Alibaba Beats But Cloud IPO Pulled

4 Min. Read Time

Key News

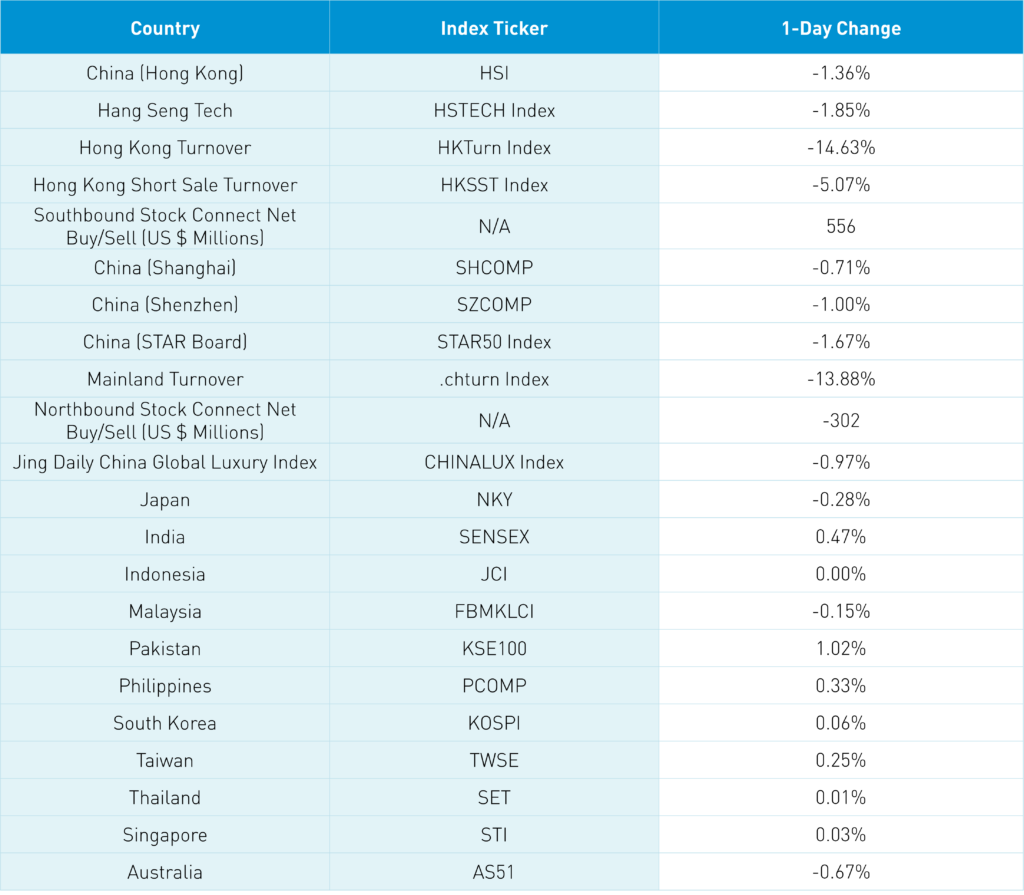

Asian equities were mixed overnight, with Japan, Mainland China, and Hong Kong off while Taiwan, Korea, and India managed small gains.

The Biden-Xi four-hour meeting met low expectations though strong progress was made on curbing fentanyl ingredient exports, furthering communication between the two militaries, and agreeing to talks on artificial intelligence risks. The sleeper positive was Biden’s comments on Taiwan and maintaining the one-China policy. We shouldn’t expect the two sides to go to the prom together, though they are learning how to play nice in the sandbox with one another.

There was significant attention surrounding Biden’s dictator comment, though I question what was worse: a CNN reporter felt that was a legitimate question or Biden falling for it. President Xi’s speech to US business executives, including Tim Cook, Elon Musk, and Jonathan Krane, was very positive on US-China relations and history though it was also a very personal speech about his time in San Francisco and Iowa. If you have time, I recommend reading the speech as it reads to me as a strong commitment to maintaining strong diplomatic and business relations with the US. (https://finance.sina.com.cn/stock/y/2023-11-16/doc-imzuuvxt7943934.shtml).

