Multiple Catalysts Lift Markets, Week in Review

4 Min. Read Time

Week in Review

- Asian equities ended a relatively positive week on a high note as internet stocks rebounded following a slump earlier in the week on high short volumes and index rebalancing.

- Multiple China economic releases this week painted a mixed picture as the Caixin (private) manufacturing PMI outpaced the official measure as the latter indicated expansion while the former indicated contraction.

- EV sales data from multiple companies was released on Thursday with BYD seeing strong sales of one million units so far this year.

- Multiple foreign executives were in China this week including Tesla’s Elon Musk and JP Morgan’s Jamie Dimon.

Friday’s Key News

Hong Kong outperformed the region on strong volume led by internet stocks.

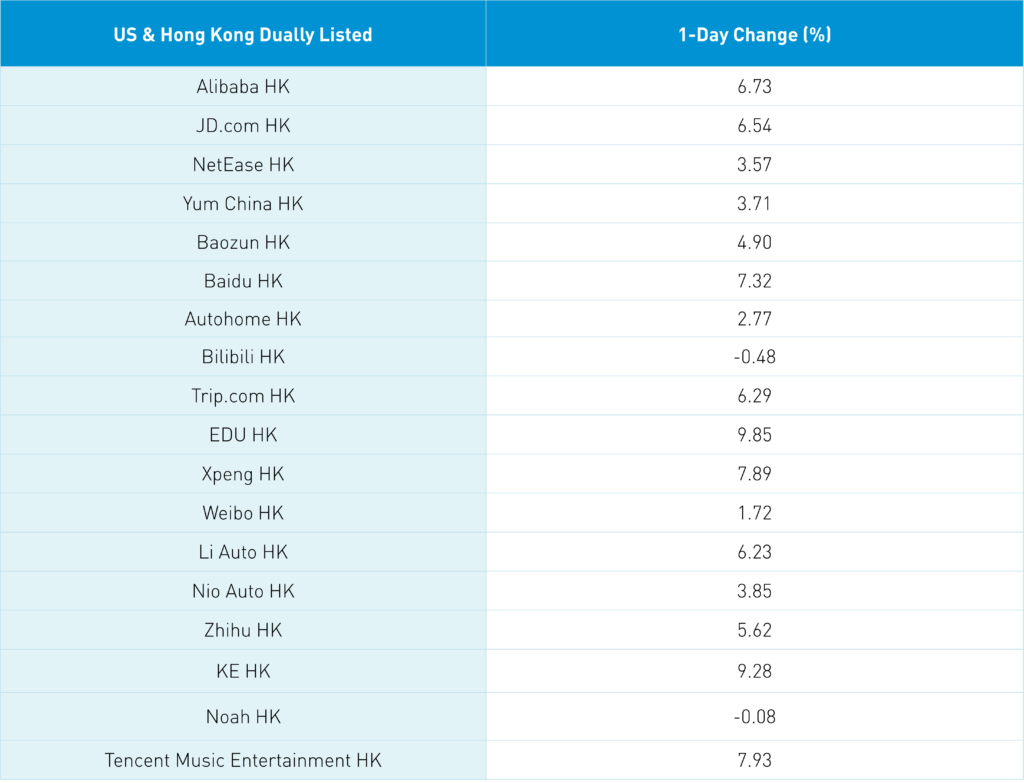

Was there short covering overnight in Hong Kong? 100%, as we noted the uptick in short volumes all this week. More importantly, we had positive catalysts that brought buyers back in. US-listed China stocks gained yesterday on strong initial results from JD.com’s 618 Grand Promotion shopping festival.

Alibaba’s November 11th “Singles Day” shopping event is well known, though JD.com’s competing 618 event is similar in offering discounts to consumers. The early strong results indicate that reports of the death of the Chinese consumer have been grossly exaggerated.

Also, the Caixin Manufacturing PMI beat expectations yesterday, remaining in growth territory, which received ZERO media attention yesterday. “If it bleeds it leads” as the “official” PMI’s miss was headlines news earlier in the week. Did you see any articles on the Caixin PMI’s beat? Me neither.

