Premier Li’s Improving Economic Outlook & PetroChina’s EXtraordinary Results

3 Min. Read Time

Key News

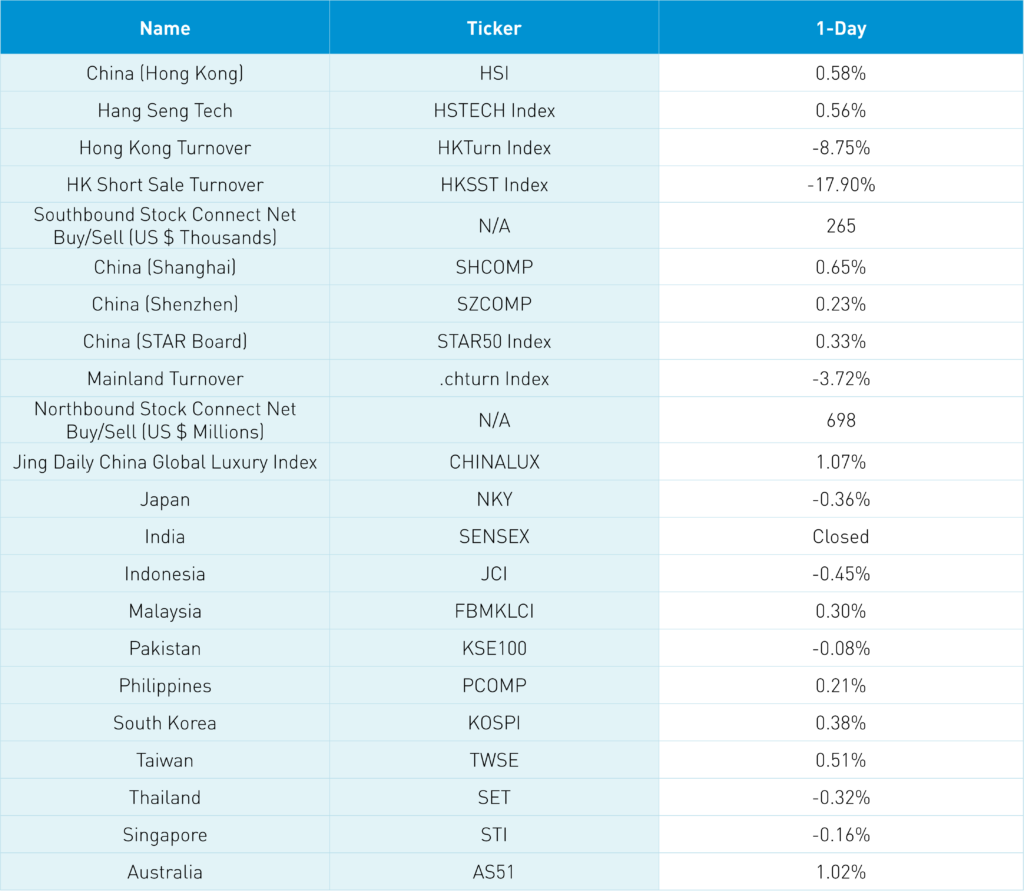

Asian equities were broadly higher except for Japan and South East Asia, while India was closed for Rama Navami. According to Google, this Hindu festival celebrates the birthday of Rama, the seventh avatar of the deity Vishnu. So we have that going for us…….which is nice.

In breaking news, in a similar fashion to Alibaba, JD.com announced a spin-off and separate listing of JD property on the Main Board of the Stock Exchange of Hong Kong Limited. Stay tuned!

China and Hong Kong rallied into the close as Premier Li’s keynote speech at the Boao Forum stated, “In the first two months of this year, the Chinese economy showed an encouraging momentum of rebound. The situation in March is even better than that in January and February.” The government will “…build on the momentum of recovery and work for sustained and overall improvement in the economic performance.” Shocking how little coverage his speech received in Western media though that’s job security for me!