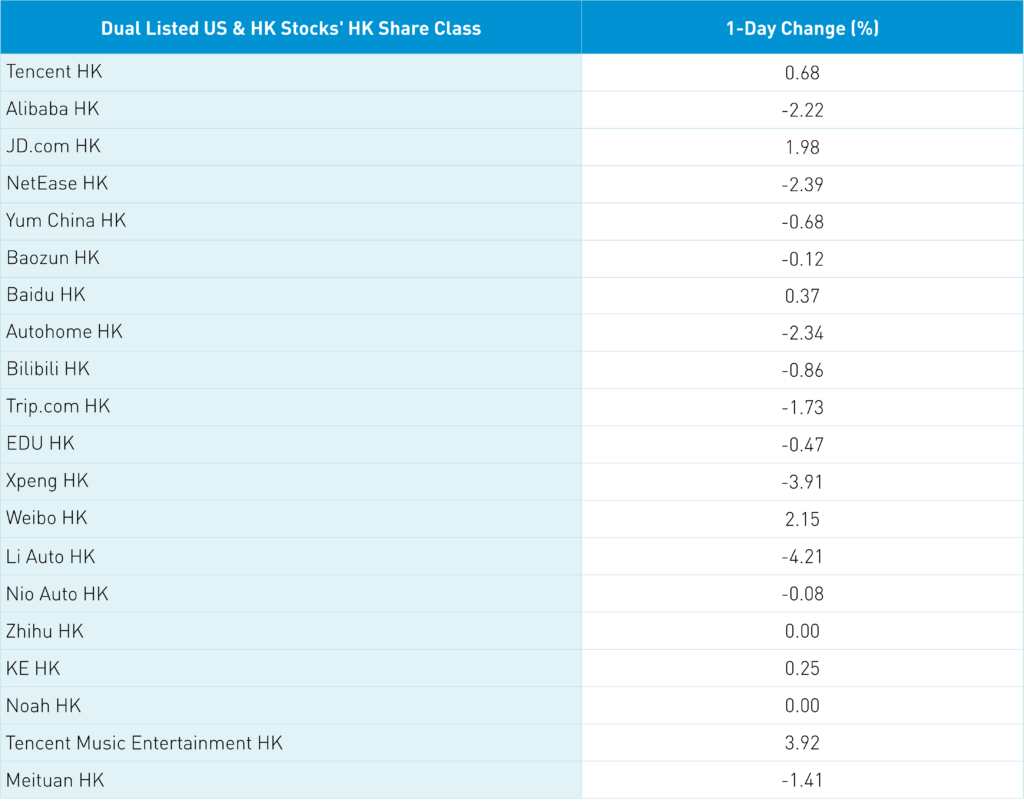

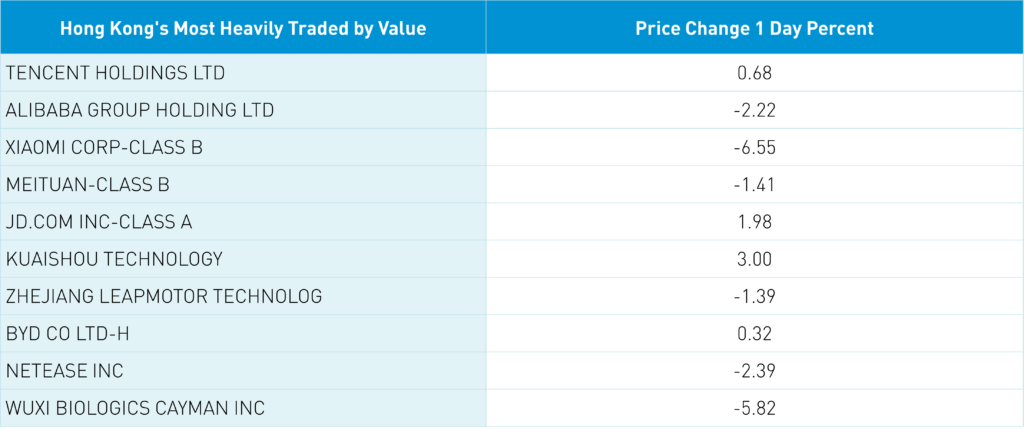

Hong Kong was hit with profit-taking, led lower by growth stocks/sectors as neither the Biden-Xi summit nor strong/better-than-expected results from Tencent and JD.com inspired buyers. Hong Kong’s most heavily traded by value were Tencent +0.68%, Alibaba HK -2.22%, Xiaomi -6.55%, Meituan -1.41%, and JD.com HK +1.98%.

