Tencent Provides Promising Outlook as Investors Wait for Jay Powell

4 Min. Read Time

Tencent Q4 Earnings Overview

Tencent reported Q4 financial results after the Hong Kong close and before the US open overnight. Goldilocks would say that the results were "not too hot and not too cold." Ultimately, advertising revenue increased +15% year-over-year (YoY) in Q4 year over year compared to a -7% decrease in 2022 from 2021. We knew that Q4 was not going to be good as COVID spread across China following the elimination of the zero COVID policy. Markets are forward-looking, so the pickup in Q4 likely means another pickup in Q1, Q2, etc. In fact, during the conference call, the company said that January and February were showing “positive signs” of a sustained recovery. Tencent’s main performance drivers are video games and its WeChat social media platform, which is up to 1.3 billion users globally. While international games saw gains, domestic games were off. Management slashed sales and marketing expenses by -47% YoY in Q4 from RMB 11.6 billion to RMB 6.1 billion, compared to a -28% decrease in 2022 versus 2021. Research and development and general/administrative expenses did increase in both Q4 and 2022. Overall, I would say that there is a light on the horizon!

- Revenue increased +0.5% to RMB 144.954 billion (US $20.8 billion) versus analyst expectations of RMB 144.5 billion and Q4 2021’s RMB 144.188 billion.

- Adjusted Net Income increased to RMB 29.711 billion versus analyst expectations of RMB 30.843 billion and Q4 2022’s 24.88 billion.

- Adjusted EPS was RMB 3.042 versus analyst expectations of RMB 3.178.

Key News

Asian equities were higher overnight on light volumes, while Indonesia was off for the Nyepi holiday, which is a day of silence, fasting, and meditation.

That sounds delightful, though it is not happening for US and global traders and investors. At 2:30 pm EDT all eyes will be on Jay Powell. Investors seem to be positive that the US and European bank crisis is contained. Fingers crossed!

President Xi’s visit to Russia seemed to run the balancing act successfully. A follow-up call to Zelensky seems to be the next step on their peace proposal.