May electric vehicle (EV) sales figures, especially BYD’s numbers, have also helped as there are rumors that there might be further EV policy support coming. Markets also liked the belief that Fed hiking in June and July, and then pausing, highlighted in yesterday’s note, also helped. CNY and the Asia Dollar Index gained +0.57% and +0.59%, respectively, versus the US dollar on the potential pause. A resolution on the US debt ceiling is an obvious positive as well.

These positives come against the backdrop of low China ownership among asset allocators, especially in the United States. Several strategists I respect have noted that China ownership levels have fallen back to October 2022 levels. Of course, the market does what is least expected, i.e. the pain trade is higher (fingers crossed). Wednesday’s fall may have been a capitulation bottom, especially in Hong Kong, though both Shanghai and Shenzhen are sitting on support levels (fingers still crossed). Overall, I believe we are more likely to see good news going forward, except for China’s manufacturing weakness due to slowing global growth.

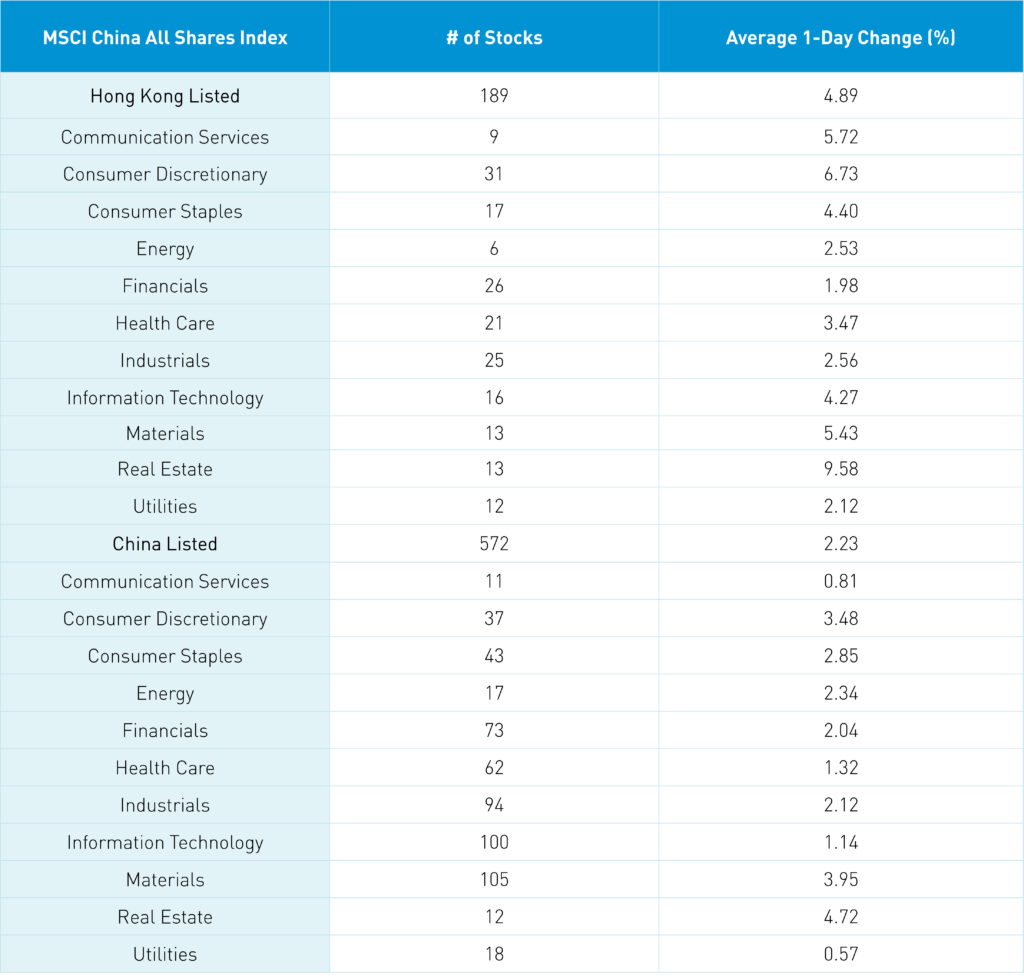

Real estate was the best performing sector in both Hong Kong, where it gained +9.58%, and Mainland China, where it gained +4.43% on chatter that property stimulus is coming. After the close in Hong Kong, Bloomberg reported that policy makers are working on more real estate measures. Sluggish property sales and declining property prices have not only weighed on consumer confidence, but also have upstream and downstream economic effects. Building stuff requires cement, steel, copper, etc., which explains the pop in commodity prices overnight.