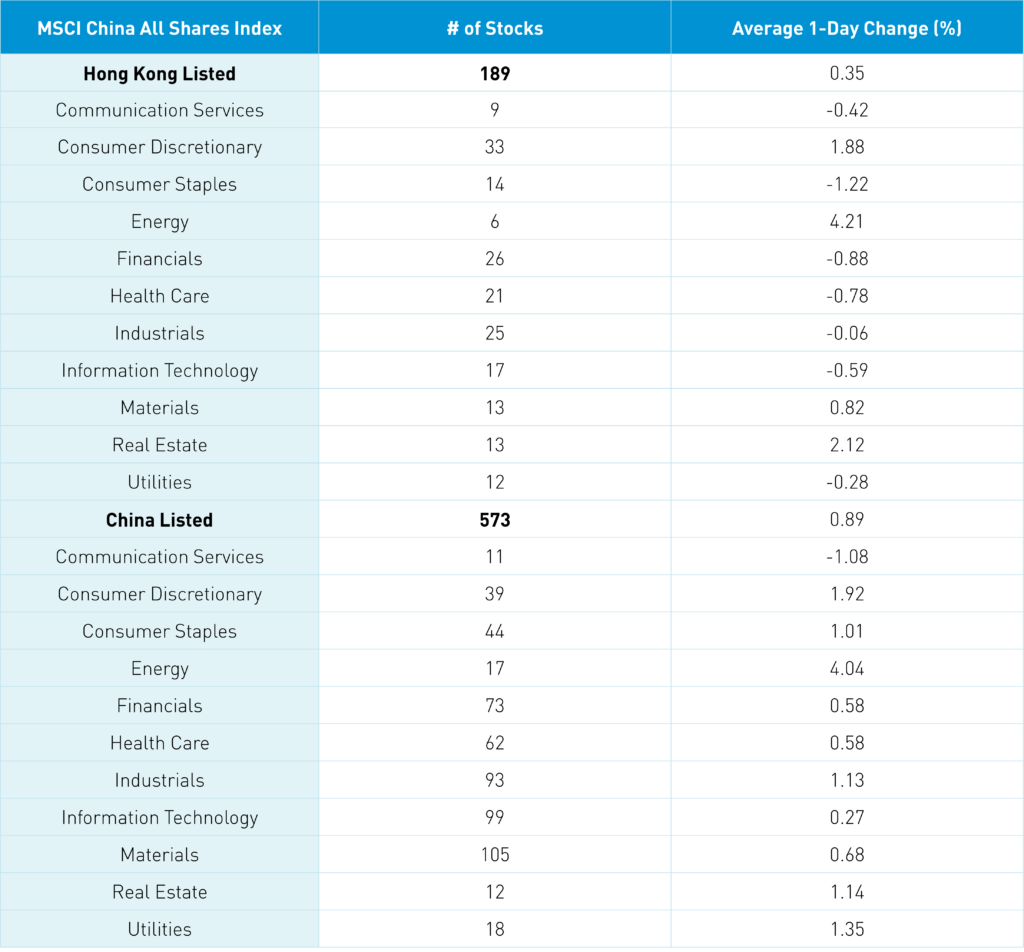

As we’ve stated ad nauseam, Q1 2023 will be better than Q4 2022, Q2 will be better than Q1, etc., as consumer confidence builds and pro-domestic consumption policies are implemented. The top sector performer in China, +4.08%, and HK, +4.21%, was energy, led by PetroChina (857 HK, 601857 CH), which gained +7.83% in Hong Kong and +6.95% in China. The energy giant announced revenue jumped +23.9% year-over-year (YoY), net income jumped +62.1% YoY, and announced a stock buyback for the first time! Another bad look for Chinese Ex SOE strategies, in light of recent SOE reform announcements, which don’t hold any energy stocks.

