National Team Melts Snowballs as Hong Kong Rebounds

4 Min. Read Time

Key News

Asian equities were mixed as Mainland China outperformed and the US dollar was down overnight, following the 10-year Treasury Yield lower.

Mainland China opened lower and appeared headed toward another drawdown with the Shanghai Composite’s intra-day low of -2.56%, Shenzhen’s intra-day low of -2.65%, and the STAR Board's intra-day low of -2.07%, all of which exceeded 52-week lows.

Premier Li’s speech at Davos negated hopes for a policy bazooka as massive stimulus is not necessary. This is true as Mainland China’s economy rebounds incrementally, though real estate clearly needs more policy support after yesterday’s countrywide property declines.

Then, at 2 pm, the cavalry arrived as the "National Team" (i.e. Mainland institutions with links to the government, including the Social Security Fund, pension funds, insurance companies, etc.) arrived with Mainland equity ETFs seeing massive volumes similar to yesterday. The ETFs with volume spikes were the same ones that the sovereign wealth fund Central Huijin purchased last year. It did not take Sherlock Holmes long to figure out who today’s buyer was. Investors took notice, and large and mega-cap growth stocks outperformed as foreign investors pivoted. Northbound Stock Connect flows went from significant outflows to only a net -$100 million.

Mainland China is dealing with an issue similar to Hong Kong’s Callable Bull/Bear Contracts (CBBCs), which are sometimes called Snowballs, though today’s intervention prevented a further forced liquidation drawdown. The People's Bank of China (PBOC), China's central banks, continues to add liquidity to the financial system as we near Chinese New Year and the week-long holiday.

Hong Kong rebounded despite a lack of intervention or acknowledgment of the CBBC issue on decent volumes. This followed yesterday’s rout as the market was led higher by Tencent, which gained +1.09% after buying 3.64 million shares today, raising their buyback total to 169 million (1.76% of shares outstanding). Meituan gained +1.53% after buying back 5.73 million shares as their buyback streak reached its 7th day. Meanwhile, Alibaba and BYD were both up +1.52% and +0.56%, respectively. Baidu gained +3.05% after an analyst upgrade.

Yesterday, we discussed Hong Kong’s CBBCs, which appear to be a contributor to yesterday’s market action and recent weakness as their mandatory liquidation levels are hit in both indices, such as the Hang Seng Index and individual stocks, against the backdrop of the recent buyer’s strike. It is remarkable how little attention this issue has received from the media, in my opinion.

What you will not read about in Western media today: 1) Swiss watchmaker Richemont’s Q4 financial results were higher due to China sales increasing 25% year-over-year versus Europe's sales decreasing -3%, and sales in the Americas increasing +8%. CFO Burhart Grund stated: “Overall, I would say the Chinese business is rebuilding,” according to Reuters.

US Treasury officials in Beijing are visiting their counterparts in another sign of US and Chinese efforts to stabilize their relationship. According to the Financial Times, which is the only media source that I saw that commented on the meeting, “This trip underscores Secretary Yellen and the Biden administration’s commitment to establishing resilient channels of communication between the United States and China,” said a Treasury official.

January 17th, besides being one of my sister’s and Benjamin Franklin’s birthdays, is the day that pizza orders return to averages as New Year's Day resolutions are tossed aside. I was up earlier than usual, working out today. I could not help but notice a news organization‘s Davos coverage was balanced on China comments, but when it switched to the US anchors, it was all doom and gloom. Any notice of today’s Wall Street Journal? There are too many anti-China articles to count! As mentioned, Biden is clearly looking to stabilize the relationship, though neither Congress nor the media seem to care or notice. This seems strange to me!

