April Auto Sales & Li Auto in Focus

3 Min. Read Time

Key News

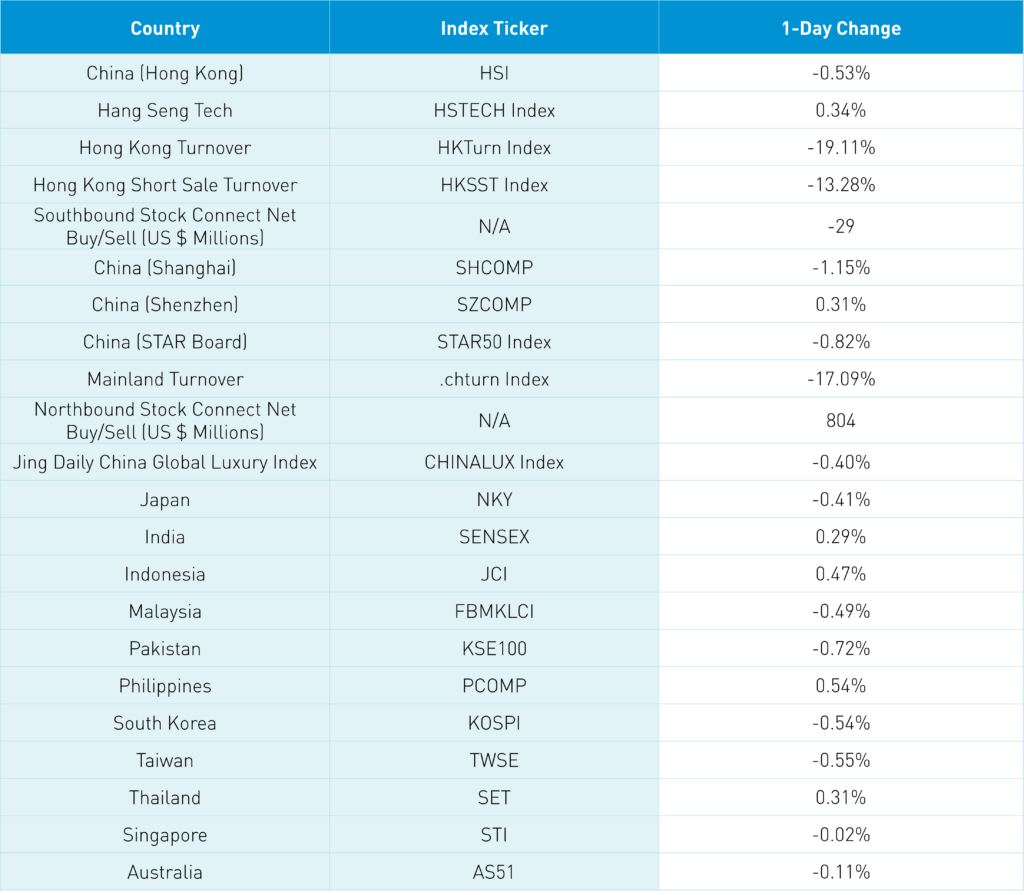

Asian equities were lower overnight on light volumes and US debt ceiling concerns in advance of today’s US CPI release.

Foreign investors bought a healthy $804 million of Mainland stocks today via Northbound Stock Connect. China and Hong Kong were mixed as Mainland traders booked profits in SOEs with the Mainland and Hong Kong financial sectors down -2.9% and -2.23% along with Mainland and Hong Kong energy sectors down -2.31% and -0.8%. SOE reform buzz has led local Chinese asset managers to list SOE-focused ETFs. Auto stocks were a top performer in both China and Hong Kong as April auto sales increased 54.5% year over year to 1.65 million and +2.1% month over month.

