Meituan & NetEase Beat, Debt Ceiling, US Dollar Weigh On Risk Assets

3 Min. Read Time

Key News

Asia had another rough night on the US debt ceiling concerns except for Taiwan, which rode Nvidia’s earnings higher.

Ironically, the debt ceiling is driving the US dollar higher as the Asia Dollar Index fell overnight along with China’s Renminbi. The US dollar’s strength has weighed on stocks globally, except for the US, over the last month though it makes foreign goods and commodities cheaper, which should help lower inflation. Mainland China and Hong Kong were down following the performance of US-listed China stocks yesterday, as the debt ceiling and US-China political rhetoric were not helping.

There was talk about taking down risk, i.e., selling stock before the US’ three-day weekend due to debt ceiling uncertainties as the Hang Seng Index closed below 19k.

I am a bit surprised by Western media headlines on COVID in China as one Chinese scientist said there might be a springtime uptick. Data on metro usage in major Chinese cities show no change in behavior though we’ll keep an eye on this. A Western media headline on a UFO landing in Tiananmen Square would not surprise me at this point.

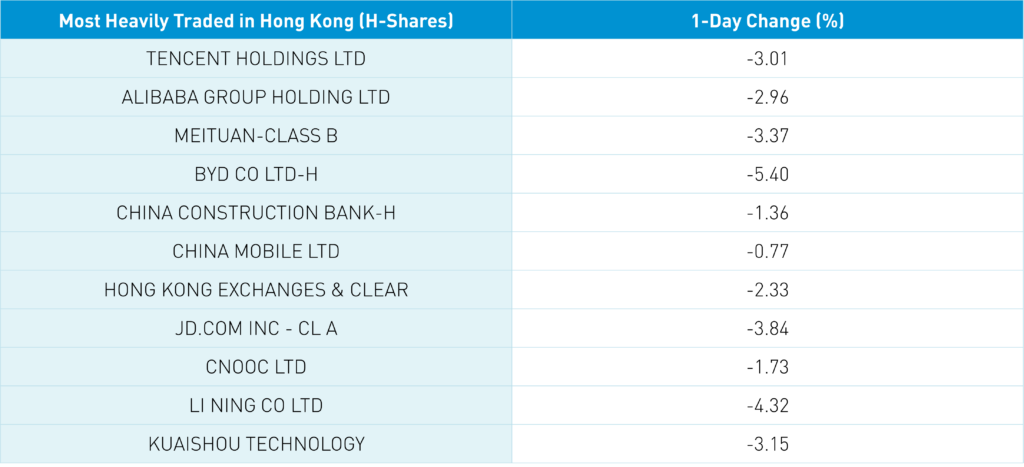

With buyers sitting on the sidelines, this selling pressure continues to weigh on stocks as Hong Kong only had 63 stocks up today while 430 fell and 34 were unchanged. Exhibit A would be foreign investors’ sale of $1.4 billion worth of Mainland stocks overnight via Northbound Stock Connect. Yesterday, we mentioned that a huge, almost $500 million, sale in the Hong Kong-listed Hong Kong Tracker ETF. Hong Kong short sale volume picked up overnight to 18% of total Main Board turnover, but is not that high considering the aggregate volumes as short sellers remember never to be short a dull market. Mainland China managed a late afternoon rally which trimmed losses. Nvidia’s results garnered much attention though Lenovo (992 HK) -1.38% driven by weak global demand for personal computers, which fell 29% year over year and below levels in 2019 and 2018—interesting public spat as Great Wall Motor accuses BYD of overstating zero emission.