This morning, Alibaba beat analyst expectations with revenue up +9% year over year (YoY) to RMB 224.79B ($30.81B) versus expectations of RMB 224.09B, adjusted net income increased by +16% to RMB 140.188B ($5.508B) versus expectations of RMB 140.042B, and adjusted EPS was up +21% to RMB 1.95 ($0.27). The core China e-commerce revenue grew by 4% YoY to RMB 97.654B, though international grew +53% to RMB 24.511B. Cloud revenue was up only +2% to RMB 27.648, though the company’s decision to halt the cloud business due to US semiconductor restrictions has garnered significant attention. Ultimately, the environment for extracting shareholder value via Hong Kong IPOs and spin-offs is not today.

Tencent had mentioned hoarding US chips in advance of the US export controls. Remember, Alibaba has made several management changes, with the new team potentially disagreeing with the previous spin-off plan. The stock’s negative reaction to positive results is a head-scratcher. However, the change of heart on the cloud spin-off may have left some confused. The company is paying a dividend for the first time of $1 per share from its $85 billion of cash. The company used $1.62 billion of cash to buy back stock in the quarter. At $79, the company is nearly trading at 50% cash ($200 billion market cap versus $85 billion of cash) and a forward P/E below 9!

NetEase (NTES US) beat on the big three: revenue, adjusted net income, and adjusted EPS this morning/post-Hong Kong close. Mainland investors bought the Hong Kong dip via Southbound Stock Connect with large buys in the Hong Kong ETF Tracker and Hang Seng Tech ETFs. The Mainland market has been grinding higher, so a break is not unexpected. Fairly quiet in China overnight, though the Biden-Xi meeting was portrayed in a positive light by Mainland media. Foreign investors returned to sellers of Mainland stocks to the tune of -$302 million via Northbound Stock Connect.

