Alibaba Spin-Off as PBOC Steps Up Real Estate Support

3 Min. Read Time

Key News

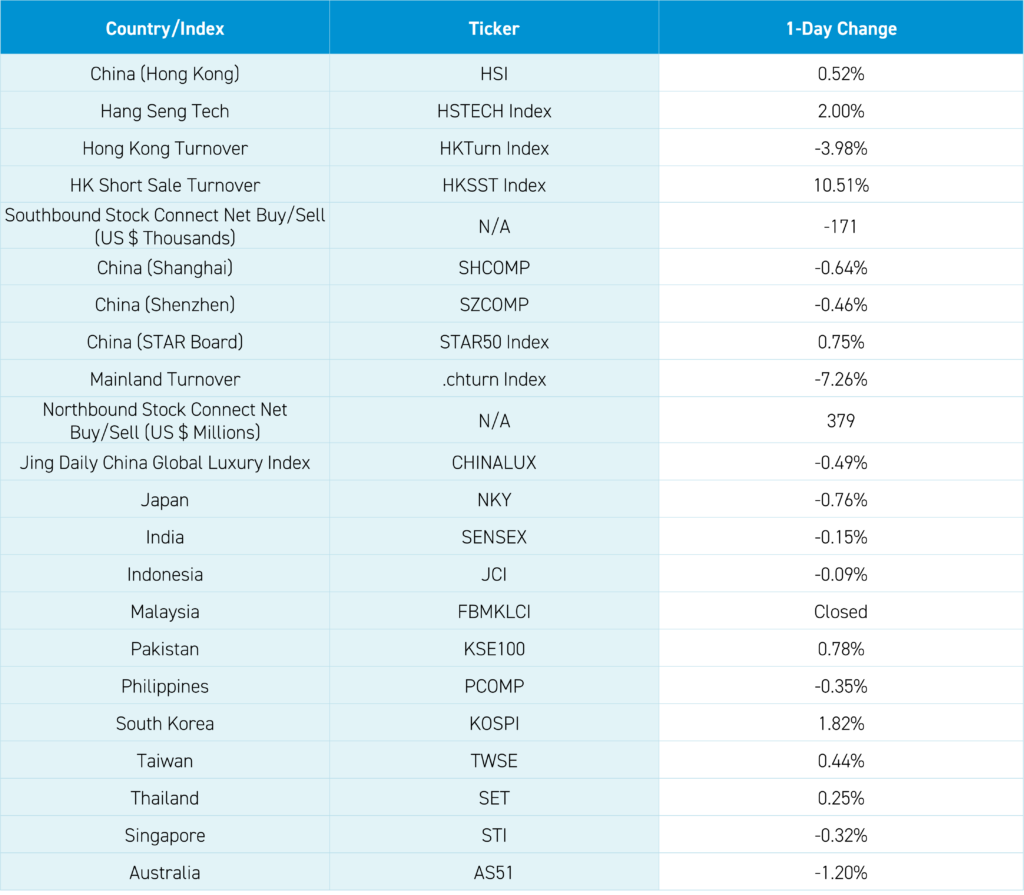

Asian equities were mixed overnight, as Hong Kong posted a gain, South Korea outperformed the region, Japan was off, and Australia underperformed the region.

