Mainland China Has One Of Its Best Trading Days EVER

4 Min. Read Time

Key News

Asian equities were mixed as Mainland China outperformed the region.

Mainland China had one of its best trading days EVER, as 4,934 stocks advanced and only 92 declined! That represents a 50-to-1 advancer-to-decliner ratio. The top 100 most heavily traded stocks by value included only 4 that were lower. Northbound Stock Connect had very high volumes as investors poured a net $2.3 billion into Mainland stocks from Hong Kong, which, according to my calculations, is the 16th largest net inflow day in the history of the program.

Shanghai, Shenzhen, and the STAR Board gained +1.94%, +3.36%, and +4.86%, respectively, though Mainland China semiconductors gained +6.8%, photolithography machine stocks gained +10.6%, the Semiconductor Manufacturing (SMIC) ecosystem gained +7.71%, and semiconductor equipment stocks were up +7.5%. Remember, this all occurred on the day of MSCI’s Semi-Annual Index Review’s implementation, which represents a net sale of both Mainland China and Hong Kong-listed stocks.

Many different moving parts contributed as the common narrative. A China-based semiconductor company's US intellectual property infringement case was dismissed. Meanwhile, there was also chatter of Chinese companies making progress on developing their own chip-making lithography machines. This is all very speculative at this point, though it is something we will keep an eye on, as it would have a material consequence on many of the US stock market darlings.

Buying from the National Team, which refers to institutional investors aligned with the government, such as the Social Security Fund and sovereign wealth fund Central Huijin, was clearly a factor as several Mainland China-listed equity ETFs favored by the National Team had high volumes.

The CSRC had an investor symposium on capital markets that included a statement that quantitative trading would not be banned, though jawboning down leverage in such strategies is clearly occurring. These strategies go long stocks with leverage, usually focusing on mid and small caps, and then hedging using futures.

President Xi and the Central Committee held a meeting focused on the economy before the Dual Sessions. The release stated, “Proactive fiscal policy must be appropriately intensified….enhance the consistency of macro policy….focus on expanding domestic demand, unswervingly deepen reforms”. This sounds good to me, though it does not seem to have been a significant factor in last night's market action. Premier Li also met with a delegation from the US Chamber of Commerce.

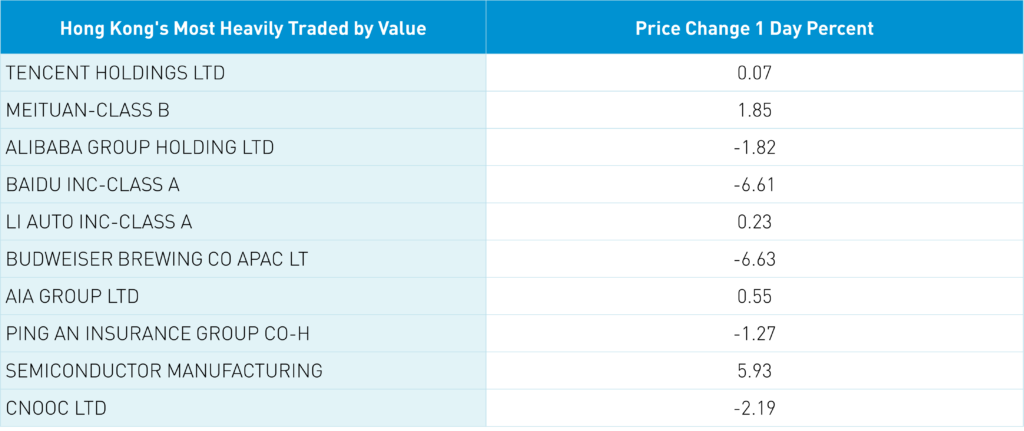

Hong Kong also overcame losses to end flat, as the Hang Seng Tech Index managed a small gain of +0.14%. Hong Kong’s most heavily traded stocks by value were Tencent, which pulled off a James Bond by gaining +0.07% despite being a net sell by MSCI, Meituan, which gained +1.85%, Alibaba, which fell -1.82% after cutting their cloud computing unit’s price, Baidu, which fell -6.61% after yesterday’s slight revenue miss and increased costs due to AI, and Li Auto, which gained +0.23% after strong Q4 financial results earlier in the week. Budweiser closed down -6.63% despite having the best ticker, 1876 HK, which represents the year in which the brewer was founded. It is interesting how Alibaba and Baidu’s cloud and AI efforts have had mixed results on financials, which, once again, has not affected US technology.

There was a fair amount of chatter on raising US tariffs on China EVs, though the tariffs are already sky-high, with Exhibit A being the lack of Chinese EVs in the US! That is, except for Polestars, which are a partnership between Volvo and China's Geely Automotive.

NetEase reported Q4 financial results after the HK close.

- Revenue increased +7% to RMB 27.1B ($3.8B) versus estimates of RMB 28.2B

- Adjusted net income increased to RMB 7.4B ($1B) from Q4 2022’s RMB 4.8B, versus estimates of RMB 7.9B

- The company spent $664mm buying 7.2mm ADRs in 2023

- The company will pay a dividend of $1.07 per ADR in March 2024.

