Real Estate Rises, Did The CSRC Front Run The PCAOB On Audit Reviews?

3 Min. Read Time

Key News

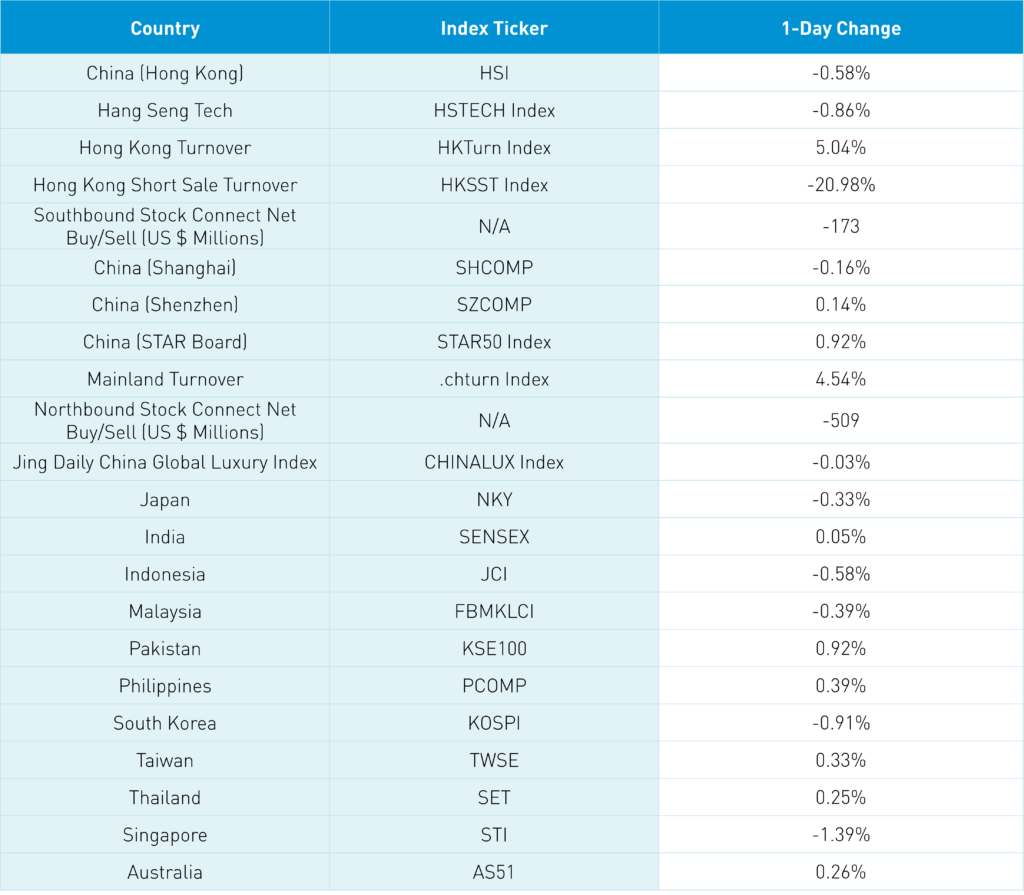

Asian equities were mixed overnight on light news.