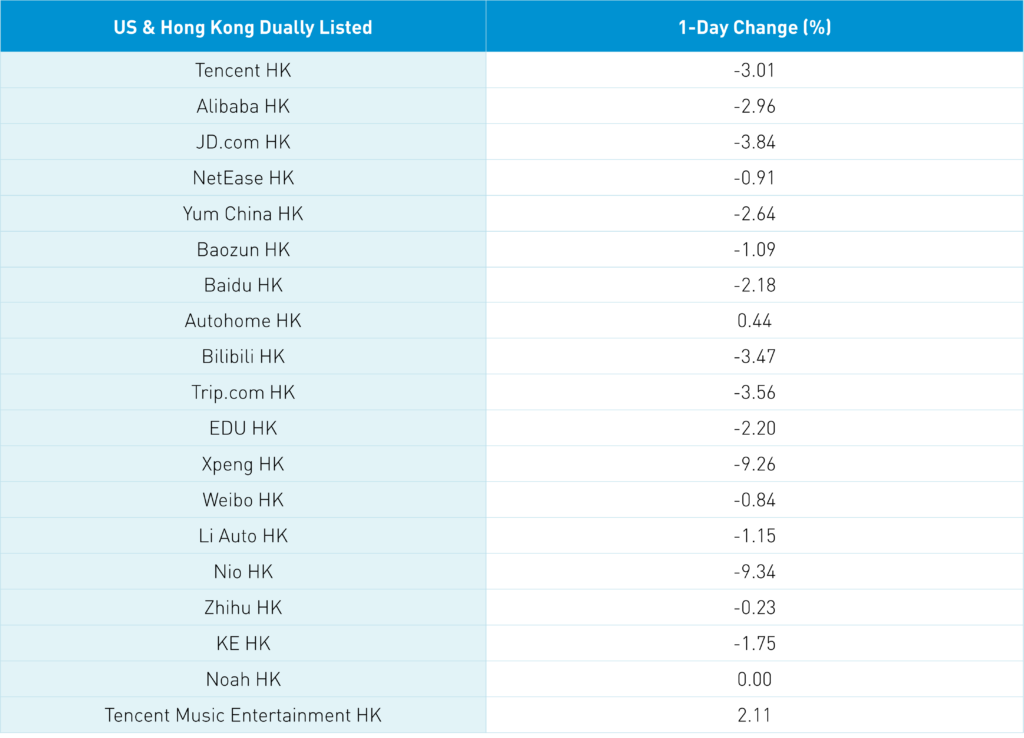

After the Hong Kong close, Meituan and NetEase beat analyst expectations on the big three: revenue, adjusted net income, and adjusted EPS, with the former swinging to a profit in a great sign. Meanwhile, Weibo's results were mixed.

Meituan Earnings:

- Revenue +26.7% to RMB 58.617B from Q1 2022’s RMB 46.268B versus analyst expectations of RMB 57.476B.

- Adjusted net income was RMB 5.491B from a loss of (RMB 3.586B) a year ago versus analyst expectations of RMB 1.948B. Adjusted EPS was RMB 0.89 versus analyst expectations of RMB 0.28.

NetEase Earnings:

- Revenue +6.3% to RMB 25B from RMB 23.555B and analyst expectations of RMB 24.806B.

- Adjusted net income increased to RMB 7.566B from RMB 5.117B and analyst expectations of RMB 5.697B

- Adjusted EPS was RMB 11.74 from RMB 7.81, and analyst expectations of RMB 8.57.

- NetEase increased both its dividend and stock repurchase.

Weibo Earnings:

- Revenue decreased -15% to $413 million from $484 million and analyst expectations of $413 million.

- Adjusted net income decreased to $111. million from $132 million versus analyst expectations of $10 million.

- Adjusted EPS was $0.47 from $0.56 versus analyst expectations of $0.43.

- Weibo announced a special dividend of $0.85 versus yesterday’s closing price of $16.06.

Baidu's spin off of its short video platform will list in Hong Kong.

China’s Ministry of Commerce is expected to meet with the US Secretary of Commerce Raimondo and US Trade Representative Tsai today and tomorrow.