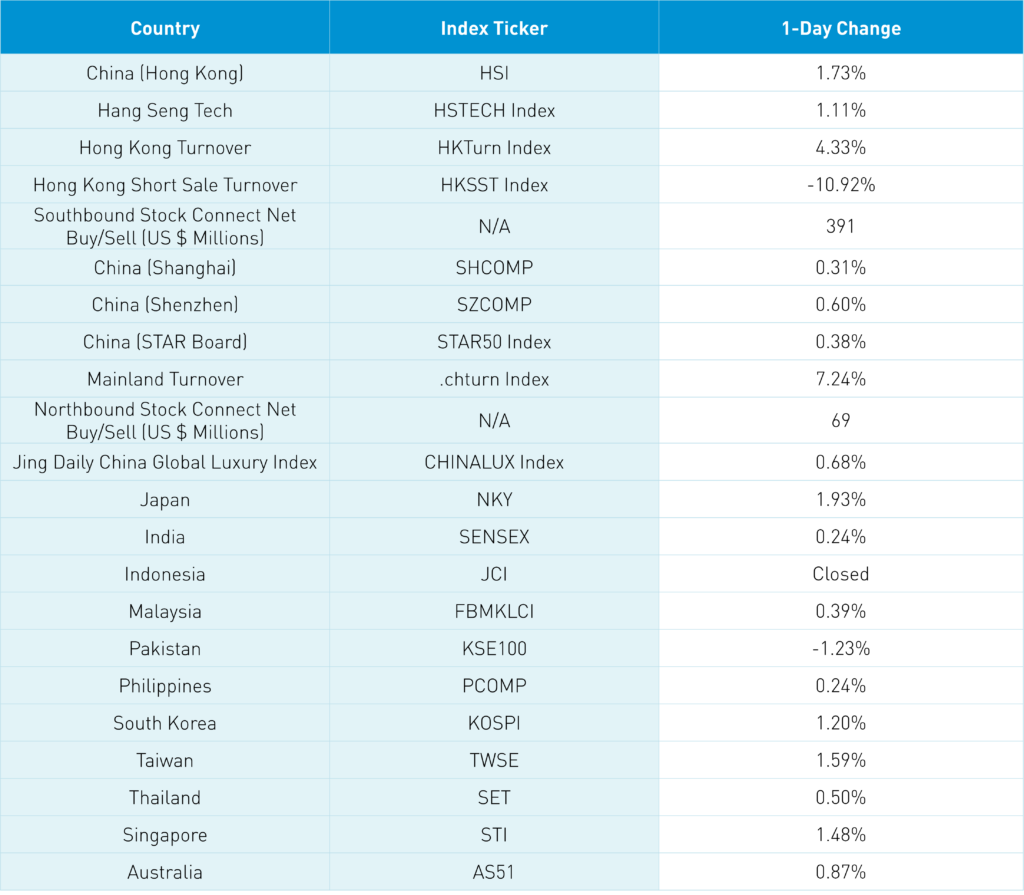

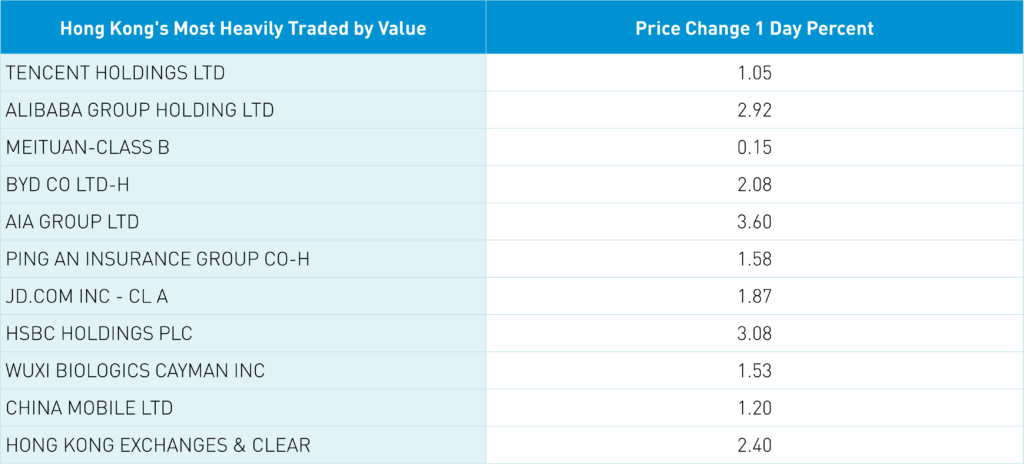

Hong Kong had a good day, led by the most heavily traded, which was Tencent, which gained +1.05% in advance of their earnings call today. Alibaba gained +2.92%, Meituan gained +0.15%, BYD gained +2.08%, and AIA gained +4.6%. Volumes were light, though short sale volumes were lighter than overall volumes. Mainland investors bought a net $391 million worth of Hong Kong stocks today as Tencent was a large net buy.

Mainland China underperformed Hong Kong, but had several interesting and positive catalysts. I would point out Evergrande’s offshore bond restructuring. Wasn’t Evergrande China’s Lehman moment? Real estate was the top performer in Hong Kong, where the industry gained +2.45% and ended up as the 2nd best sector on the Mainland, where it gained +1.4%. I still can’t get anyone to buy these offshore China US dollar bonds. #frustrating.

Nvidia’s cloud computing announcement lifted tech broadly, but specific subsectors such as computer hardware, data centers, AI etc. were lower as mega cap tech plays had a very strong day.

