The “Good Stuff” Outperforms, Biden-Xi Summit Odds Increase

3 Min. Read Time

Key News

Asian equities were mixed overnight as growth stocks outperformed the region.

Mainland China and Hong Kong had a sneakily strong day as Mainland China’s outperformance was driven by high volume, which broke the RMB 1 trillion level for the first time since the end of August. The growth factor outperformed significantly in both Mainland China and Hong Kong, led by growth sectors including technology and health care. Large, diversified China indices had a decent day as value (i.e. low to no-growth) sector weights such as financials and energy were hit as investors favored what we call the “good stuff” i.e. growth stocks that look and feel like their US equivalents.

Healthcare was a leading sector in Hong Kong and Mainland China on positive earnings and new drug approvals in the US and China. We saw positive earnings momentum from Mindray, which gained +6.48%, and Pharmaron, which gained +12.6%. Innovent’s positive obesity drug trial led to a gain of +4.56% for the stock. Meanwhile, Junshi Biosciences gained +5.47% in Mainland China and 8.22% in Hong Kong.

Meanwhile, weak results from China Merchants Bank and HSBC weighed on banks.

Huawei’s ecosystem and tech subsectors including semiconductors rallied on the company’s strong Mate 60 and Mate 60 Pro sales, which came at the expense of Apple. One month ago, we noted Apple’s stock fall had nothing to do with the media’s “Chinese government ban,” but rather the strong release from Huawei.

A Biden-Xi summit looks likely following Foreign Minister Wang Yi’s Washington, DC trip that included a meeting with President Biden and Secretary of State Blinken. While the “path to San Francisco won’t be easy,” according to Wang, directionally, things are clearly improving. However, the “path” to San Francisco will be easy as more flights between the US and China have gone into service.