Northbound Stock Connect inflow was a strong at $1.2 billion overnight, though it was interesting that Mainland investors were net sellers of Hong Kong stocks via Southbound Stock Connect. Tencent and Meituan were moderate net buys via Southbound Stock Connect overnight.

LVMH CEO Bernard Arnault is expected to visit China.

Meanwhile, Bloomberg had an interesting article on Exxon’s success in China. The oil giant is investing $10 billion to build a petrochemical plant in the country. Exxon has been doing business in China since 1892, according to Exxon’s China head Fernando Vallina.

Nvidia’s Jensen Huang is expected to visit China this month. Businesspeople are getting along just fine as they are getting on planes and meeting with one another. Might be time for politicians to do the same!

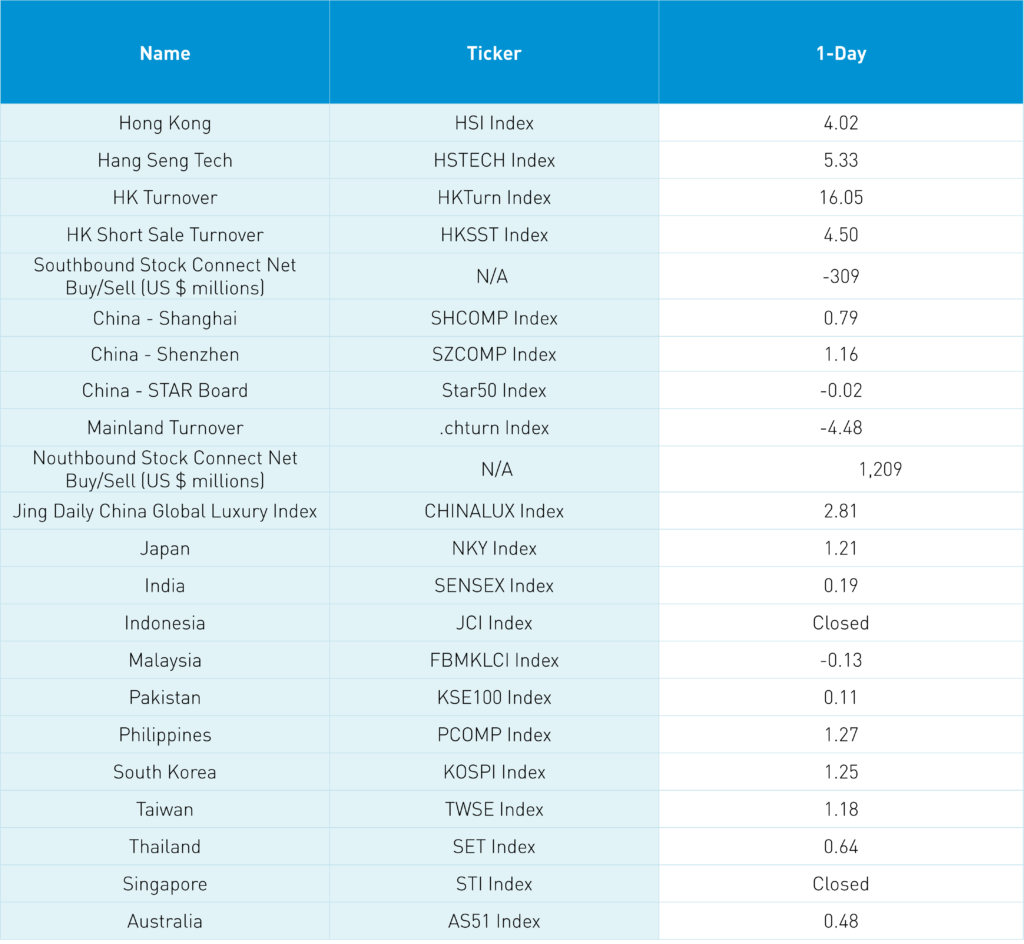

The Hang Seng and Hang Seng Tech indexes gained +4.02% and +5.33%, respectively, on volume that increased +16.05% from yesterday, which is 126% of the 1-year average. 470 stocks advanced while 49 stocks declined. Main Board short turnover increased +4.5% from yesterday, which is 119% of the 1-year average, as 16% of turnover was short turnover. Growth factors outperformed value factors, as small caps outpaced large caps. All sectors were positive as real estate gained +9.57%, consumer discretionary gained +6.72%, and communication services gained +5.71%. All subsectors were positive as retail, software, and real estate were the top performers. Southbound Stock Connect volumes were moderate/high as Mainland investors sold a net -$309 million worth of Hong Kong stocks as Kuiashou was a small net buy, and Tencent and Meituan were moderate/large net buys.