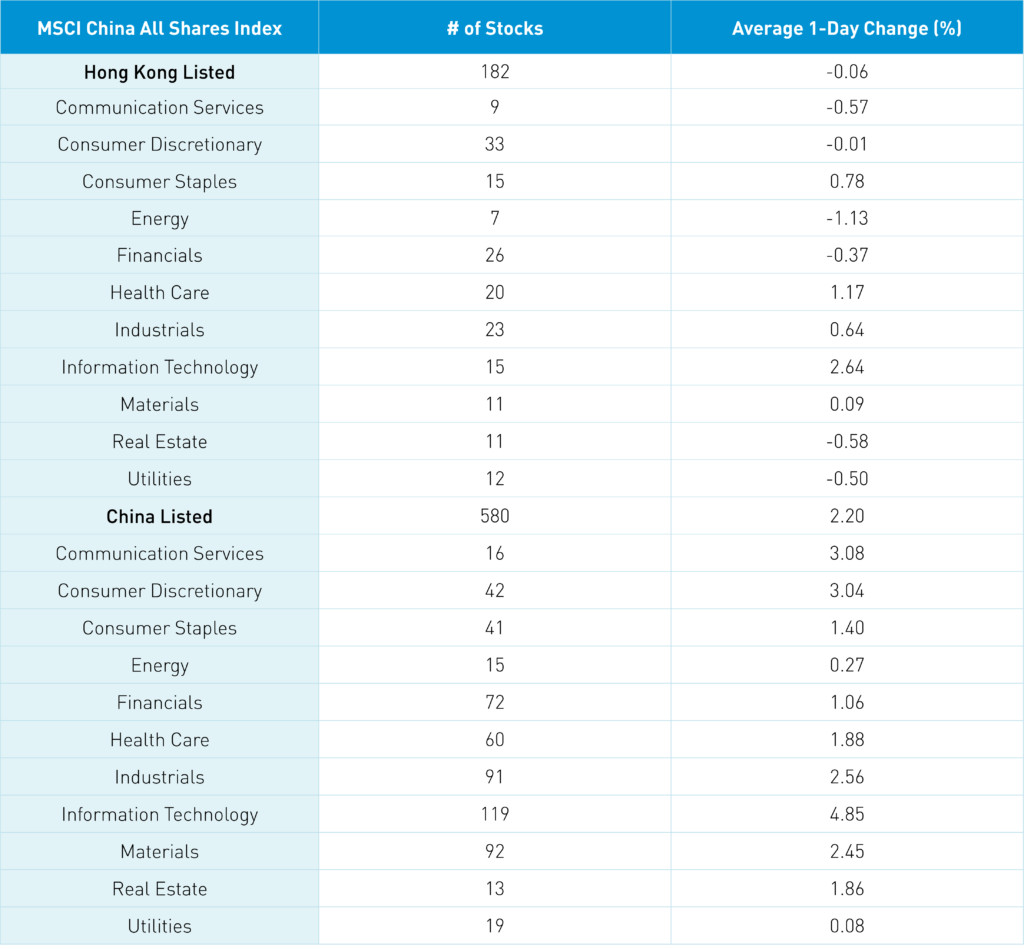

The Hang Seng and Hang Seng Tech indexes diverged to close -0.15% and +0.14%, respectively, on volume that increased +21.8% from yesterday, which is 131% of the 1-year average. 275 stocks advanced, while 199 declined. Main Board short turnover declined -8.25% from yesterday, which is 88% of the 1-year average, as 12% of turnover was short turnover (remember that Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor outperformed the value factor. The top-performing sectors were Technology, which gained +2.64%, Health Care, which gained +1.17%, and Consumer Staples, which gained +0.79%. Meanwhile, Energy fell -1.12%, Real Estate fell -0.58%, and Communication Services fell -0.57%. The top-performing subsectors were semiconductors, foodstuffs, and technical hardware equipment. Meanwhile, telecom, energy, and retailing were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought a net $174 million worth of Hong Kong-listed stocks and ETFs, including CNOOC, China Telecom, and Ping An, which were small net buys. Meanwhile, Tencent, China Shenhua, and Meituan were small net sells.

Shanghai, Shenzhen, and the STAR Board gained +1.94%, +3.36%, and +4.86%, respectively, on volume that declined -22.34% from yesterday, which is 95% of the 1-year average. 4,934 stocks advanced, while 92 declined. All factors were positive, as the growth factor and small caps outperformed the value factor and large caps. All sectors were positive. The top-performing sectors were Technology, which gained +4.86%, Communication Services, which gained +3.09%, and Consumer Discretionary, which gained +3.05%. All subsectors were also positive, led by photolithography, the Semiconductor Manufacturing International (SMIC) ecosystem, and semiconductors. Northbound Stock Connect volumes were very high as foreign investors bought a net $2.3 billion of Mainland stocks, including CATL, Sevenstar, and Wuxi AppTec, which were moderate net buys. Meanwhile, ZTE, Zhongji Innolight, and Foxconn were moderate net sells. CNY and the Asia dollar index were up slightly versus the US dollar. The Treasury curve steepened while copper and steel were lower.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.79 versus 7.78 yesterday

- Yield on 10-Year Government Bond 2.33% versus 2.33% yesterday

- Yield on 10-Year China Development Bank Bond 2.46% versus 2.47% yesterday

- Copper Price -0.12%

- Steel Price -0.47%