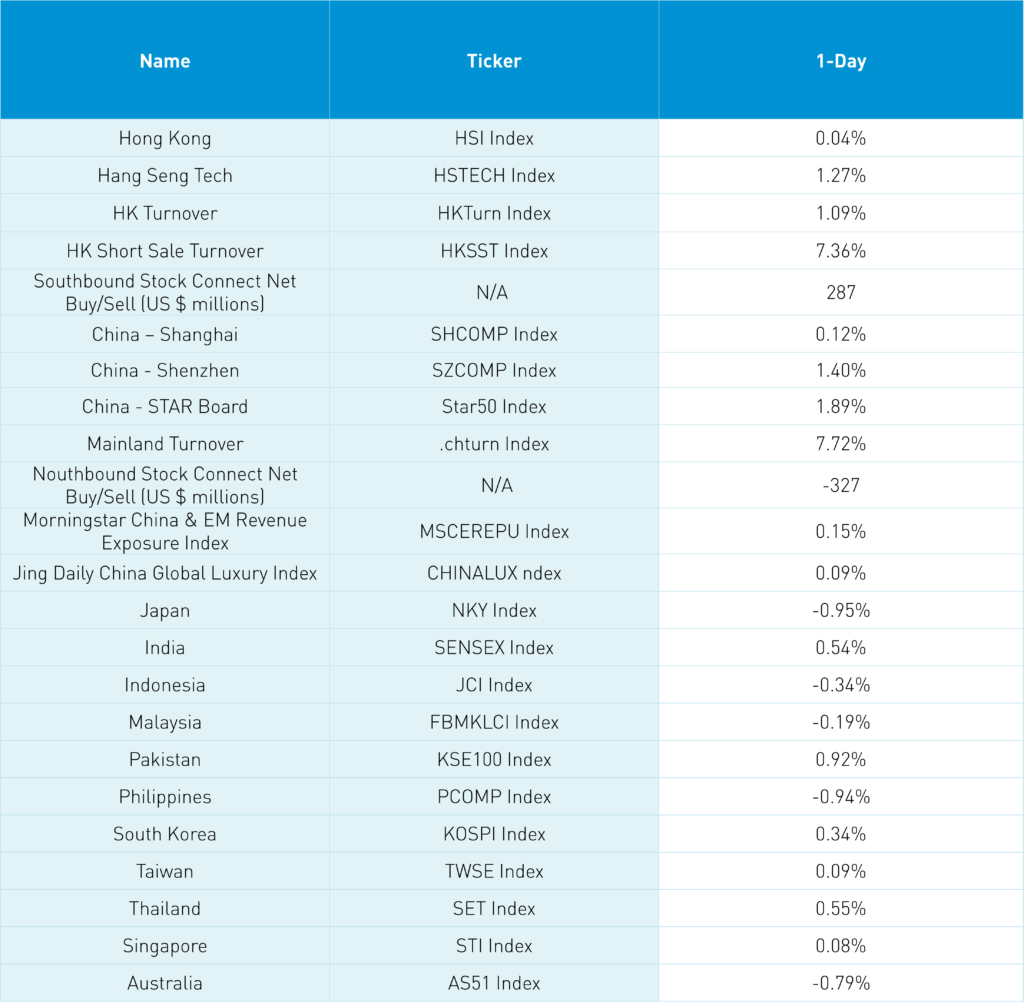

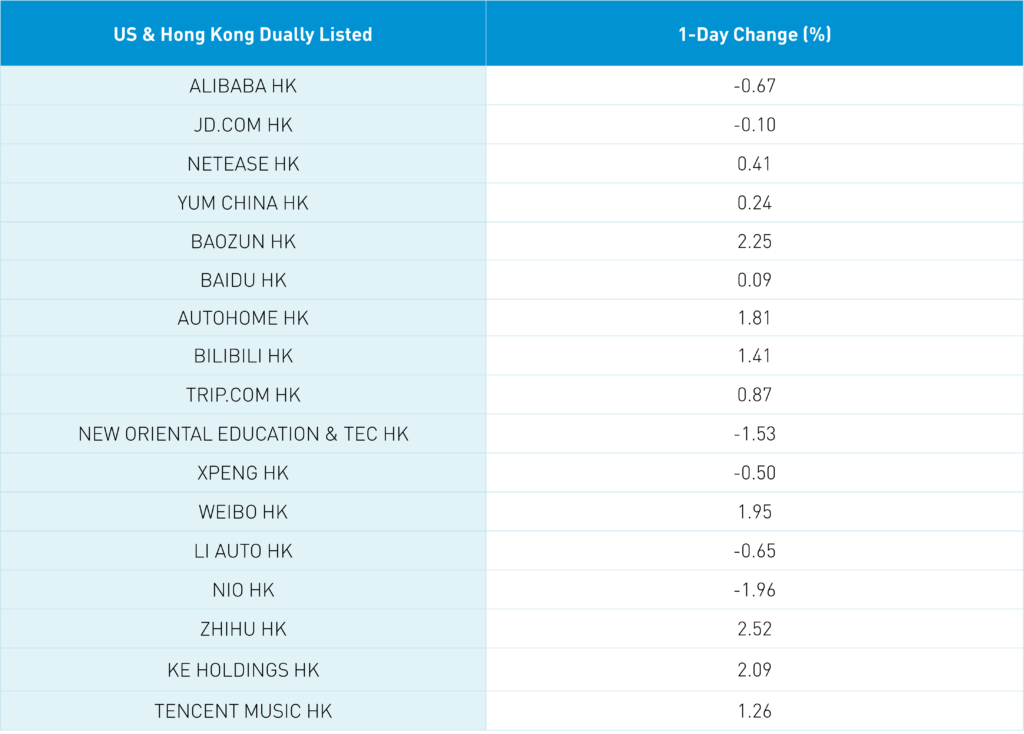

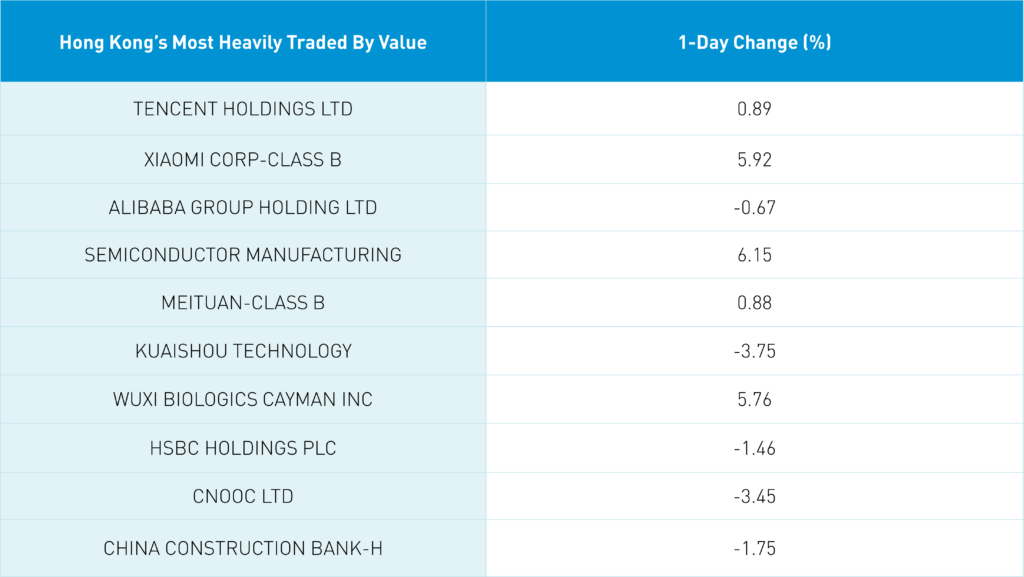

Northbound Stock Connect saw a small/moderate net outflow of $327 million, though on very high volumes, as foreign investors appear to be rotating away from financials. Hong Kong’s most heavily traded stocks were Tencent, which gained +0.89%, Xiaomi, which gained +5.92%, Alibaba, which fell -0.67%, despite a Singles Day ramp-up with 1 million merchants and brands participating, Semiconductor Manufacturing (SMIC) gained +6.15%, and Meituan gained +0.88%. Real estate was off as Evergrande’s Hong Kong court case made headlines. Country Garden has not even begun the court process, though Sunac was able to receive a court-approved restructuring. CNY and the Asia Dollar Index were basically flat overnight.

