Vipshop Reports Strong Q1 Results, China Officials Arrive in DC

3 Min. Read Time

Key News

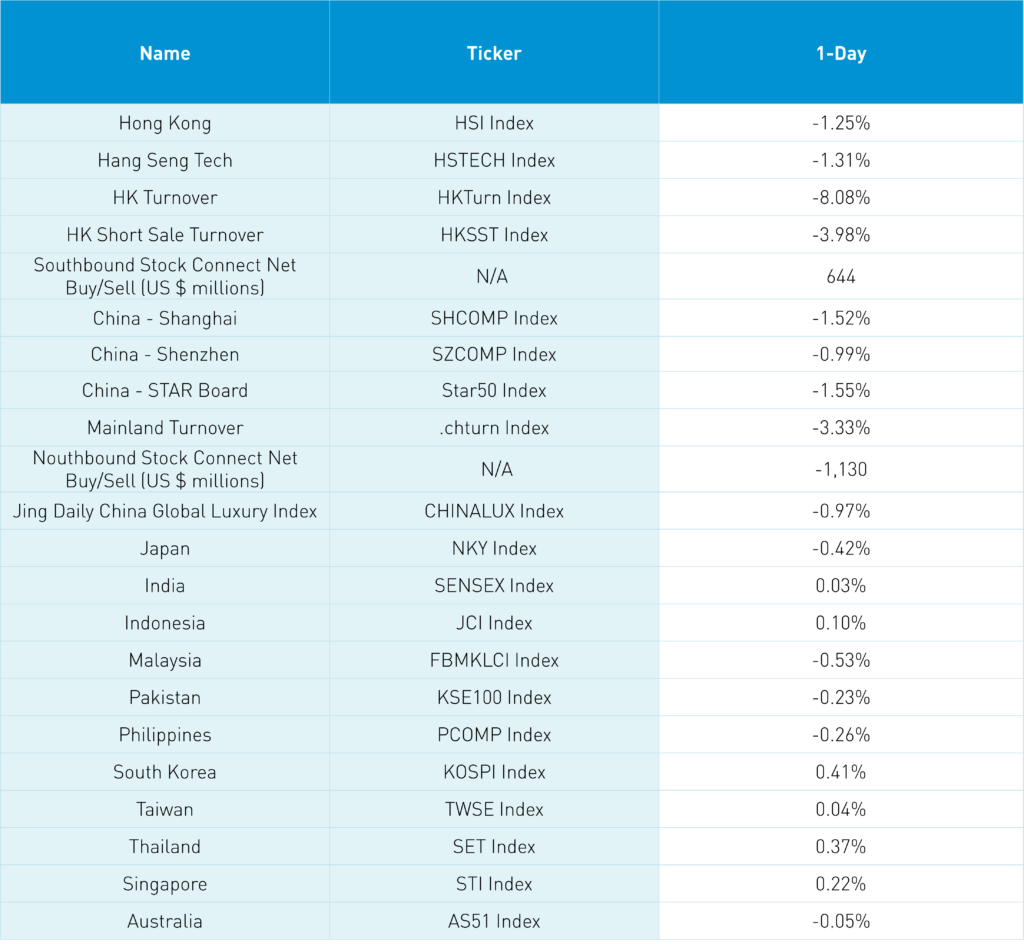

Asian equities were mixed overnight as Mainland China and Hong Kong underperformed on light volumes as investors watched the US debt ceiling drama unfold.

Political bickering weighed on Mainland China and Hong Kong as the US backtracked on some constructive G-7 comments while China officials expressed doubt over the “sincerity” of the US’ negotiation efforts, hitting back verbally on Japan’s semiconductor export limitations. This is very juvenile from both sides, in my opinion.

Meanwhile, China’s Ministry of Commerce Head and new Ambassador to the US Xie Feng are arriving in DC today. A meeting with Commerce’s Gina Raimondo and US Trade Representative Tsai will occur sometime this week, a positive step forward (green shoot).

As expected, the People’s Bank of China (PBOC) did not cut in the loan prime rate for the ninth consecutive month. Policymakers appear willing to let China’s economy come back incrementally without pressing on the stimulus gas pedal, though markets are anticipating a bank reserve requirement cut next month.