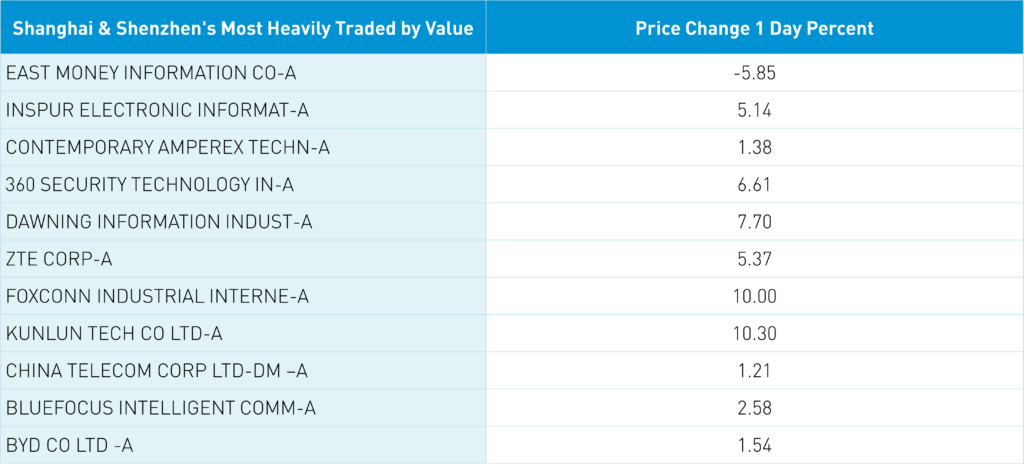

EV ecosystem stocks were positive on reports that Beijing will incentivize purchases. Popular financial stock and broker East Money fell -5.85% after its trading platform crashed twice. Foreign investor activity was very light with a net buy of $69 million worth of Mainland stocks. CNY and the Asia Dollar Index were off slightly versus the US dollar.

The US political rhetoric toward China has been described as neo-McCarthyism, though it takes two to tango. What’s driving this? A friend says money rules the world so how could that explain it. I stumbled upon the Peter G. Peterson Foundation website recently, which is focused on the US’ budget situation. It is worth taking a look. According to the US Treasury, in 2022 interest payments were the eighth largest line item in government spending, at 8% or a whopping $475 billion. Is that going to go up or down based on the Fed hiking rates? To fund the increase in interest payments coming, something needs to be cut. With a 60% chance of a US recession coming, are tax receipts going to go up or down? That is not a good combination. 2022 spending finished in the following order: social security, health, income security, national defense, Medicare, and education/training/employment/social services. What gets cut? Tough choices to be made and the defense industry needs to prove its worth, hence the neo-McCarthyism.