Bloomberg News noted that “China Internet Majors’ profitability improved” based on a Fitch Ratings release on the bonds from Alibaba (A+/Stable), Baidu (A/Stable), and Tencent (A+/Stable). The Fitch release notes the companies' “stronger business profiles, execution, and continued focus on cost efficiency to drive a fuller recovery in their profitability and cash generation from 2023, despite the uncertainty over China’s economic recovery pace.” Have you ever looked at the internet companies’ bonds versus their stocks? For example, check out Alibaba’s bond, which is due next November. Even during the worst of China’s internet regulation, bond investors did not blow out of the bonds as the companies continued to generate strong cash flows despite the stocks falling. I will post some graphs on Twitter (@ahern_brendan) today. It is an incredible disparity, showing how non-fundamental factors have weighed on the space.

The Hang Seng and Hang Seng Tech indexes gained +0.04% and +1.27%, respectively, on volume that increased +1.09% from Friday, which is 82% of the 1-year average. 294 stocks advanced while 180 declined. Main Board short turnover increased +7.37% from Friday, which is 79% of the 1-year average. The growth factor outperformed the value factor while small caps outpaced large caps. The top-performing sectors were healthcare, which gained +4.68%, technology, which gained +4.56%, and materials, which gained +2.61%. Meanwhile, energy fell -2.29%, financials fell -1.73%, and utilities fell -1.68%. The top-performing subsectors were pharmaceuticals, technical hardware, and semiconductors. Meanwhile, energy, banks, and telecom services were among the worst-performing. Southbound Stock Connect volumes were high as Mainland investors bought $287 million worth of Hong Kong-listed stocks and ETFs as Innovent was a small net buy, SMIC and Xiaomi were moderate net buys, and Kuaishou was a moderate net sell.

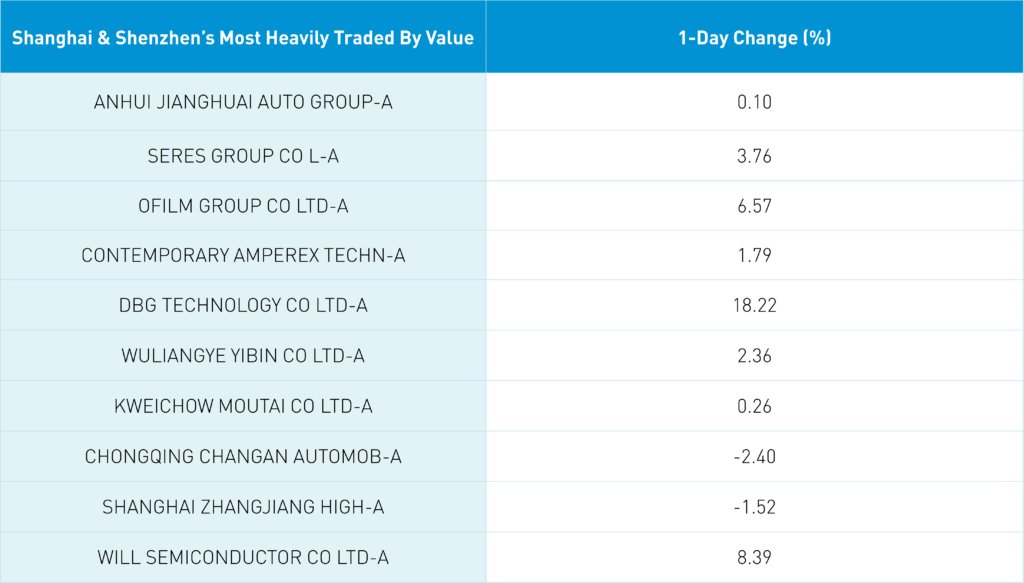

Shanghai, Shenzhen, and the STAR Board gained +0.12%, +1.4%, and +1.89%, respectively, on volume that increased +7.72% from Friday, which is 119% of the 1-year average. 3,515 stocks advanced while 787 declined. The growth factor outperformed the value factor while small caps outpaced large caps. The top-performing sectors were technology, which gained +2.27%, healthcare, which gained +2.38%, and materials, which gained +1.18%. Meanwhile, energy fell -1.92%, real estate fell -1.47%, and financials fell -1.16%. The top-performing subsectors were semiconductors, electronic components, and computer hardware. Meanwhile, oil/gas, highway and banking were the worst. Northbound Stock Connect volumes were very high as foreign investors sold a net -$327 million worth of Mainland stocks as Will Semiconductor, JAC, and Maxscend were large net buys while CMB, Citic, and LXJM were moderate sells. CNY and the Asia Dollar Index were basically flat versus the US dollar. Bonds sold off small while copper and steel rallied.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.32 versus 7.32 Friday

- CNY per EUR 7.75 versus 7.73 Friday

- Yield on 1-Day Government Bond 1.60% versus 1.55% Friday

- Yield on 10-Year Government Bond 2.71% versus 2.71% Friday

- Yield on 10-Year China Development Bank Bond 2.75% versus 2.75% Friday

- Copper Price +0.99% overnight

- Steel Price +0.84% overnight