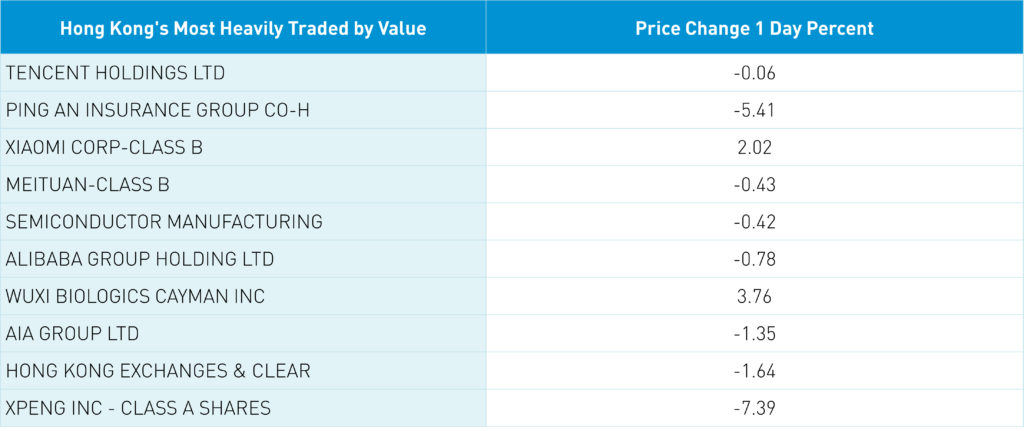

Hong Kong and Mainland China eased off morning gains in the afternoon. Real estate was a top-performing sector in both Hong Kong and Mainland China after several financial regulators met with real estate developers in order to support the sector following last week’s Central Financial Work Conference (CFWC). Rumors that Ping An (2315 HK) would take a stake in distressed developer Country Garden (locally known as Cogard) sent the insurance company's shares lower by -5.41% in Hong Kong despite denying the rumor.

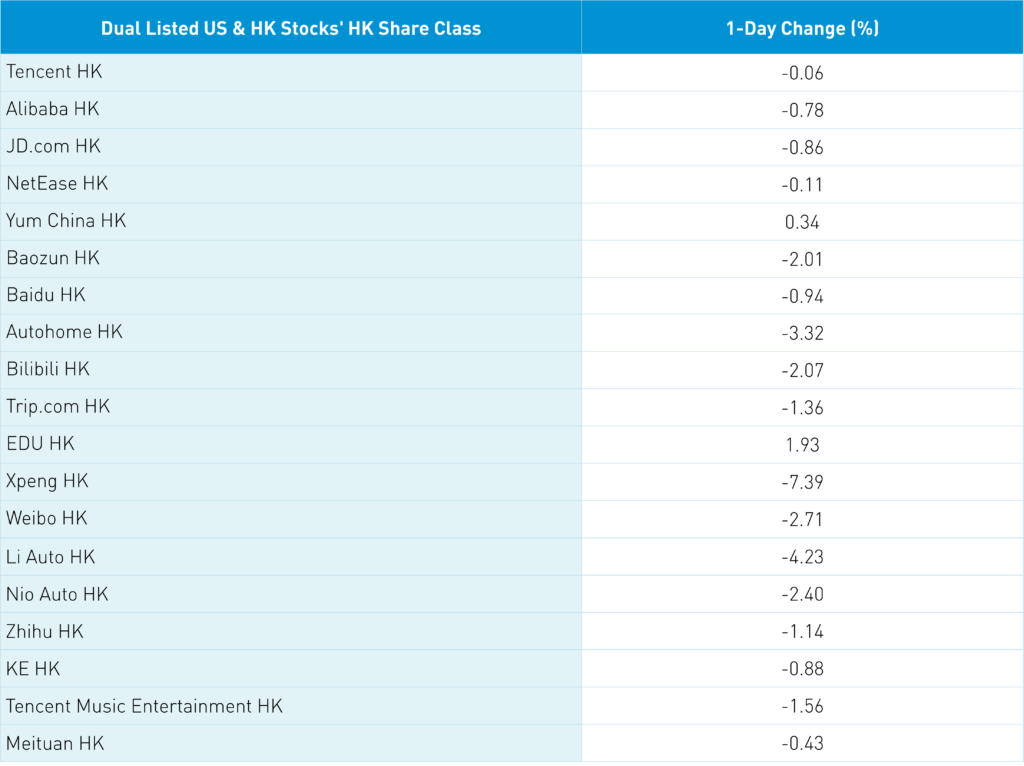

It is worth noting that Mainland China’s volumes were 118% of the 1-year average overnight, with the growth stock/sector-focused Shanghai and STAR Board closing in the green versus the value stock/sector focused Shanghai posting a small decline. The Shenzhen Composite has cleared our “line in the sand” level of 1,900, though the Shanghai Composite sits just below the 3,100 level. Mainland China’s outperformance occurred despite foreign investors selling $509 million worth of Mainland stocks via Northbound Stock Connect. Hong Kong was off, though healthcare had another strong day while internet names were mixed despite Singles Day occurring on Saturday and Q3 financial results to be released next week from heavyweights Meituan on Tuesday, Tencent and JD.com on Wednesday, and Alibaba on Thursday. I anticipate early mornings next week as I’ll be on the West Coast for APEC.