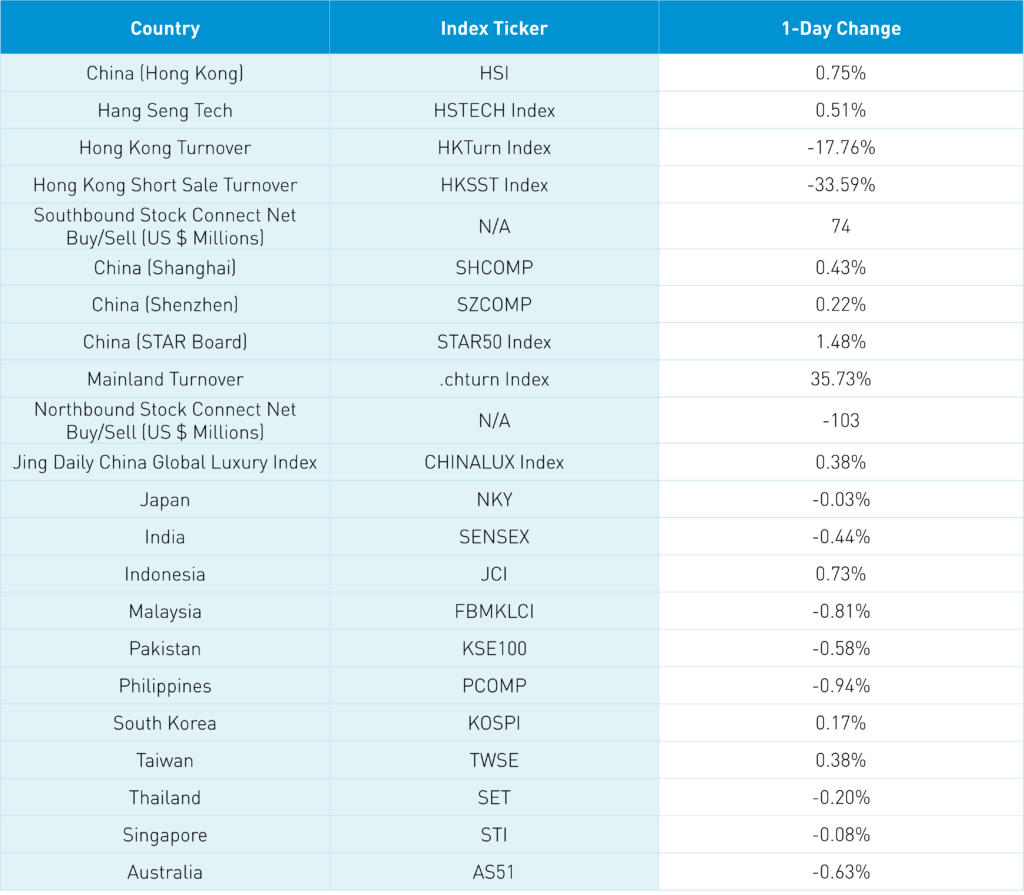

The Hang Seng and Hang Seng Tech indexes gained +0.75% and +0.51%, respectively, on volume that decreased -18% from yesterday, which is 105% of the 1-year average. 325 stocks advanced, while 156 declined. Main Board short turnover declined -33% from yesterday, which is 106% of the 1-year average, as 17% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps outpaced the growth factor and large caps. The top sectors were tech+1.45%, healthcare +1.33%, and communication +1.31%, while energy was the only down sector off -0.36%. The top sub-sectors were semis, pharmaceuticals, and transportation, while healthcare equipment, food/staples, and energy were the worst. Southbound Stock Connect volumes were moderate/light as Mainland investors bought $74 million of Hong Kong stocks and ETFs, with Tencent a small/moderate buy, CITITC Securities and Meituan small net buys, while the Hong Kong Tracker ETF, HS China Enterprise, and SMIC were small net sells.

Shanghai, Shenzhen, and the STAR Board gained +0.43%, +0.22%, and +1.28%, respectively, on volume that increased +35% from yesterday, which is 100% of the 1-year average. 1,404 stocks advanced, while 3,501 declined. The growth factor and large caps outpaced the value factor and small caps. The top sectors were tech +2.81%, staples +1.87%, and communication +1.44%, while energy and utilities were off -0.04% and -0.39%. The top sub-sectors were computer hardware, power generation equipment, and liquor, while water, gas, and the trade industry were the worst. Northbound Stock Connect volumes were high as foreign investors sold -$103 million of Mainland stocks, with Longi Green Energy a very large net buy, Kweichow Moutai a large net buy, and CITS a moderate net buy, while Inovance, Agriculture Bank, and China Merchants Bank were moderate net sells.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.83 versus 7.82 yesterday

- Yield on 10-Year Government Bond 2.50% versus 2.50% yesterday

- Yield on 10-Year China Development Bank Bond 2.64% versus 2.65% yesterday

- Copper Price -0.32%

- Steel Price -0.39%