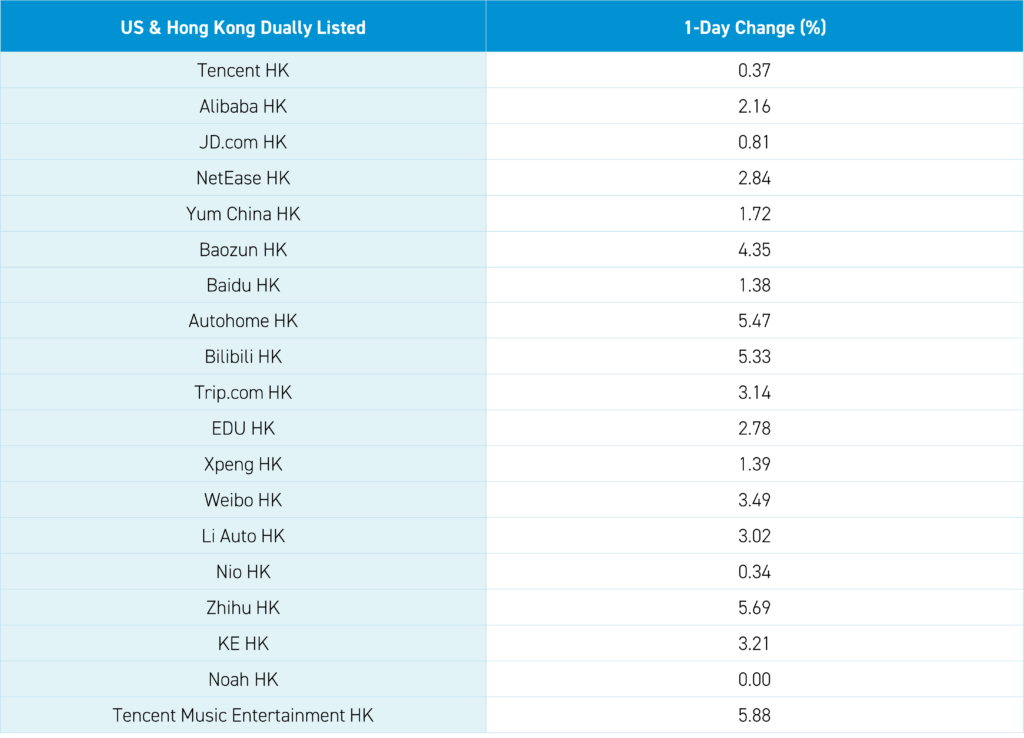

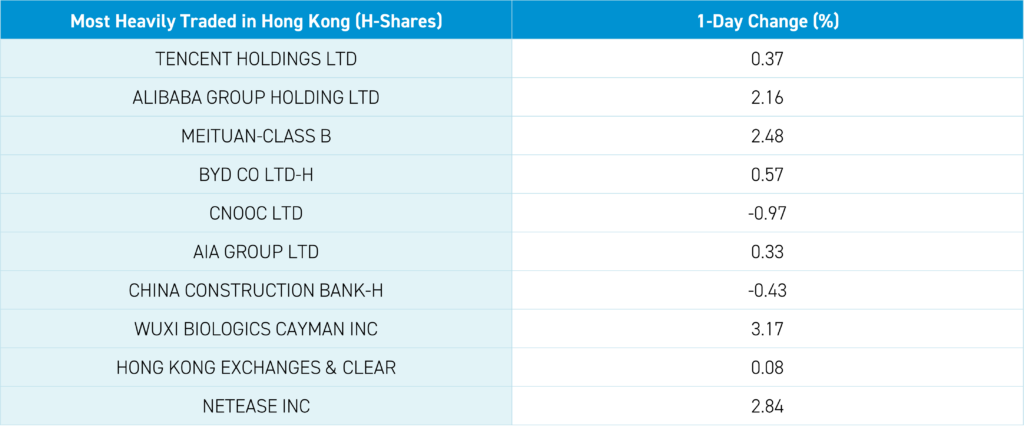

The region took yesterday’s US technology selloff and Powell press conference in stride. While Hong Kong came off its intra-day highs, it was led higher by growth stocks, including Hong Kong’s most heavily traded stocks by value: Tencent, which gained +0.37%, Alibaba, which gained +2.16%, Meituan, which gained +2.48%, BYD, which gained +0.57%, and energy giant CNOOC, which fell -0.97%.

Ministry of Finance Deputy Minister Wang Dongwei held a press conference on China’s “fiscal revenue and expenditure situation” for 2023. The national general public budget revenue (taxes) grew +6.4% year over year (YoY) to RMB 21 trillion, though 2022 was a low-base comparison. He stated, “Fiscal revenue maintains a recovery growth trend. Benefitting from the improvement of economic recovery”. Fiscal expenditures (government spending) increased 5.4% to RMB 274.6T, as the fiscal deficit rate at the beginning of 2023 was 3%. In the Q&A, he spoke to focus on “expanding domestic demand” of local citizens by enhancing “their willingness and ability to consume.” The importance of China’s digital economy was noted along with raising RMB 1T of special bonds for local governments and government spending to support the economy. This was a major headline in China, though Western media didn’t mention it anywhere.

