Trip.com Takes Flight on +180% Revenue Increase YoY, Caixin Services PMI Misses Expectations

3 Min. Read Time

Key News

Asian equities were largely higher except for Mainland China and Hong Kong, which reversed their strong gains from yesterday.

While the US was enjoying the Labor Day holiday on Monday, Hong Kong and Mainland China outperformed in Asia, as Shanghai was higher by +1.4%, Shenzhen was up +1.44%, the Hang Seng was up +2.51%, and the Hang Seng Tech Index increased +3.12%. Yesterday’s strong move was accompanied by a net $548 million worth of Mainland buying of Hong Kong-listed ETFs and stocks. This was mirrored by a very healthy and rare net purchase of Mainland stocks by foreign investors through Northbound Stock Connect, to the tune of $946 million on Monday.

Yesterday, investors cheered the mortgage and home purchase reforms that sent US-listed China stocks higher on Friday. What a difference a day makes! The August Caixin Services PMI came in at 51.8, missing expectations of 53.6 as growth slowed month over month from July’s 54.1, driven by the one-two punch of weak foreign demand combined with weak internal demand.

China’s renminbi was a headwind to risk assets as CNY fell from Friday’s 7.26 to 7.30 today. We know the reforms being implemented will take time to filter through the economy, as September housing sales and mortgage refinances will be interesting to see. Nanjing and Qingdao released further information on their land purchases and mortgage interest rates.

Foreign investors were net sellers of Mainland stocks overnight, though Mainland investors bought a healthy $1.51 billion of Hong Kong-listed ETFs and stocks, with the Hang Seng Tracker ETF seeing a very large net buy inflow. It was a very weak day in both markets, with real estate weak despite Country Garden avoiding default for the time being. It is interesting that Hong Kong-listed distressed real estate developer Sunac was up +25% today following yesterday’s gain of +34.19% as it was added to Southbound Stock Connect.

Hong Kong’s main board short turnover was high at 23% of total turnover with several Hong Kong-listed ETFs seeing high short turnover percentages.

Premier Li will attend the G20 in India instead of President Xi, likely leading to a Biden-Xi meeting at the APEC conference in San Francisco in November.

Trip.com (TCOM US, 9961 HK) reported Q2 revenue of RMB 11.2B, which represents an increase of +180% year-over-year, exceeding pre-COVID levels in 2019 by 29% versus estimates of RMB 10.78B and Adjusted EPS of RMB 5.11 versus estimates of RMB 3.64. The company's earnings dovetail well on the Ministry of Transport's report that passenger volume increased in August by +1.7% from July and +38.4% year over year.