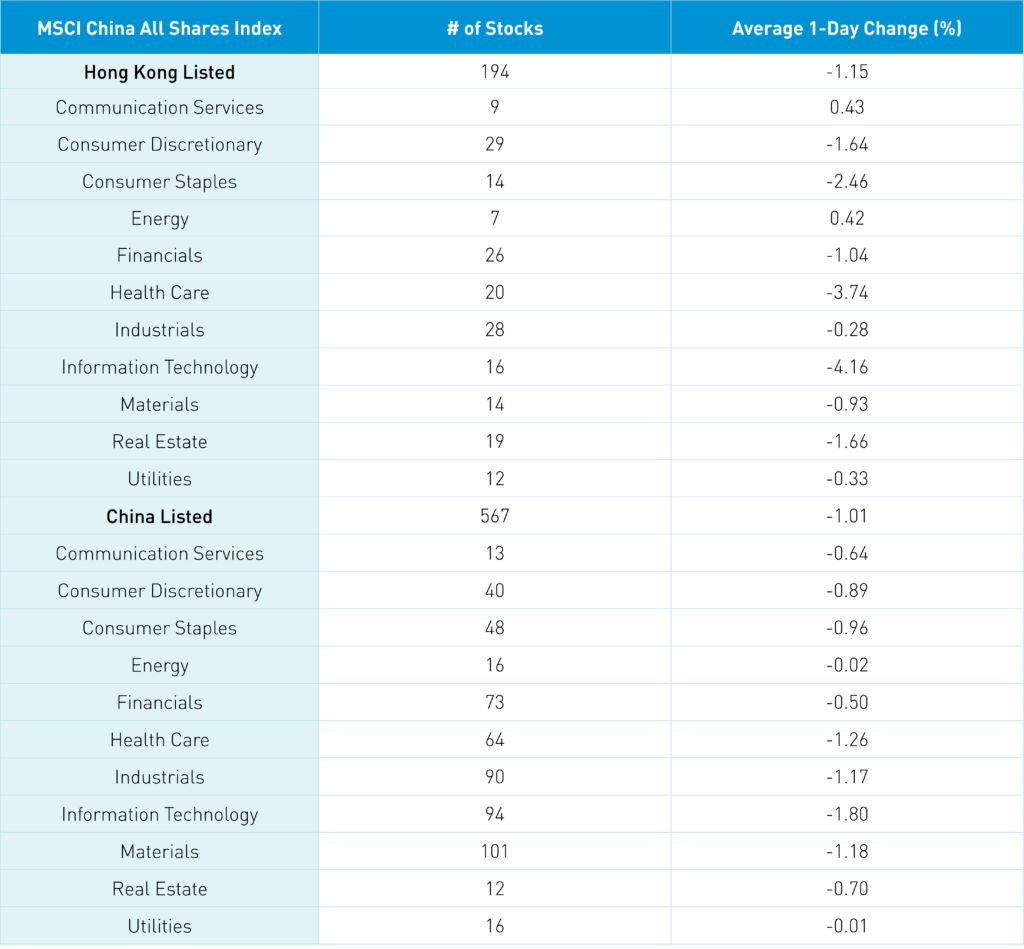

The Hang Seng and Hang Seng Tech indexes fell -1.36% and -1.85%, respectively, on volume that declined -14.63% from yesterday, which is 105% of the 1-year average. 108 stocks advanced, while 370 declined. Main Board short turnover declined -5% from yesterday, which is 128% of the 1-year average, as 29% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and large caps “outperformed”/fell less than the growth factor and small caps. Communication and energy were the only positive sectors, gaining +0.43% and +0.42%, while tech fell -4.16%, healthcare was down -3.74%, and staples closed lower -2.46%. The top sub-sectors were food/staples, media, and software, while technical hardware, pharmaceuticals, and semiconductors were the worst. Southbound Stock Connect volumes were high as Mainland investors bought +$556 million of Hong Kong stocks and ETFs, with the Hong Kong Tracker and Hang Seng Tech ETFs seeing moderate/large net buys, while Tencent and Meituan were net sells.

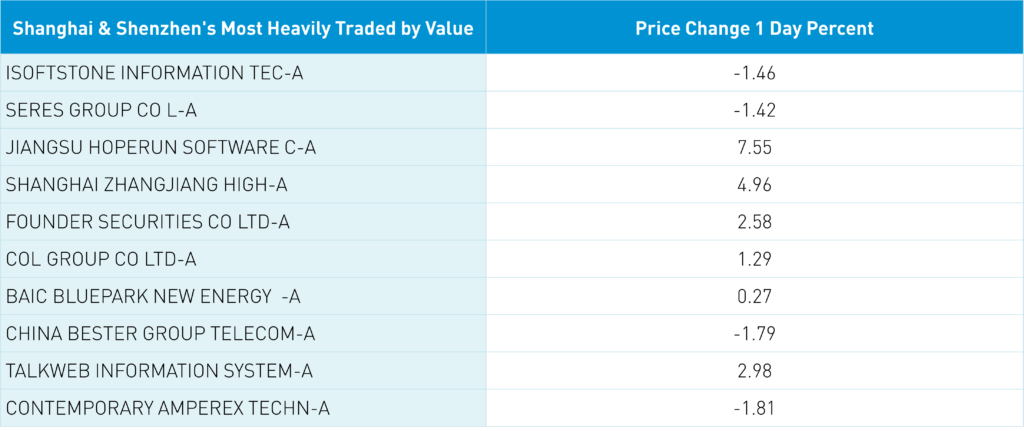

Shanghai, Shenzhen, and the STAR Board were off -0.71%, -1.00%, and -1.67%, respectively, on volume that declined -13.88% from yesterday, which is 97% of the 1-year average. 942 stocks advanced, while 3,885 declined. The value factor and large caps “outperformed”/fell less than the growth factor and small caps. All sectors were negative, with tech -1.82%, healthcare -1.27%, and materials -1.2% off the most. The top sub-sectors were cultural media, office supplies, and coal, while power generation equipment, semis, and chemicals were the worst. Northbound Stock Connect volumes were moderate/light as foreign investors sold -$302 million of Mainland stocks, with LXJM, CATL, and BYD being small net buys, while Longi and Ping An Bank were moderate net sells. CNY and the Asia dollar index gained versus the US dollar. The Treasury curve flattened while copper and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY per EUR 7.87 versus 7.86 yesterday

- Yield on 10-Year Government Bond 2.65% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.72% versus 2.73% yesterday

- Copper Price +0.25% overnight

- Steel Price +1.50% overnight