Elon Musk Visits China With Jamie Dimon On Deck

4 Min. Read Time

Key News

Asian equities were mixed overnight on light volumes as the US debt ceiling continues to weigh on sentiment despite progress. Hong Kong and Mainland China posted small gains after the former fell yesterday.

The big news in China was Elon Musk's arrival in Beijing, where he met with Foreign Minister Qin Gang before heading to Shanghai to visit the Tesla factory. The Financial Times is also reporting that JP Morgan CEO Jamie Dimon will visit China next week for the firm’s China conference, which includes executives from Starbucks, Pfizer, Baidu, and Geely.

Following the meetings between US Commerce Secretary and her China counterpart, the US and China appear to be having difficulty getting their defense ministers to meet due to US sanctions on China’s defense minister. Removing these sanctions requires informing Congress first. Communication could lead to a meeting between Biden and Xi at the Asia Pacific Economic Cooperation (APEC) meetings in San Francisco in November. Ultimately, it highlights how well business people are getting along by getting on airplanes and meeting face to face.

Weighing on China’s markets has been the lack of stimulus measures as the economy slowly rebounds, which has disappointed the market. China’s official PMIs will be released Wednesday with some chatter that economic activity has stabilized. Real estate had a decent day though overhang and concern remain.

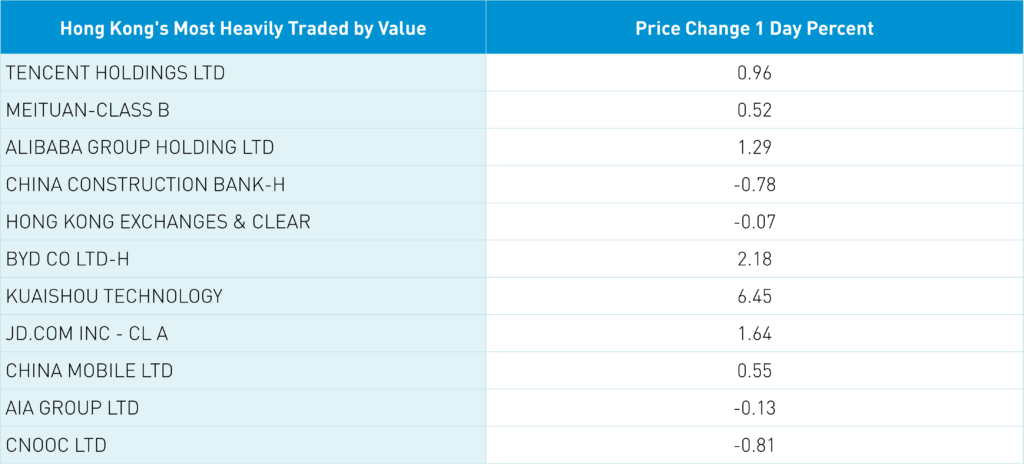

Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.96%, Meituan, which gained +0.52%, and Alibaba, which gained +1.29%, Tencent, which fell -2.85%, and Alibaba, which fell -1.08%. Internet companies should note NetEase’s +7.2% gain yesterday and -0.29% decline today, as investors like the company’s dividend while many companies buy back stock. Remember, tomorrow is MSCI’s Semi-Annual Index Review, requiring passive investors to trade at the market’s close so their index funds and ETFs in order to match the refreshed index. Alibaba's Hong Kong shares are a big net buy, which will likely make it Hong Kong’s most heavily traded stock tomorrow though I am not predicting it will go up or down. Education stocks had a good day after President Xi spoke about the importance of strengthening the educational system. The Mainland market also had a quiet night with foreign investors buying $91 million worth of Mainland stocks.

An article’s comment section provides a rudimentary sentiment gauge. Spending the time to write a comment following an article is the modern equivalent of writing to the local newspaper. It is far easier to comment than write a letter though it does indicate the writer has an opinion on the subject or a lot of time on their hands. In reading a pessimistic article on China’s economy over the weekend, I couldn’t help but notice the comments following the article criticized the article for its lack of evidence and poor thesis. In light of recent issues like the debt ceiling, Fed hikes, inflation, etc., the "blame China" narrative is getting a little long in the tooth. I could not help but laugh during a TV interview of a long-running politician blaming the US debt ceiling on China despite his tenure in office for the last twenty-plus years. The distraction technique of blaming China instead of looking in the mirror might be running out of steam. We shall see!

The Hang Seng and Hang Seng Tech indexes gained +0.24% and +1.5%, respectively, on volume that decreased -14.43% from yesterday, which is 79% of the 1-year average. 266 stocks advanced while 220 declined. Main Board short turnover declined -21% from yesterday, which is 78% of the 1-year average. The growth factor outperformed the value factor while small caps outpaced large caps. The top sectors were communication services, which gained +1.19%, consumer staples, which gained +1.14%, and consumer discretionary, which gained +1.03%. Meanwhile, materials fell -0.88%, energy fell -0.57%, and utilities fell -0.46%. The top subsectors were food, auto, and consumer services, while household products, transportation, and healthcare equipment were among the worst. Southbound Stock Connect volumes were very light as Mainland investors bought a net $179 million worth of Hong Kong stocks as Kuaishou was a very small net sell, and Tencent and Meituan were small/moderate net buys.

Shanghai, Shenzhen, and the STAR Board gained +0.09%, +0.49%, and +1.56%, respectively, on volume that increased +1.47% from yesterday. 2,181 stocks advanced while 2,465 declined. The value factor outperformed the growth factor while large caps outpaced small caps. The top sectors were communication, which gained +3.15%, real estate, which gained +1.29%, and industrials, which gained +1.05%. Meanwhile, consumer staples fell -1.14%, healthcare fell -1.1%, and energy -0.47%. The top-performing subsectors were computer hardware, internet, and cultural media, while soft drinks, liquor, and steel were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $91 million worth of Mainland stocks as Foxconn was a very small net buy, Longi Green Energy was a small net sell, and Kweichow Moutai was a moderate net sell.

After yesterday’s Memorial Day holiday, many thanks to those who served in the US military and their families. A shoutout to those close to me who served including my father, and my friends Craig and Matt!

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.07 versus 7.06 Friday

- CNY per EUR 7.59 versus 7.58 Friday

- Asia Dollar Index -0.04% overnight

- Yield on 10-Year China Development Bank Bond 2.70% versus 2.72% Friday

- Yield on 10-Year China Development Bank Bond 2.88% versus 2.89% Friday

- Copper Price +0.00% overnight

- Steel Price -0.17% overnight