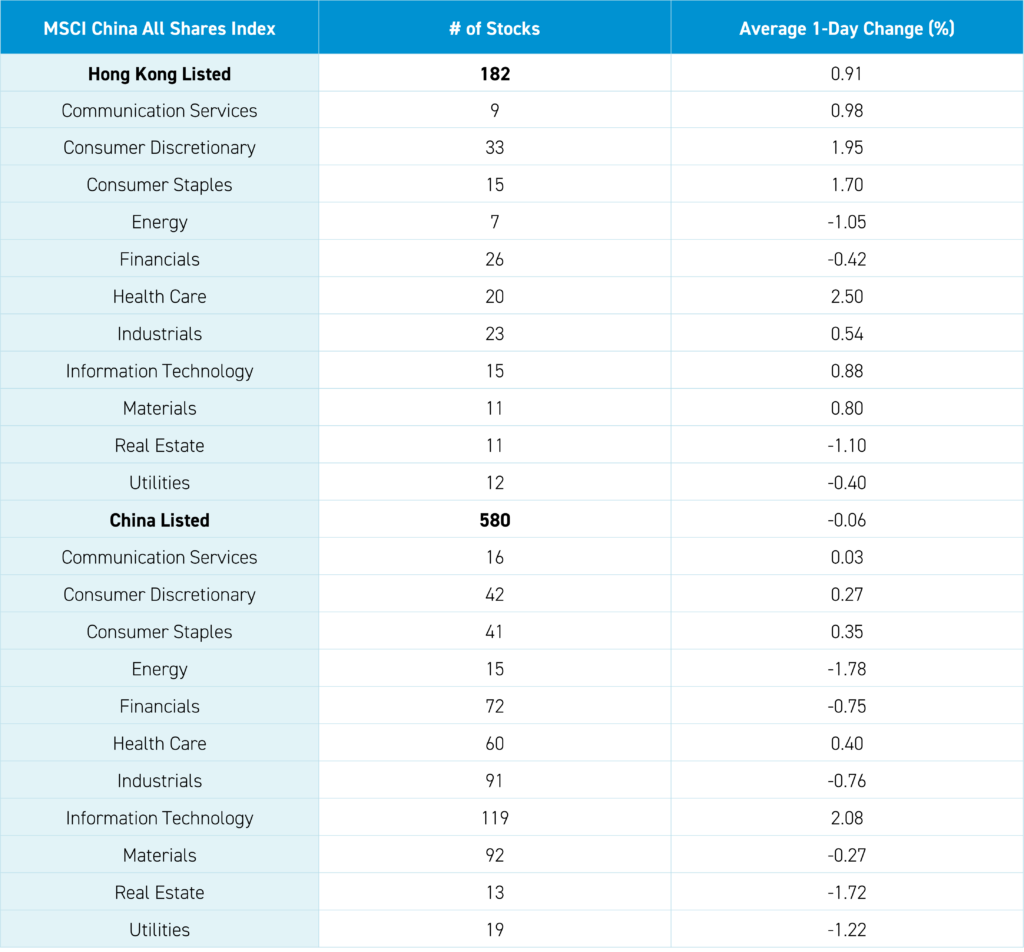

President Xi’s Wednesday Central Committee meeting was noted for its emphasis on the importance of the technology sector, which likely explains the sector's outperformance in Mainland China, where it gained +2.09%, and Hong Kong, where it gained +0.86%.

The January Caixin Manufacturing PMI was flat month-over-month and matched expectations at 50.8. It is not newsworthy if it isn’t bad! As expected, real estate sales data was another disaster, with the sector underperforming in China, where it fell -1.72% and Hong Kong, where it fell -1.11%. However, after the close, the People's Bank of China (PBOC) increased its support for housing in January as its Pledged Supplemental Lending (PSL) increased by RMB 150B ($20B) to RMB 3.4T from December’s RMB 3.2T. Clearly there is more policy support occurring to stabilize the sector. Something to watch!

Healthcare outperformed with Wuxi AppTec rebounding +2.69% on reports the Congress allegations against the company won’t result in a bill, while WuXi XDC +7.2% on preliminary 2023 results indicating profits +80% YoY. As I’ve stated, you need to downplay what Congress says as they want to get on TV so they can build a brand for themselves. Exhibit A was the ridiculous and embarrassing social media CEO Congress meeting yesterday. Many investors take what Congress says as guaranteed to become law, which is untrue.