The US dollar’s recent strength continued overnight as CNY fell -0.34% to 7.05 CNY per USD and the Asia Dollar Index pulled an inverse James Bond to close lower by -0.07%. Both Mainland China and Hong Kong slowly slid over the course of the trading session after opening higher, driven by a lack of catalysts and buyers despite mainland investors buying $644 million worth of Hong Kong stocks through Southbound Stock Connect.

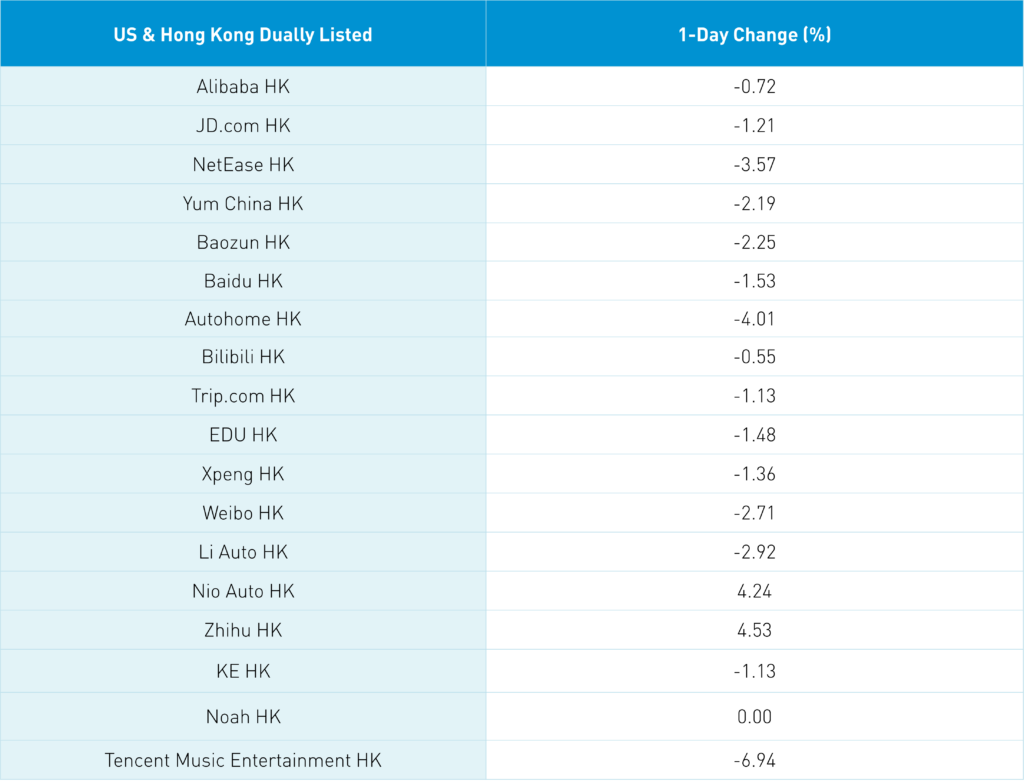

86 new game approvals including of Tencent’s Ace Fighter 2 and NetEase’s 7-Day World failed to excite investors. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.35%, Meituan, which gained +0.15% after launching in Hong Kong, Alibaba, which fell -0.72% as layoffs in its cloud unit were viewed negatively, Kuiashou, which gained +3.08% after yesterday’s strong results and buyback announcement from yesterday after turning profitable, and Ping An Insurance, which fell -3.46%.

