IMF Raises China’s GDP Forecast As Mainland Investors Buy The Hong Kong Dip In Size

4 Min. Read Time

Key News

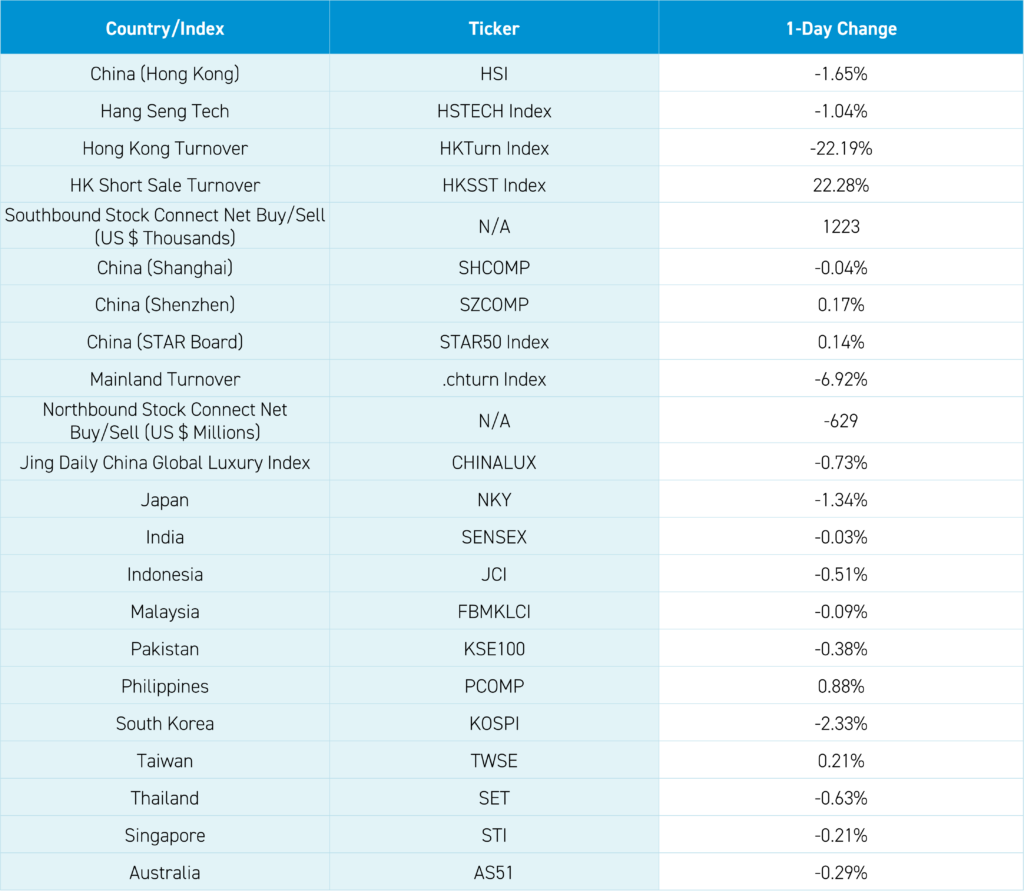

Asian equities were mostly lower as South Korea underperformed after their short sale ban yesterday, while Taiwan and the Philippines managed small gains.

The US Treasury Yield inched higher yesterday, leading to a stronger US dollar as celebrity central bankers joust for TV time. Hong Kong was hit with a bout of profit taking on moderate volume while the Mainland market was mixed on high volume. Mainland investors bought a very healthy $1.223 billion of Hong Kong ETFs and stocks with a very large net inflow into the Hong Kong Tracker ETF, with two other Hong Kong ETFs seeing small net inflows. No announcements from sovereign wealth fund Central Huijin on ETF purchases, though they have been focused on Mainland China versus Hong Kong.

October trade data was mixed, with exports -6.4%, missing expectations of -3.5% and September’s -6.2%, while imports -3% beat expectations of -5% and September’s -6.2%. Remember, exports are more reflective of the global economy than China’s economy. The International Monetary Fund noticed the recent policy support and economic bottoming (fingers crossed) and raised their 2023 GDP forecast to 5.4% from 5% and the 2024 GDP forecast to 4.6% from 4.2%. The GDP forecast occurred at the conclusion of a China trip by the IMF, which acknowledges “continuing weakness in the property market and subdued external demand” weighing on the economy. Real estate stocks had a rough day in Hong Kong despite Vanke’s meeting with creditors yesterday, followed by the Shenzhen provincial government echoing support.