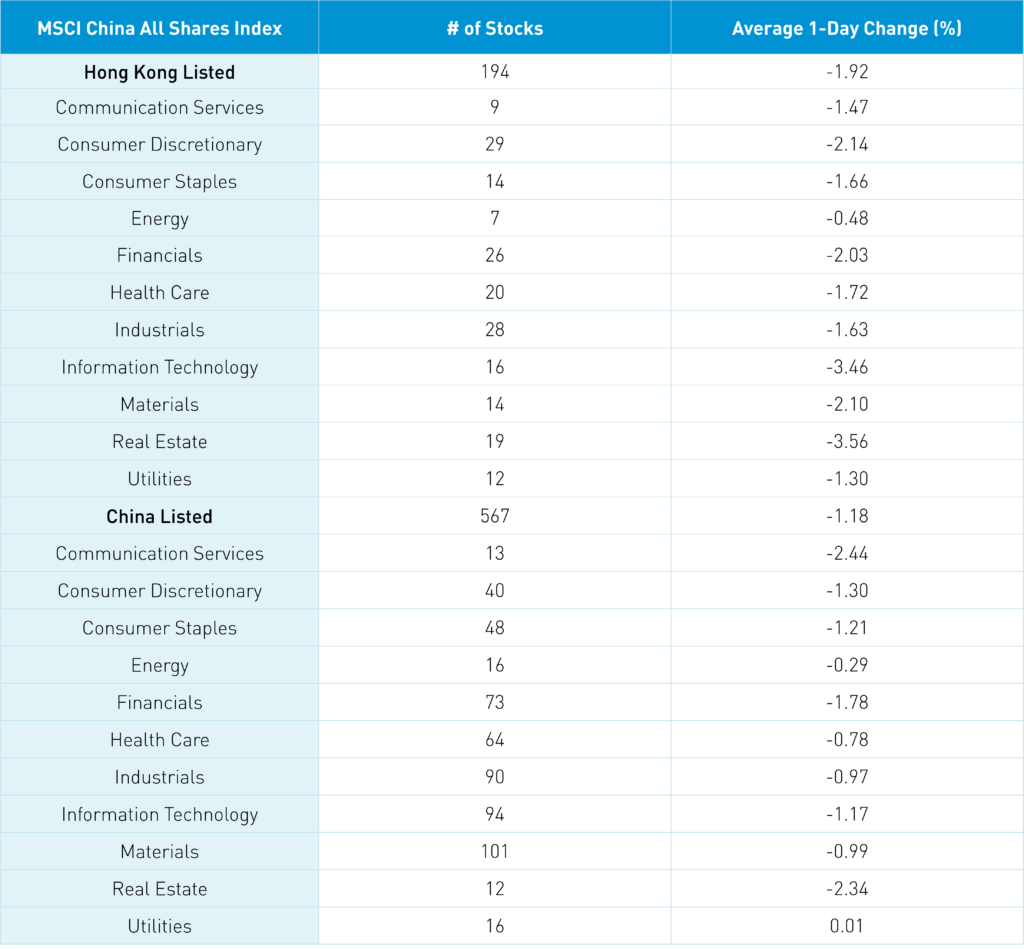

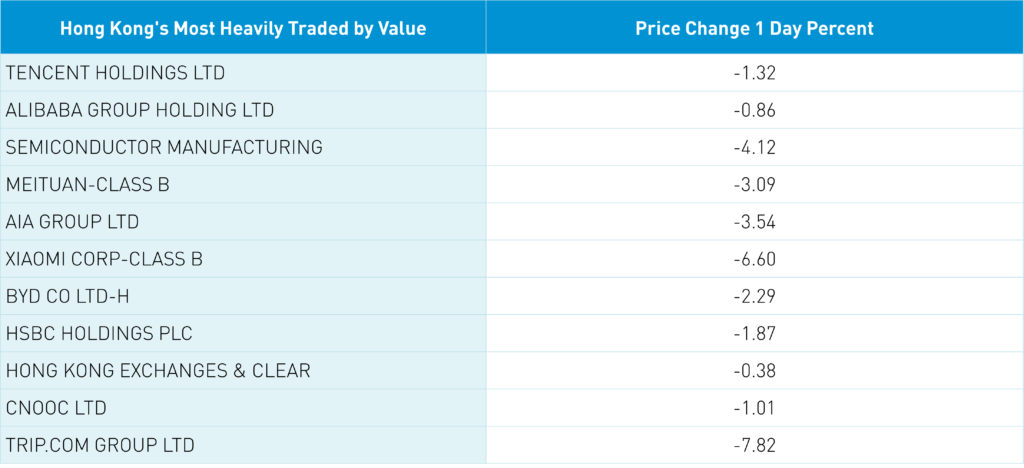

The Hang Seng and Hang Seng Technology indexes fell -2.06% and -2.59%, respectively, on volume that decreased -33.53% from yesterday, which is 96% of the 1-year average. 76 stocks advanced, while 420 declined. Main Board short turnover decreased -4.84% from yesterday, which is 124% of the 1-year average. The growth factor outperformed the value factor, while large caps outpaced small caps. All sectors were negative, as real estate fell -3.57%, technology fell -3.46%, and consumer discretionary fell -2.15%. All subsectors were negative, as household products, technical hardware, and insurance were among the worst-performing. Southbound Stock Connect volumes were moderate/high as Mainland investors bought a net $1.51 billion of ETFs and stocks. The most heavily-bought stocks included ZJLD Group, Sinopec, and CNOOC. Meanwhile, Semiconductor Manufacturing International Co. (SMIC), Li Auto, and Meituan all saw light net selling.

Shanghai, Shenzhen, and the STAR Board fell -0.71%, -0.58%, and -1.25%, respectively, on volume that decreased -9.55% from yesterday, which is 91% of the 1-year average. 1,363 stocks advanced, while 3,337 stocks declined. The growth factor “outperformed” the value factor, while small caps “outperformed” large caps. Utilities constituted the only positive sector, up +0.41%. Meanwhile, communication services fell -2.45%, real estate fell -2.35%, and financials fell -1.8%. The top-performing subsectors included electric power, coal, and motorcycles. Meanwhile, insurance, real estate, and cultural media were among the worst-performing. Northbound Stock Connect volumes were light as foreign investors sold a net -$631 million worth of Mainland stocks. Kweichow Moutai, CATL, and Zhongji Innolight were all moderate net buys. Meanwhile, Wuliangye Yibin, and Sevenstar Electronics were all saw light net selling. CNY and the Asia Dollar Index fell versus the US dollar. Copper and steel were lower overnight.

Last Night's Performance

We have added the Morningstar Developed Markets China & Emerging Markets Revenue Exposure Index, which tracks the performance of developed market companies with high revenue exposure to China and other emerging markets, to our daily performance tracker.

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.30 versus 7.27 yesterday

- CNY per EUR 7.85 versus 7.85 yesterday

- Yield on 1-Day Government Bond 1.45% versus 1.45% yesterday

- Yield on 10-Year Government Bond 2.62% versus 2.62% yesterday

- Yield on 10-Year China Development Bank Bond 2.75% versus 2.75% yesterday

- Copper Price -0.69% overnight

- Steel Price -0.13% overnight