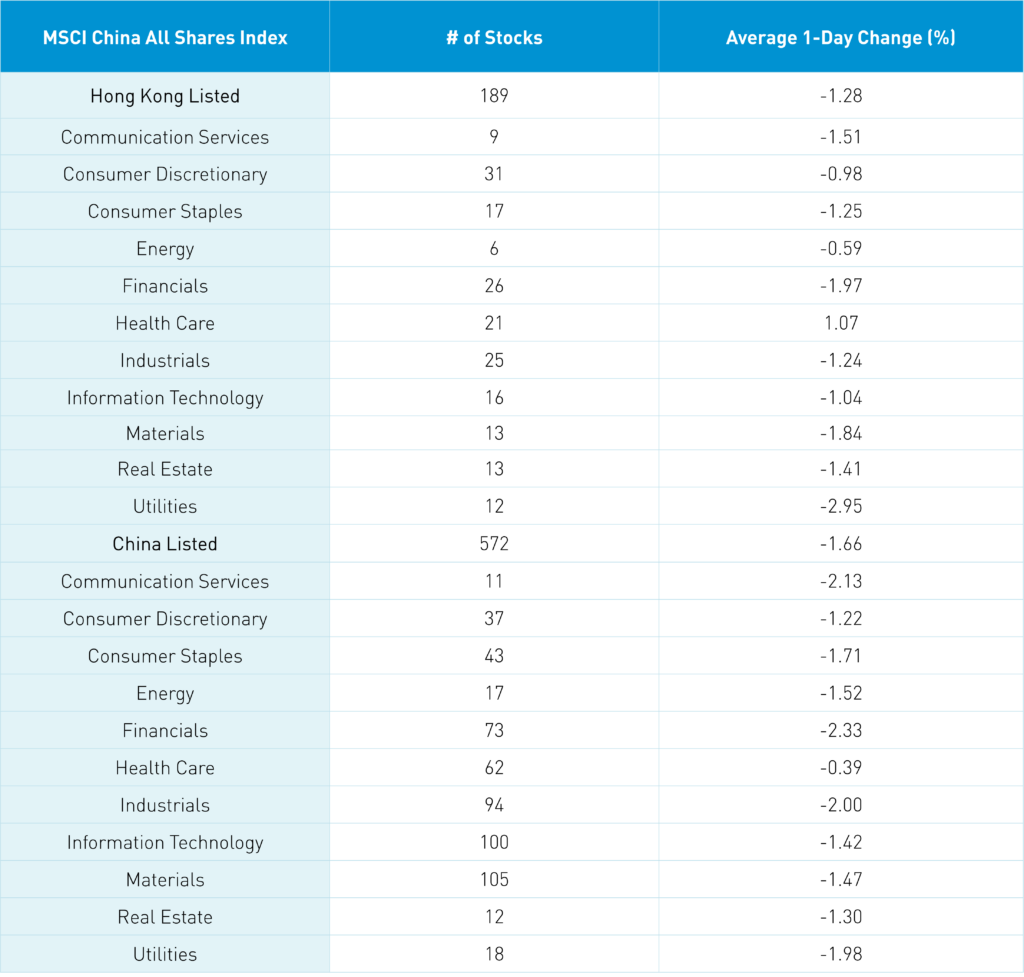

Financials were weak in both Hong Kong, down -2.01%, and Mainland China, down -2.32% as investors took profits in SOEs and high dividend payers. Healthcare was a rare positive today as Covid vaccinations expire, leading to another round of jabs. Foreign investors sold a healthy $1.13 billion worth of Mainland stocks via Northbound Stock Connect. The Hang Seng, Shanghai, and Shenzhen indexes are all sitting at support levels.

E-commerce company Vipshop (VIPS US) reported Q1 results before the US market open today, indicating strong growth as it beat estimates on revenue, which increased +9.1% year-over-year (YoY), adjusted net income, which gained +45% YoY, and adjusted earnings per share (EPS). Pinduoduo will report Q1 results tomorrow.

I received a great question at a conference that I attended yesterday, which was: can you trust China’s data? We really don’t need government data as there are plenty of other data sources that can help us understand what is happening economically. Besides our cell phones being mobile surveillance devices, there are a whole host of ways to receive real time economic data. Coincidentally, Yicai Global noted that 74 of 113 Chinese cities saw an increase in pollution levels, while air quality has dropped across 339 Chinese cities so far this year. As economic activity picks up post zero COVID, there is an unfortunate consequence: pollution.