Q3 expectations are low, though we anticipate further buybacks will be announced and maybe a dividend from a major E-Commerce company. There were several below-the-radar positives that were not widely reported. President Xi gave the opening speech at the 2023 World Internet Conference Wuhan Summit. This is another strong signal that the Internet regulatory cycle is over. Alibaba’s CEO gave a speech as well. China’s Foreign Ministry confirmed a Biden-Xi meeting next week at APEC. Meanwhile, Vice President Han spoke about the importance of US-China relations at the Innovation Economic Forum in Singapore. The PBOC head spoke about the importance of monetary tools and policy to support the economy at the Financial Street Forum.

The CSRC is China’s financial regulator, similar to the SEC. Their head of International Cooperation Department gave a speech yesterday including comments on “China-US audit and regulatory cooperation” which were progressing “smoothly”. Professional investors cannot hold a stock that faces delisting risk. The SEC maintains a website with US-listed China ADRs due to the Holding Foreign Companies Accountable Act (HFCAA). The Public Company Accounting Oversight Board (PCAOB) visited Hong Kong last September after China changed its law in August allowing PCAOB auditor inspections. In December 2022, the PCAOB reported the first round of audit reviews went well without any hindrance. Yes, there were deficiencies, as expected. Thus far, the PCAOB has not opined on the results of their second Hong Kong auditor review. I doubt the Big Four US accounting firms are not doing their job on US-listed China stocks, though I would anticipate deficiencies and fines to be levied. A green light from the PCAOB should lead to the SEC removing the ADRs from their website. Maybe the CSRC is telling us something? Maybe not! We shall see!