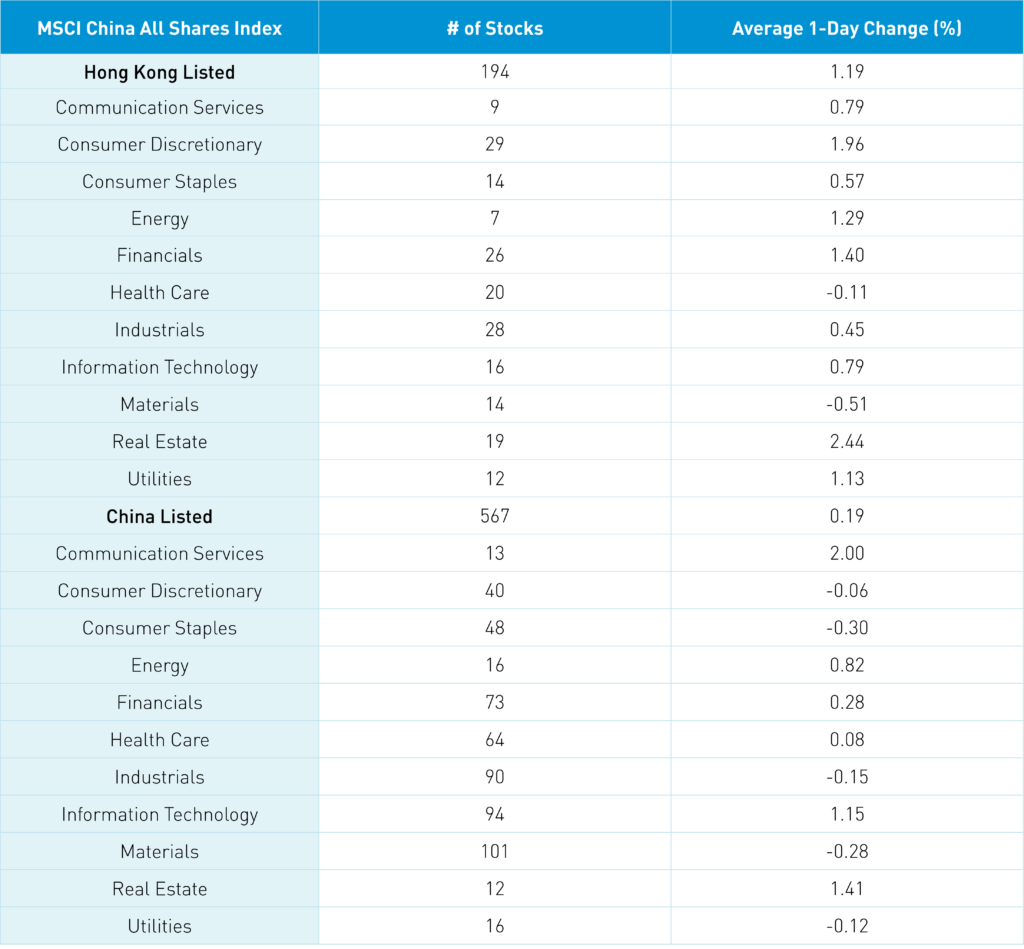

The Hang Seng and Hang Seng Tech indexes gained +1.73% and +1.11%, respectively, on volume that increased +4.33% from yesterday, which is 88% of the 1-year average. 339 stocks advanced, while 151 declined. Main Board short turnover fell -10.94% from yesterday, which is 73% of the 1-year average as 14% of turnover was short turnover. Value outperformed growth, while large caps outperformed small caps. The top-performing sectors were real estate, which gained +2.43%, consumer discretionary, which finished higher by +1.96%, and financials, which gained +1.39%, while healthcare and materials were down -0.11% and -0.52%, respectively. The top-performing subsectors were insurance, technical hardware, and autos, while media, semiconductors, and household products were among the worst performing. Southbound Stock Connect volumes were light as Mainland investors bought $391 million worth of Hong Kong stocks today as Tencent was a moderate buy, Kuiashou was a small net buy, and Meituan was a small net sell.

Shanghai, Shenzhen, and the STAR Board gained +0.31%, +0.60%, and +0.38%, respectively, on volume that increased +7.24% from yesterday, which is 107% of the 1-year average. 2,715 stocks advanced, while 1,864 stocks declined. Value factors outperformed growth factors, as small caps outpaced large caps. The top-performing sectors were communication services, which gained+2%, real estate, which closed higher by +1.41%, and technology, which gained +1.16%, while industrials fell -0.14%, materials closed lower by -0.28%, and consumer staples fell -0.3%. The top-performing subsectors were computer hardware, internet, and communication equipment. Meanwhile, office supplies, restaurants, and precious metals were among the worst. Northbound Stock Connect volumes were moderate/high as foreign investors bought a net $69 million worth of Mainland stocks as Kweichow Moutai and Foxconn were net buys. CNY was off slightly versus the US dollar, while Shanghai copper gained, and Shanghai steel lost.