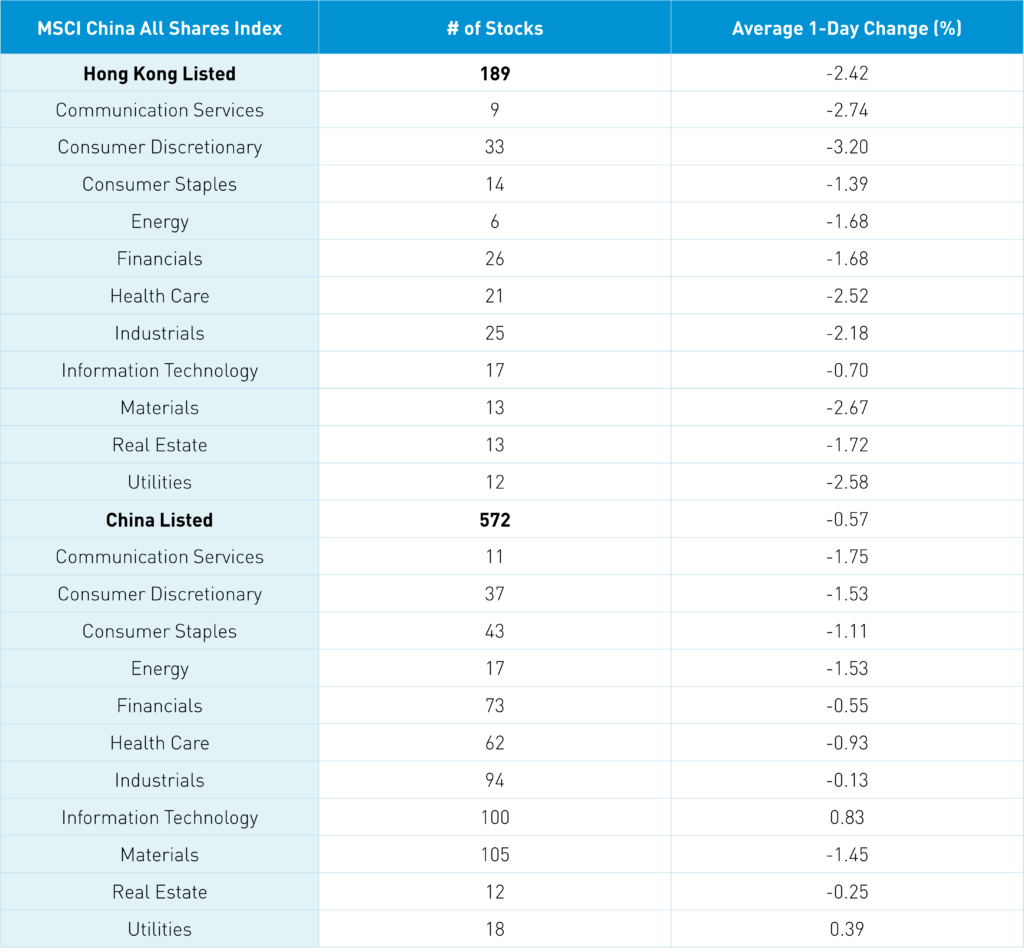

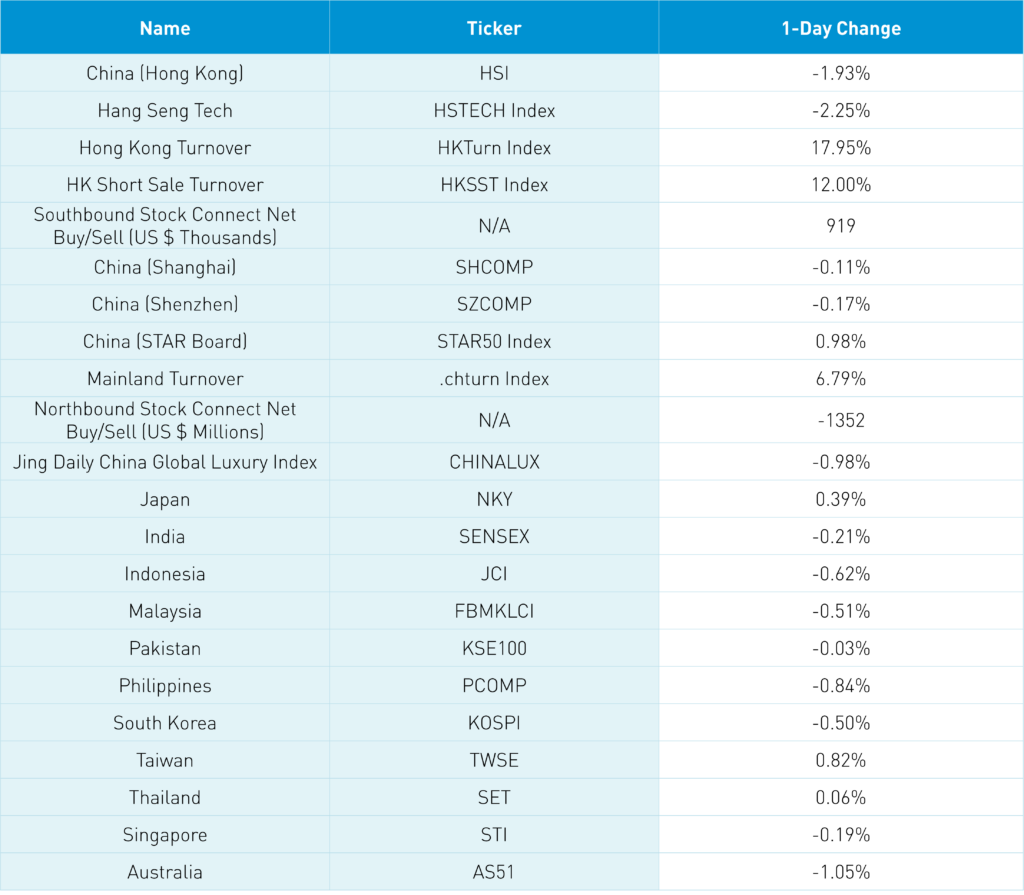

The Hang Seng and Hang Seng Tech indexes fell -1.93% and -2.25%, respectively, on volume that increased +17.95% from yesterday, which is 97% of the 1-year average. 63 stocks advanced, while 430 declined. Main Board short turnover increased +11.97% from yesterday, 104% of the 1-year average, as 18% of turnover was short turnover. The value factor fell less than the growth factor; small caps “outperformed”/fell less than large caps. All sectors were down, as consumer discretionary -3.19%, communication -2.73%, and materials -2.66%. Media was the only positive sub-sector, while auto, retailing, and software were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $919mm of Hong Kong stocks, with Tencent a large net buy, Meituan a moderate net buy, and Kuiashou a small net sell.

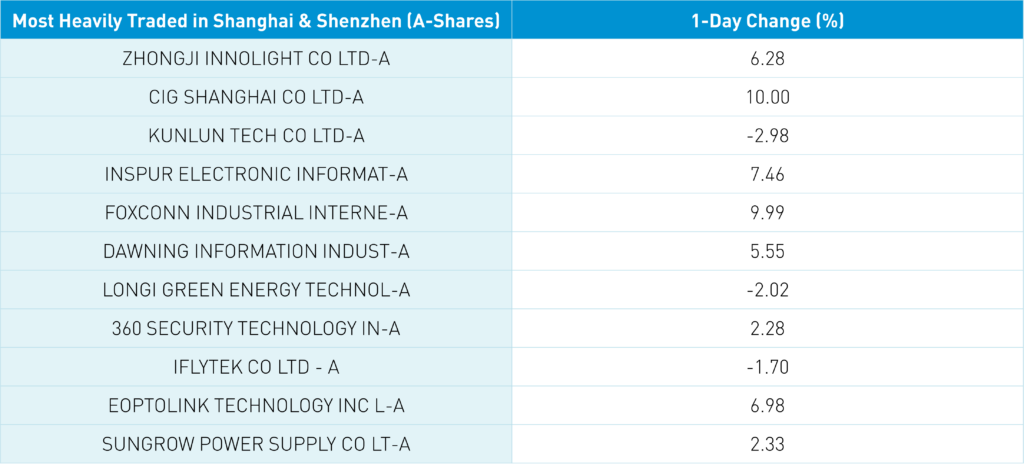

Shanghai, Shenzhen, and the STAR Board diverged to close -0.11%, -0.17%, and +0.98%, respectively, on volume that increased +6.79% from yesterday, which is 92% of the 1-year average. 1,313 stocks advanced, while 3,358 stocks declined. Growth factors outperformed value factors as small caps outpaced large caps. Tech and utilities gained +0.8% and +0.36%, while communication -1.78%, discretionary -1.55%, and energy -1.55%. The top sub-sectors were computer hardware, power generation equipment, and gas, while internet, cultural media, and precious metals were the worst. Northbound Stock Connect volumes were light/moderate as foreign investors sold $1.352B of Mainland stocks, with Foxconn a very small net sell, Longi Green and Kweichow Moutai moderate net sells. CNY and the Asia dollar index fell versus the US dollar as Treasury bonds fell. Copper and steel had another rough day.

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.07 versus 7.05 yesterday

- CNY per EUR 7.59 versus 7.59 yesterday

- Asia Dollar Index -0.21% overnight

- Yield on 10-Year Government Bond 2.71% versus 2.70% yesterday

- Yield on 10-Year China Development Bank Bond 2.87% versus 2.87% yesterday

- Copper Price -1.08% overnight

- Steel Price -2.30% overnight