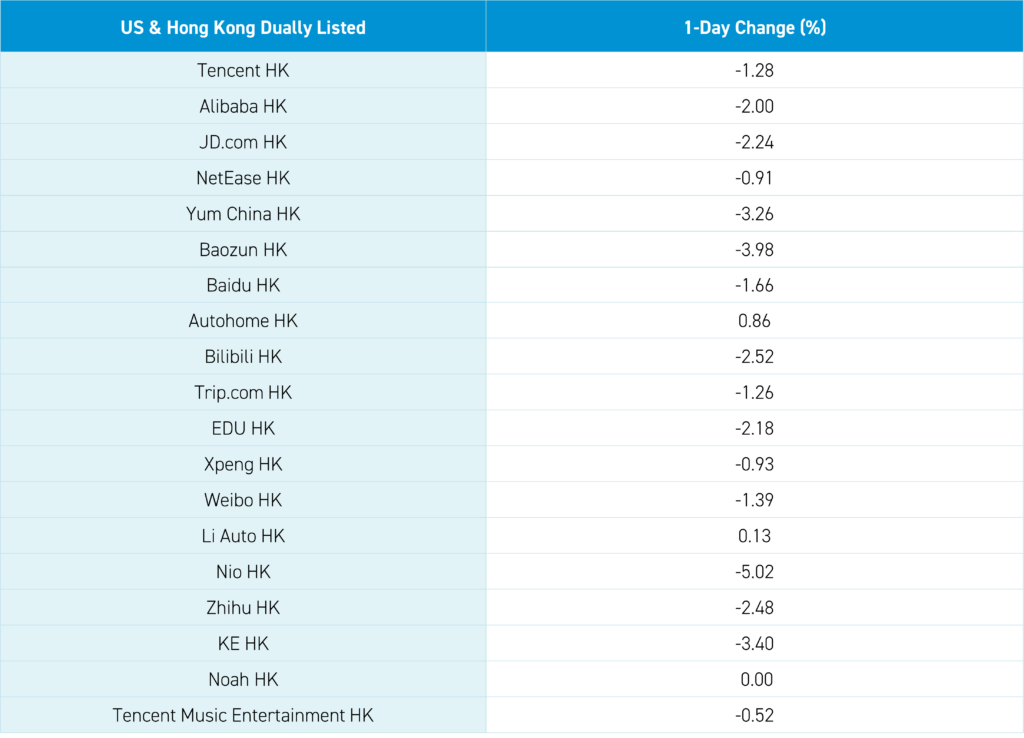

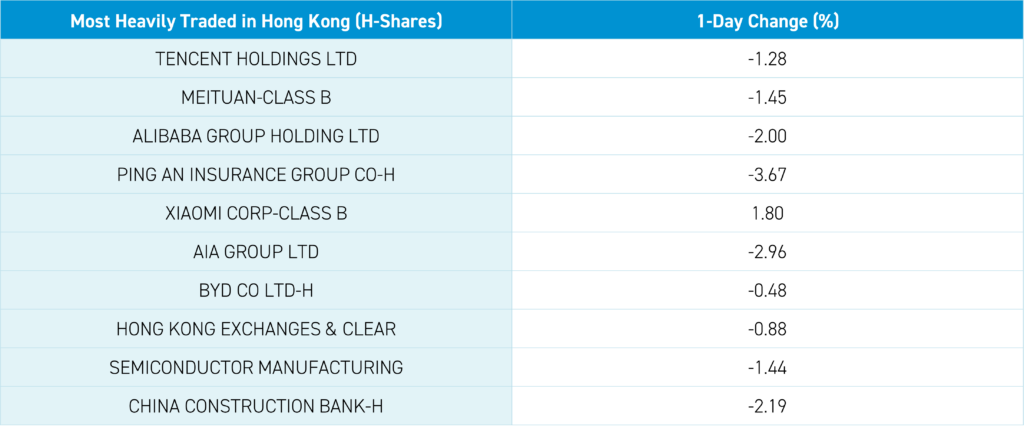

After the close, the PBOC announced it would support private/non-SOE developers by supporting/promoting the issuance of new bonds through an effort called the “second arrow”. Hong Kong breadth was awful as we endured another “foreign freakout” with 4 to 1 losers to winners as Hong Kong’s most heavily traded by value were Tencent -1.28%, Meituan -1.45%, and Alibaba -2%, in line with yesterday’s fall in their ADRs.