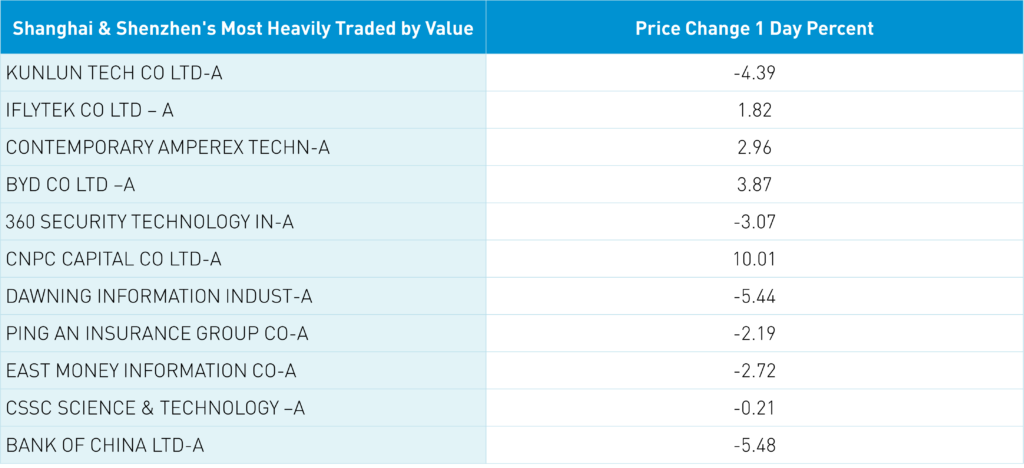

Within the Mainland, the third and fourth most heavily traded stocks by value were CATL (300750 CH) gaining+2.96% and BYD (002594 CH) closing higher by +3.87%. Prior to the US market opening, Li Auto (LI US) beat analyst estimates on revenue +96.55% year over year, adjusted net income, and adjusted EPS as the electric vehicle company delivered 52,584 vehicles in the first quarter. JD.com reports tomorrow after the Hong Kong close/prior to the US opening.

The PCAOB released its 2022 inspection reports for the auditors the Board inspected in China. While some issues were discovered, they gained complete access and, in the words of Chair Williams: “It is not unexpected to find such high rates of deficiencies in jurisdictions that are being inspected for the first time. And the deficiencies identified by PCAOB staff at the firms in mainland China and Hong Kong are consistent with the types and number of findings the PCAOB has encountered in other first-time inspections around the world.” This should be viewed as a positive.

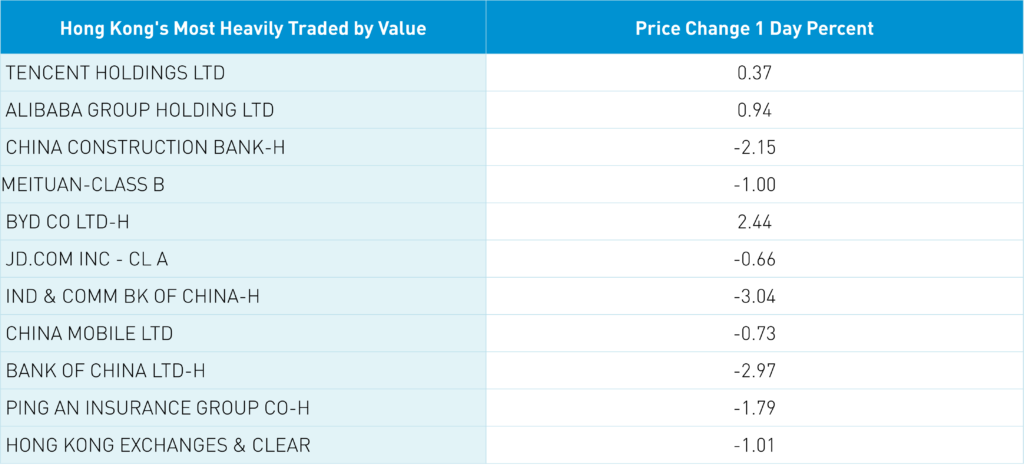

Hong Kong was mixed overnight on light volume with the most heavily traded by value Tencent +0.37%, Alibaba HK +0.94%, China Construction Bank -2.15%, Meituan -1%, BYD +2.44%, and JD.com HK -0.66%. Real estate was off -2.37% in Hong Kong and -0.98% after a small distressed Shanghai-listed developer will be delisted after failing exchange listing requirements. Hong Kong shorts were quiet while Mainland investors were a small net seller of Hong Kong stocks via Southbound Stock Connect. Some chatter that Italy might leave the Belt & Road initiative, though who knows! CNY and Asia dollar index were off versus the US dollar though rallying post the CPI print.