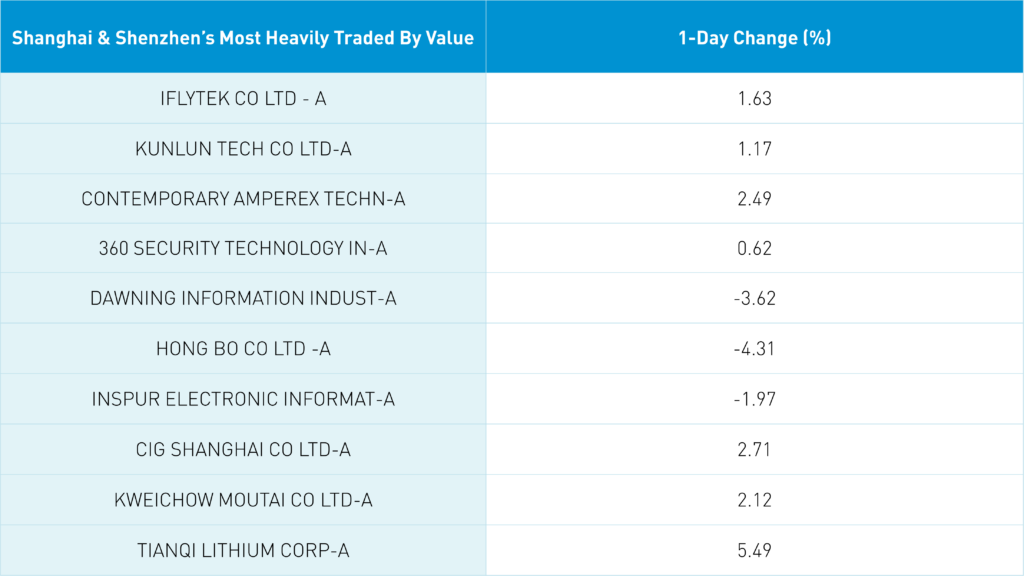

Shanghai, Shenzhen, and the STAR Board diverged to close +0.79%, +1.16%, and -0.02%, respectively, on turnover that decreased -4.48% from yesterday, which is 101% of the 1-year average. 3,264 stocks advanced while 1,411 stocks declined. Growth and value factors both performed well, while small caps outpaced large caps. All sectors were positive as real estate gained +4.68%, materials gained +3.91%, and consumer discretionary gained +3.44%. The top-performing subsectors were household products, household appliances, and building materials. Meanwhile, computer hardware, aerospace/military, and education were among the worst. Northbound Stock Connect volumes were moderate as foreign investors bought a healthy $1.209 worth of Mainland stocks as Kweichow Moutai a moderate/large net buy, Ping An insurance was a moderate/small net sell, and China Tourism Group Duty Free was a small net sell. CNY and the Asia Dollar Index gained +0.57% and +0.59%, respectively, versus the US dollar. Treasury bonds sold off, while copper and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.08 versus 7.10 yesterday

- CNY per EUR 7.61 versus 7.64 yesterday

- Asia Dollar Index +0.59% overnight

- Yield on 1-Day Government Bond 1.50% versus 1.57% yesterday

- Yield on 10-Year Government Bond 2.70% versus 2.68% yesterday

- Yield on 10-Year China Development Bank Bond 2.85% versus 2.84% yesterday

- Copper Price +0.98% overnight

- Steel Price +1.60% overnight