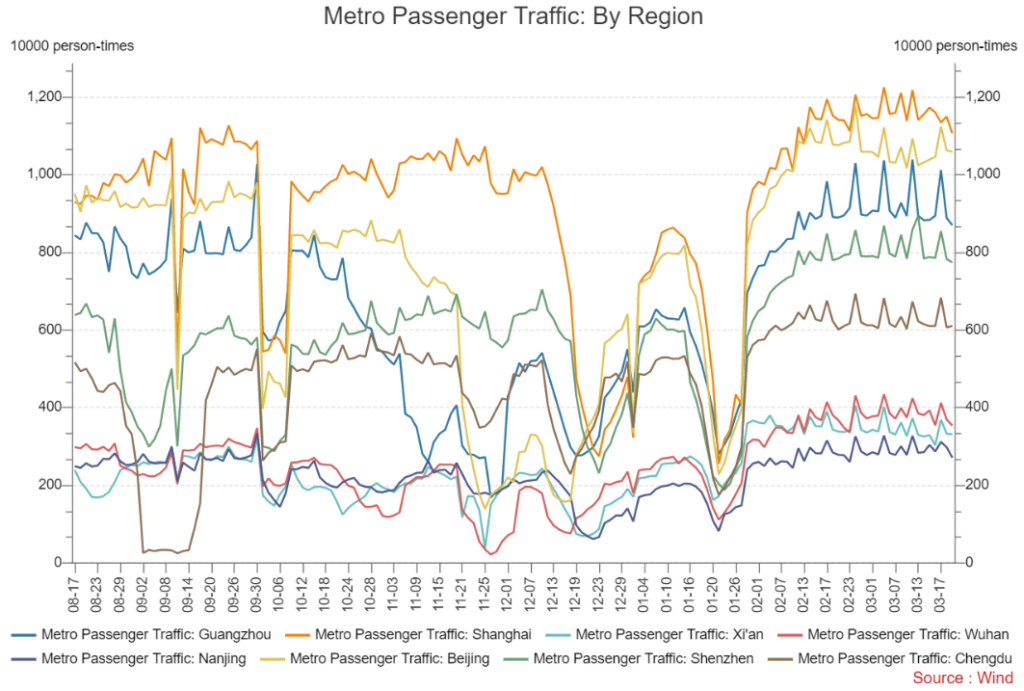

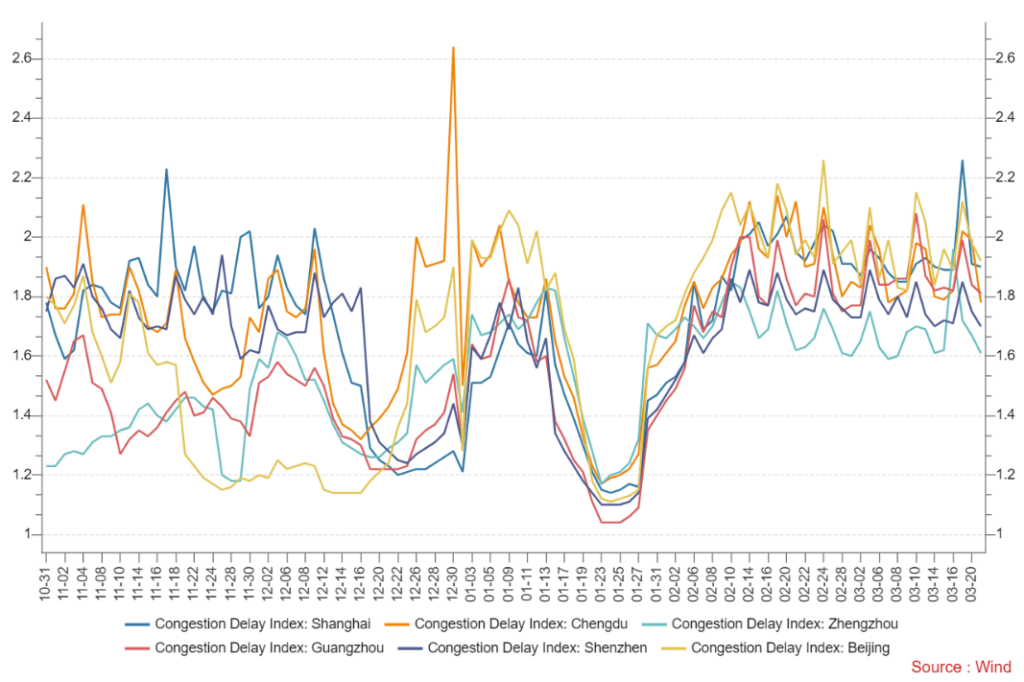

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.87 yesterday

- CNY per EUR 7.43 versus 7.40 yesterday

- Yield on 10-Year Government Bond 2.85% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.02% yesterday

- Copper Price +0.98% overnight

- Steel Price -0.81% overnight