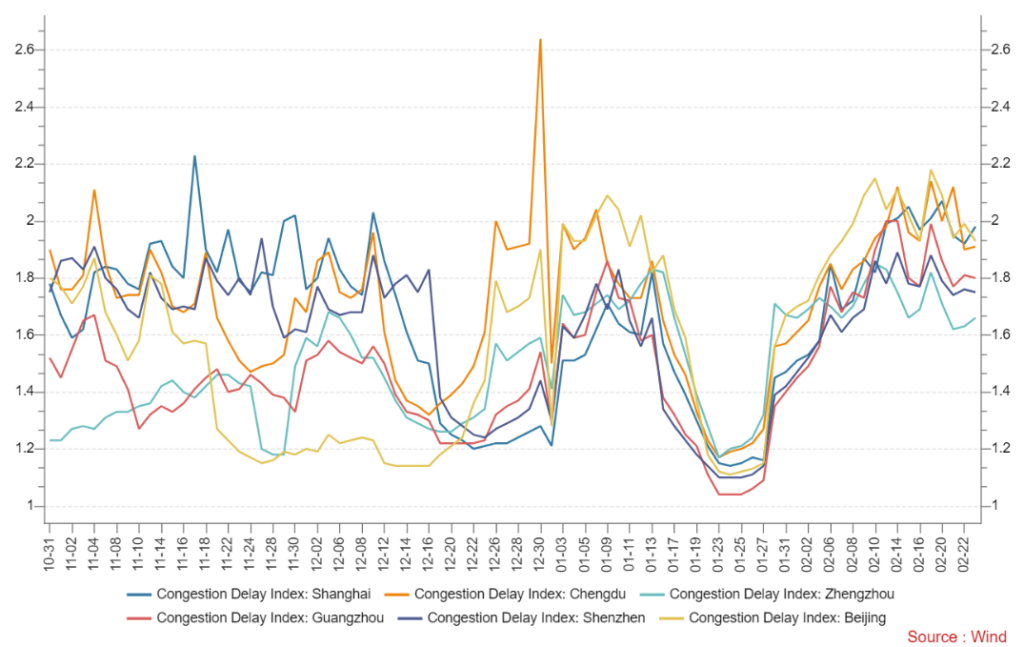

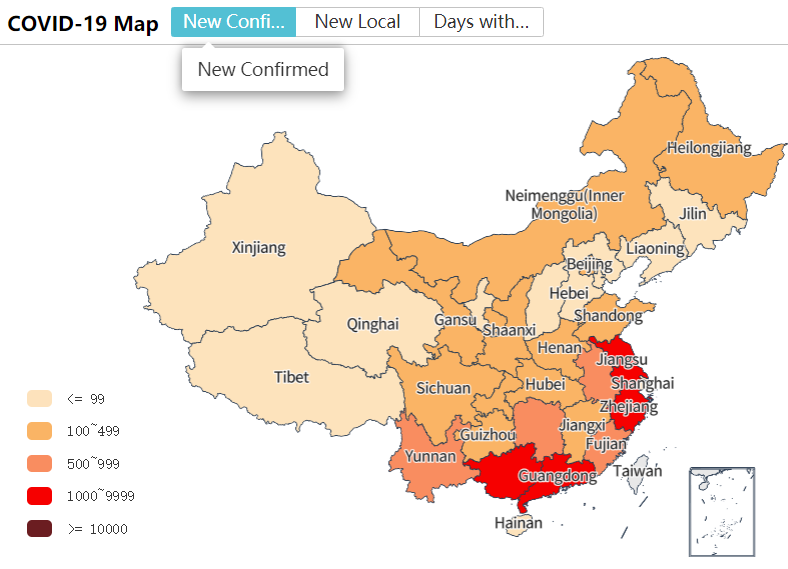

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.96 versus 6.91 yesterday

- CNY per EUR 7.33 versus 7.31 yesterday

- Yield on 1-Day Government Bond 1.62% versus 1.61% yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.92% yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.10% yesterday

- Copper Price -0.95% overnight

- Steel Price -1.01% overnight