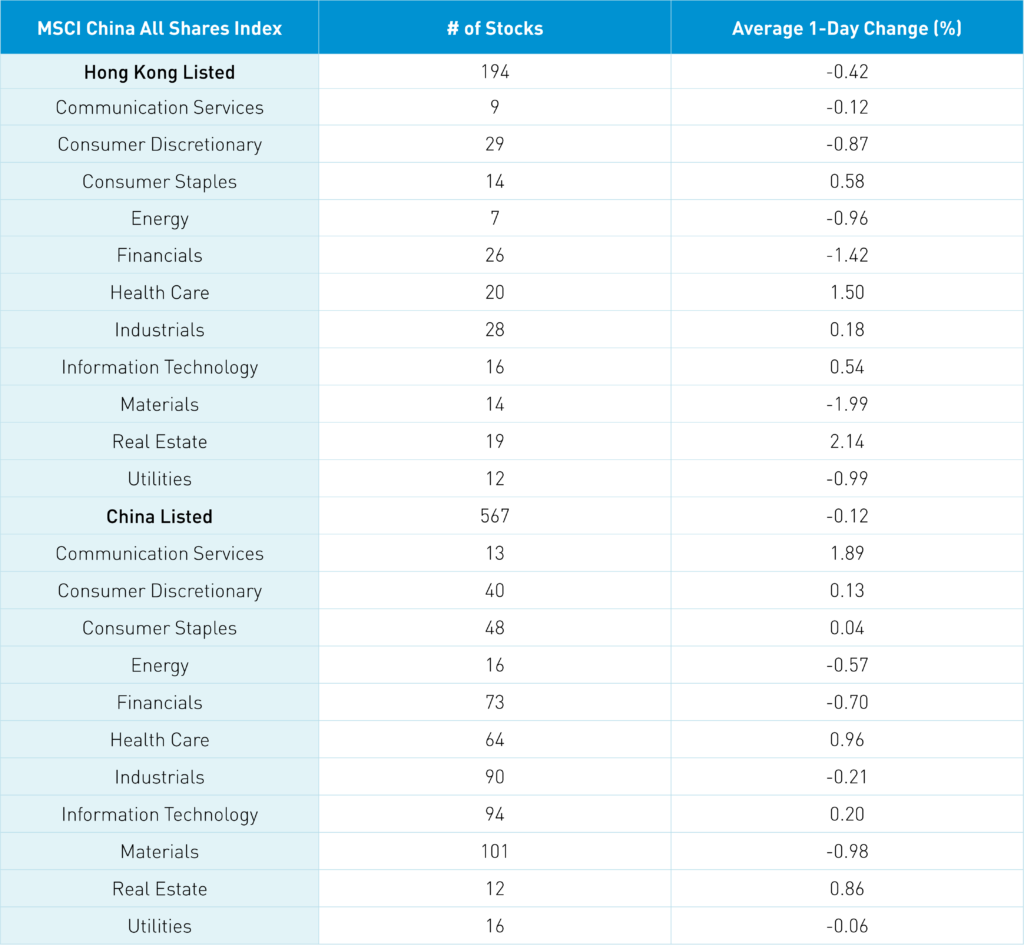

The Hang Seng and Hang Seng Tech indexes fell -0.58% and -0.86%, respectively, on volume that increased +5.04% from yesterday, which is 85% of the 1-year average. 176 stocks advanced, while 305 declined. Main Board short turnover declined -20.98% from yesterday, which is 81% of the 1-year average, as 16% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor outperformed the value factor as small caps “outperformed” (i.e. fell less than) large caps. The top-performing sectors were real estate, which gained +2.14%, healthcare, which gained +1.5%, and consumer staples, which gained +0.59%. Meanwhile, the worst-performing sectors were materials, which fell -1.99%, financials, which fell -1.42%, and utilities, which fell -0.98%. The top-performing subsectors were real estate, business services, and food and beverage. Meanwhile, insurance, autos, and materials were the among the worst-performing. Southbound Stock Connect volumes were high as Mainland investors sold -$173 million of Hong Kong stocks and ETFs, with SMIC a moderate/light buy, Xiaomi and Wuxi Biologics small net buys, while the Hong Kong Tracker ETF a large net sell, Hang Seng Tech ETF a moderate net sell, CNOOC and Tencent small net sells.

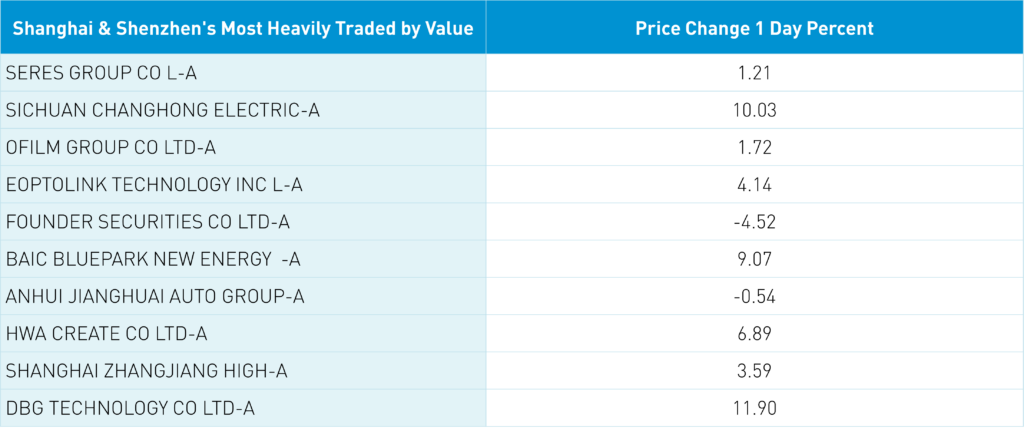

Shanghai, Shenzhen, and STAR Board diverged to close -0.16%, +0.14%, and +0.92%, respectively, on volume that increased +4.54% from yesterday, which is 118% of the 1-year average. 2,114 stocks advanced, while 2,682 declined. The growth factor outperformed the value factor, while small caps outpaced large caps. The top-performing sectors were communication services, which gained +1.99%, healthcare, which gained +0.97%, and real estate, which gained +0.87%. Meanwhile, materials fell -0.97%, financials fell -0.69%, and energy fell -0.56%. The top-performing subsectors were cultural media, internet, and software. Meanwhile, insurance, precious metals, and diversified financials were the worst-performing. Northbound Stock Connect stock volumes were moderate as foreign investors sold a net -$509 million worth of Mainland stocks, with Luzhou Lao Jiao, Kweichow Moutai, and East Money small net buys, while Eoptolink, Founder Securities, and O-Film were small net sells. CNY and Asia dollar index were basically flat versus the US dollar. Treasury bonds rallied while copper fell and steel rose.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.28 versus 7.28 yesterday

- CNY per EUR 7.77 versus 7.78 yesterday

- Yield on 10-Year Government Bond 2.64% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.72% versus 2.73% yesterday

- Copper Price -0.41% overnight

- Steel Price +0.03% overnight