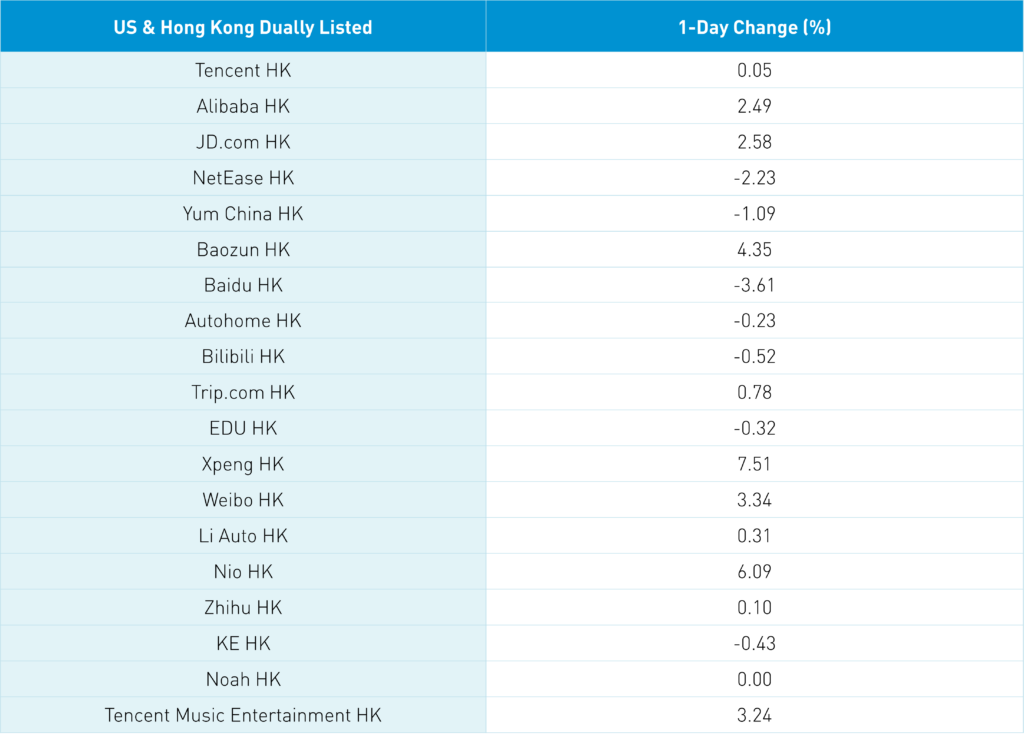

Houston, we have a problem…Hong Kong’s most heavily traded were Tencent +0.05%, Alibaba HK +2.49%, Meituan +1.43%, and Kuaishou +5.6%. Tencent, Meituan, and Kuaishou had small/moderate net buying from Mainland investors via Southbound Stock Connect. On Alibaba’s conference call last night explaining the new corporate structure, when asked about making Hong Kong the primary listing, which would make the Hong Kong shares Southbound Connect eligible, management said they were looking into it after postponing their Hong Kong filing. Hmmm. Heavily shorted Hong Kong-listed ETFs saw short volume as a percentage of volume decline from 71% to 50%, 64% to 38%, and 62% to 43% as the Hang Seng Index stayed above the 20k level two days in a row. Foreign investors bought a healthy $698mm of Mainland stocks via Northbound Stock Connect.

The Hang Seng and Hang Seng Tech gained +0.58% and +0.56% on volume, down -8.75% from yesterday, 110% of the 1-year average. 260 stocks advanced, while 235 declined. Main Board short turnover fell -17.9% from yesterday, 101% of the 1-year average, as 16% of turnover was short turnover. Value factors outpaced growth factors as large caps edged out small caps. The top sectors were energy +4.21%, real estate +2.12%, and discretionary +1.88%, while staples -1.22%, financials -0.88%, and healthcare -0.78%. The top sub-sectors were energy, auto, and household, while healthcare equipment/services, technical hardware, and insurance were the worst. Southbound Stock Connect volumes were light as Mainland investors bought $265mm of Hong Kong stocks, with Tencent, Meituan, and Kuaishou all small/moderate net buys.