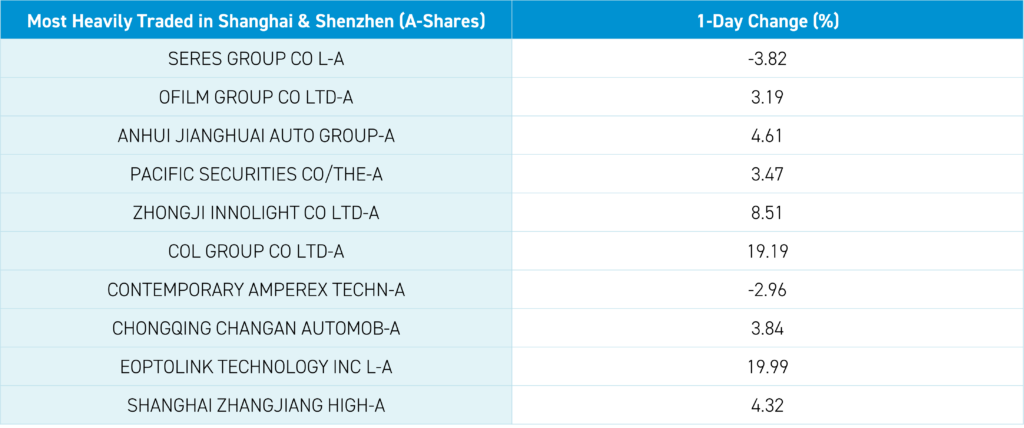

Mainland held up better than Hong Kong, with the Shenzhen and STAR Board posting small gains despite foreign investors selling -$629 million of Mainland stocks today via Southbound Stock Connect. The Mainland’s heavily traded stock by value was automaker Seres Group (601127 CH) -3.82% after rising from RMB 30 in late August to today’s close of RMB 94 after announcing an EV partnership with Huawei. Treasury Secretary Yellen and Vice Premier He Lifeng will meet in SF prior to the APEC summit next week. Australia Prime Minister Albanese wraps up his China trip and President Xi meeting. Hong Kong is hosting the Global Financial Leaders’ Investment Summit, with executives from global banks attending. Sensing a trend? Me too.

Can you imagine what a short sale ban would do for the Hong Kong market? Ironically, a move like that could lead to MSCI downgrading Hong Kong from developed market indices to emerging markets indices. There are technical reasons for Hong Kong and China not to be in the same index or to be combined, though it doesn’t make a lot of sense to me.

The 2023 League of Legends (LoL) World Championship has been taking place in South Korea since early October, with the finals taking place on Sunday, November 19th, at the Gocheok Sky Dome in Seoul. The Gocheok Sky Dome is the largest arena in South Korea, with a capacity of 16,744, and home to Seoul’s Kiwoom Heroes. LoL is an exceedingly popular video game in Mainland China and Asia, though the competition draws teams from Europe, and North/South America as well. The month-long competition’s motto is aptly called “The Grind. The Glory.” There is some chatter that sports apparel maker Li Ning (2331 HK) -4.56% was down after the LoL team it sponsored was eliminated from the competition. Apparently, fans took to social media, blaming the sponsor. As a New York sports fan, I understand their frustration.