Alibaba could spin off its In Time department store unit. It was not a bad start to February as we say goodbye to January.

Yesterday, I mentioned South Korea’s rough start to the year; Taiwan is off small year to date, India is flat and Japan is up a little. Yesterday, I noticed several prominent stocks from South Korea, Taiwan, and Japan were downgraded. The downgrades came from analysts from different firms, though all cited valuations. While US analysts’ US tech price targets remain between the moon and Milky Way, and Asian analysts appear slightly more cautious—just observation.

The Hang Seng and Hang Seng Tech indexes gained +0.52% and +2.00%, respectively, on volume that declined -3.98% from yesterday, which is 94% of the 1-year average. 287 stocks advanced, while 192 declined. Main Board short turnover increased +10.51% from yesterday, which is 107% of the 1-year average as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Health Care, which gained +2.51%, Consumer Discretionary, which gained +1.95%, and Consumer Staples, which gained +1.70%. Meanwhile, Real Estate fell -1.1%, Energy fell -1.05%, and Financials fell -0.41%. The top-performing subsectors were media, consumer services, and semiconductors. Meanwhile, telecom services, energy, and banks were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors sold a net -$171 million worth of Hong Kong-listed stocks and ETFs with China Shenhua, CNOOC, and Kuaishou small net buys, while Tencent was a moderate/small net sell, Meituan and China Mobile small net sells.

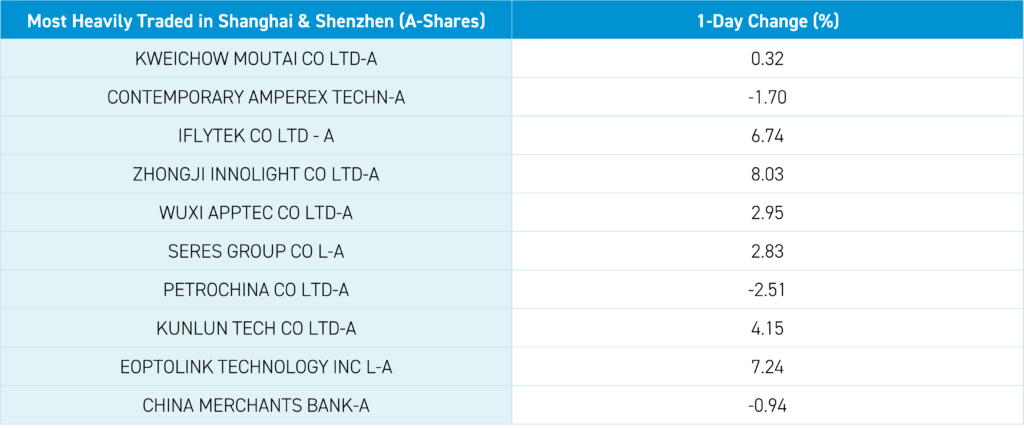

Shanghai, Shenzhen, and the STAR Board diverged to close -0.64%, -0.46%, and +0.75%, respectively, on volume that decreased -7.26% from yesterday, which is 84% of the 1-year average. 1,078 stocks advanced, while 3,874 declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Technology, which gained +2.1%, Health Care, which gained +0.41%, and Consumer Staples, which gained +0.36%. Meanwhile, Energy fell -1.77%, Real Estate fell -1.71%, and Utilities fell -1.2%. The top-performing subsectors were computer hardware, communication, and electronic components. Meanwhile, education, diversified financials, and forestry were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors bought a net $379 million worth of Mainland stocks, including iFlytek, Petrochina, and TFC, which were small/moderate net buys, while Mingyang Smart Energy, Pientze Huang, and Foxconn were small/moderate net sells. CNY and the Asia dollar index were off small compared to the US dollar. Treasury bonds were off small, copper gained, and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.18 versus 7.17 yesterday

- CNY per EUR 7.75 versus 7.77 yesterday

- Yield on 10-Year Government Bond 2.43% versus 2.43% yesterday

- Yield on 10-Year China Development Bank Bond 2.60% versus 2.59% yesterday

- Copper Price +0.23% overnight

- Steel Price -0.62% overnight