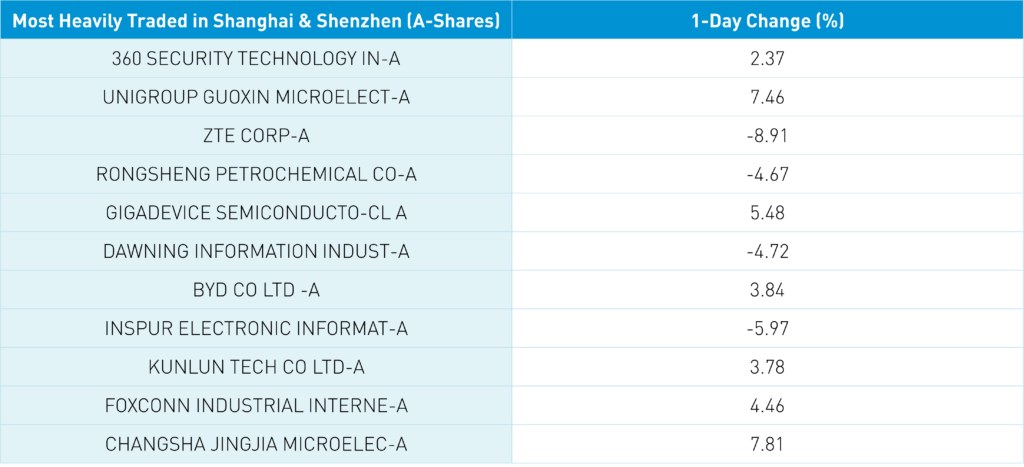

Shanghai, Shenzhen, and STAR Board gained +0.65%, +0.23%, and +0.33% on volume -3.72% from yesterday, 105% of the 1-year average. 1,857 stocks advanced, while 2,802 stocks declined. Value factors outpaced growth factors as large caps outperformed small caps. The top sectors were energy +4.06%, discretionary +1.94%, and utilities +1..36%, while communication was the only negative sector -1.06%. The top sub-sectors were household appliances, coal, and restaurants, while telecom, communications equipment, and software were the worst. Northbound Stock Connect volumes were moderate/high as foreign investors bought $698mm of Mainland stocks, with Foxconn the highest volume Connect name on a small net buy. CNY and the Asia dollar index made minimal gains versus the US dollar. Treasury bonds sold off while Shanghai copper and steel gained.

Shout out to my not-so-little guy Gray on his birthday!

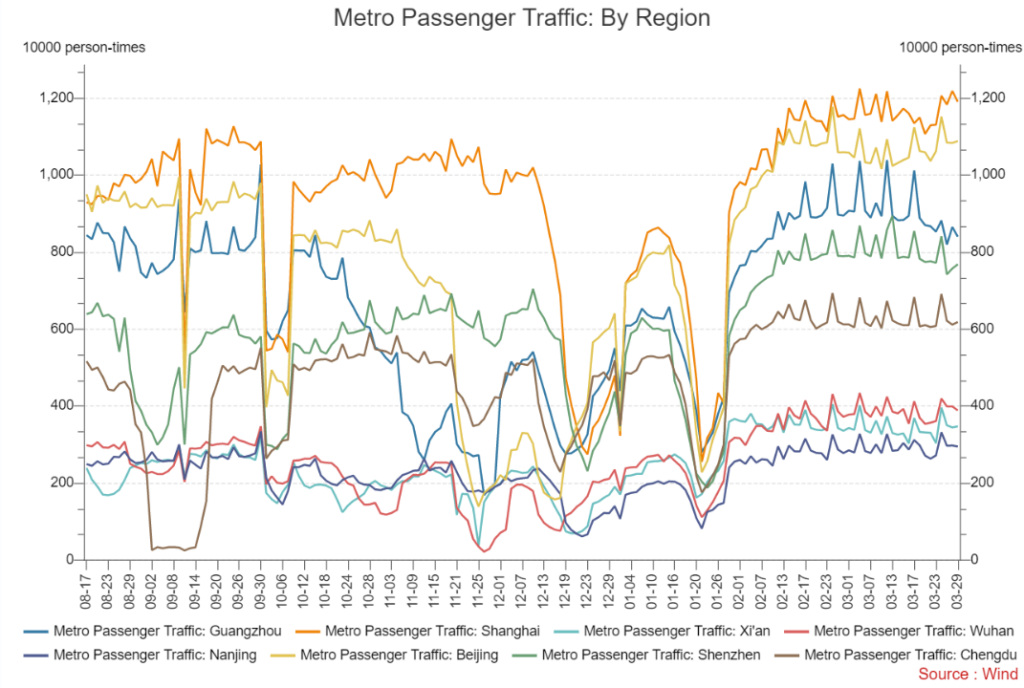

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.88 yesterday

- CNY per EUR 7.48 versus 7.48 yesterday

- Asia Dollar Index +0.07% overnight

- Yield on 10-Year Government Bond 2.86% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.04% versus 3.02% yesterday

- Copper Price +0.45% overnight

- Steel Price -0.14% overnight