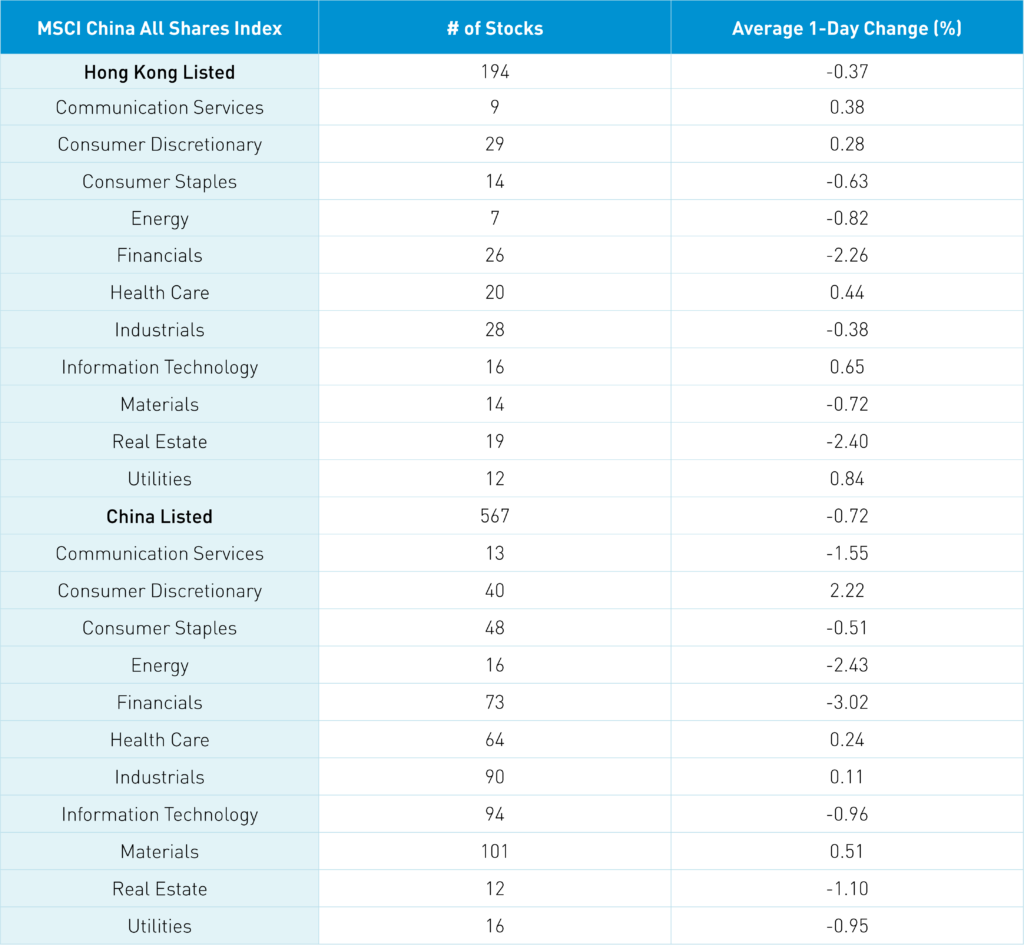

The Hang Seng and Hang Seng Tech diverged -0.53% and +0.34% on volume off -19% from yesterday which is 82% of the 1-year average. 236 stocks advanced while 248 declined. Main Board short turnover declined -13.16% which is 66% of the 1-year average as 13% of turnover was short turnover. The growth factor outperformed the value facto while small caps “outperformed” large caps. Top sectors were utilities +0.84%, tech +0.65%, and healthcare +0.44% while real estate -2.4%, financials -2.26%, and energy -0.82%. The top sub-sectors were autos, household products, and semis while banks, diversified financials, and insurance were the worst. Southbound Stock Connect volumes were light as Mainland investors sold $29 million of Hong Kong stocks while SMIC was a small net sell, and Tencent and Meituan were small net buys.

Shanghai, Shenzhen, and STAR Board were mixed -1.15%, +0.31%, and -0.82% on volume -17% from yesterday which is 110% of the 1-year average. 2,667 stocks advanced while 1,958 declined. The growth factor outperformed the value factor while small caps “outperformed” large caps. The top sectors were discretionary +2.22%, materials +0.51%, and healthcare +0.24% while financials -3.02%, energy -2.43%, and communication -1.55%. The top sub-sectors were the auto industry, auto parts, and education while computer hardware, oil/gas, and banking were the worst. Northbound Stock Connect volumes were moderate/high as foreign investors bought a healthy $804 million of Mainland stocks with Citic a small net sell, and Ping An and Kweichow Moutai small net buys. CNY and Asia's dollar slipped versus the US dollar. Shanghai copper and steel were both off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.92 versus 6.92 yesterday

- CNY per EUR 7.58 versus 7.58 yesterday

- Asia Dollar Index -0.02% overnight

- Yield on 10-Year Government Bond 2.72% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 2.89% versus 2.91% yesterday

- Copper Price -0.24% overnight

- Steel Price -0.59% overnight