The Hang Seng and Hang Seng Tech indexes fell -1.25% and -1.31%, respectively, on volume that decreased -8.08% from yesterday, which is 73% of the 1-year average. 121 stocks rose while 375 declined. Main Board short turnover fell -4% from yesterday, which is 71% of the 1-year average as 16% of turnover was short turnover. Value and growth factors were both down while small caps “outperformed” (i.e. fell less than) large caps. Healthcare was the only positive sector, gaining +1.06%, while utilities fell -2.96%, financials fell -1.98%, and materials fell -1.85%. Pharmaceuticals and healthcare equipment were the only positive subsectors, while media, utilities, and food were among the worst performers. Southbound Stock Connect volumes were light as Mainland investors bought $644 million worth of Hong Kong stocks as Tencent, Meituan, and Kuiashou were all small net buys.

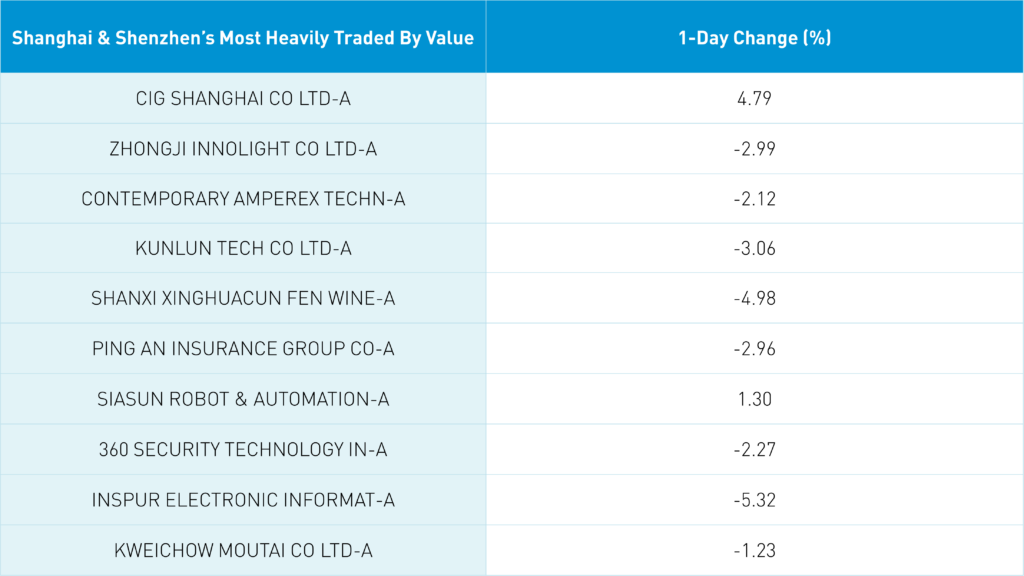

Shanghai, Shenzhen, and the STAR Board fell -1.52%, -0.99%, and -1.55%, respectively, on volume that decreased -3.33% from yesterday, which is 83% of the 1-year average. 1,441 stocks advanced while 3,225 stocks declined. Growth and value factors outperformed, though momentum was off while small caps “outperformed” (i.e. fell less) than large caps. All sectors were negative as financials fell -2.32%, communication services fell -2.12%, and industrials fell -1.98%. Pharmaceuticals and biotechnology were the only positive subsectors, while insurance, computer hardware, and telecom were among the worst. Northbound Stock Connect volumes were light as foreign investors sold a healthy net -$1.13 billion worth of Mainland stocks as Kweichow Moutai was a moderate net sell, Shanxi Fen Wine was a small net buy, and Ping An Insurance was a small net sell. CNY and the Asia dollar index fell -0.34% and -0.07%, respectively, versus the US dollar, while Treasury bonds rallied. Copper and Steel were off.

Happy birthday to my son Mac!

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.06 versus 7.03 yesterday

- CNY per EUR 7.59 versus 7.61 yesterday

- Yield on 1-Day Government Bond 1.44% versus 1.43% yesterday

- Yield on 10-Year Government Bond 2.70% versus 2.71% yesterday

- Yield on 10-Year China Development Bank Bond 2.86% versus 2.88% yesterday

- Copper Price -0.65% overnight

- Steel Price -0.47% overnight