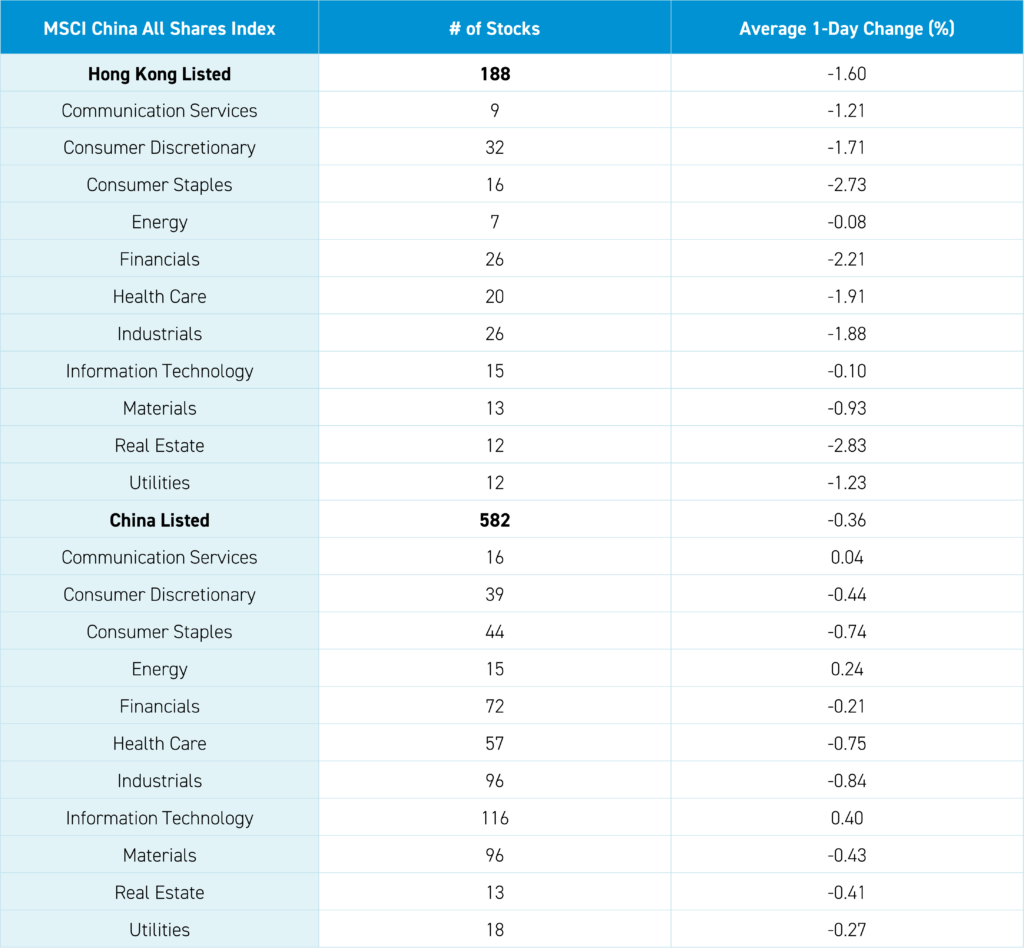

The Hang Seng and Hang Seng Tech fell -1.65% and -1.04% on volume -22.19% from yesterday, which is 80% of the 1-year average. 90 stocks advanced, while 402 declined. Main Board short turnover increased 22.28% from yesterday, which is 103% of the 1-year average, as 21% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Value and growth factors were both off, while large caps “outperformed”/fell less than small caps. All sectors were negative, with energy and tech off the least at -0.08% and -0.1%, while real estate -2.83%, staples -2.73%, and financials -2.21%. The top sub-sectors were food/staples retail, energy, and tech hardware, while insurance, real estate, and food were the worst. Southbound Stock Connect volumes were moderate as Mainland investors bought $1.223 billion of Mainland stocks and ETFs, with the Hong Kong Tracker ETF seeing a large net inflow and H-Shares and Hang Seng Tech ETFs seeing moderate net buying.

Shanghai, Shenzhen, and STAR Board were mixed -0.04%, +0.17%, and +0.14% on volume -692% from yesterday, which is 113% of the 1-year average. 2,667 stocks advanced, while 2,022 declined. Value and growth factors were both off, while small caps outpaced large caps. The top sectors were tech +0.4%, energy +0.24%, and communication +0.04%, while industrials -0.84%, healthcare -0.75% and staples -0.74%. The top sub-sectors were computer hardware, communication equipment, and education, while insurance, office supplies, and motorcycles were the worst. Northbound Stock Connect volumes were off as foreign investors sold -$629 million of Mainland stocks with stockbroker East Money, Willsemi, and BYD small/moderate net buys while CATL was a large net sell, Innolight and Eoptolink moderate net sells. CNY and the Asia dollar index fell versus the US dollar. Treasury bonds were sold while copper gained and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.28 versus 7.27 yesterday

- CNY per EUR 7.78 versus 7.81 yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.73% versus 2.72% yesterday

- Copper Price +0.24% overnight

- Steel Price -0.31% overnight