Profit Taking Rules the Day Despite NetEase and Bilibili Beating

4 Min. Read Time

NetEase Earnings Overview

Online gaming company NetEase (NTES US, 9999 HK) beat analyst expectations on revenue, adjusted net income, and adjusted EPS in Q1. NetEase continues to pay dividends, with a 1st quarter amount of $0.49 per ADR. Since January 2023, the company has spent $811mm buying back 8.9mm ADRs under the board-approved stock buyback plan of $5B.

- Revenue increased +7.2% to RMB 26.9B from Q1 2023’s RMB 25B versus expectations RMB 26.747B

- Adjusted Net Income increased to RMB 8.5B from RMB 7.57B versus expectations RMB 8.327B

- Adjusted EPS increased to RMB 13.10 from RMB 11.62 versus expectations RMB 12.759

Bilibili Earnings Overview

Online social media/video/gaming company Bilibili (BILI US, 9626 HK) also beat on the big three as the company was able to curtail its loss. Hopefully, the company will achieve profitability soon.

- Revenue +12% to RMB 5.66B from Q1 2023’s RMB 5.069B versus expectations RMB 5.606B

- Adjusted Net Income Loss decreased to RMB 439mm from YoY loss of RMB 1.028B versus loss expectations of RMB 497mm

- Adjusted EPS loss decreased to RMB 1.06 from YoY loss of RMB 2.51 versus loss expectations of RMB 1.20

Key News

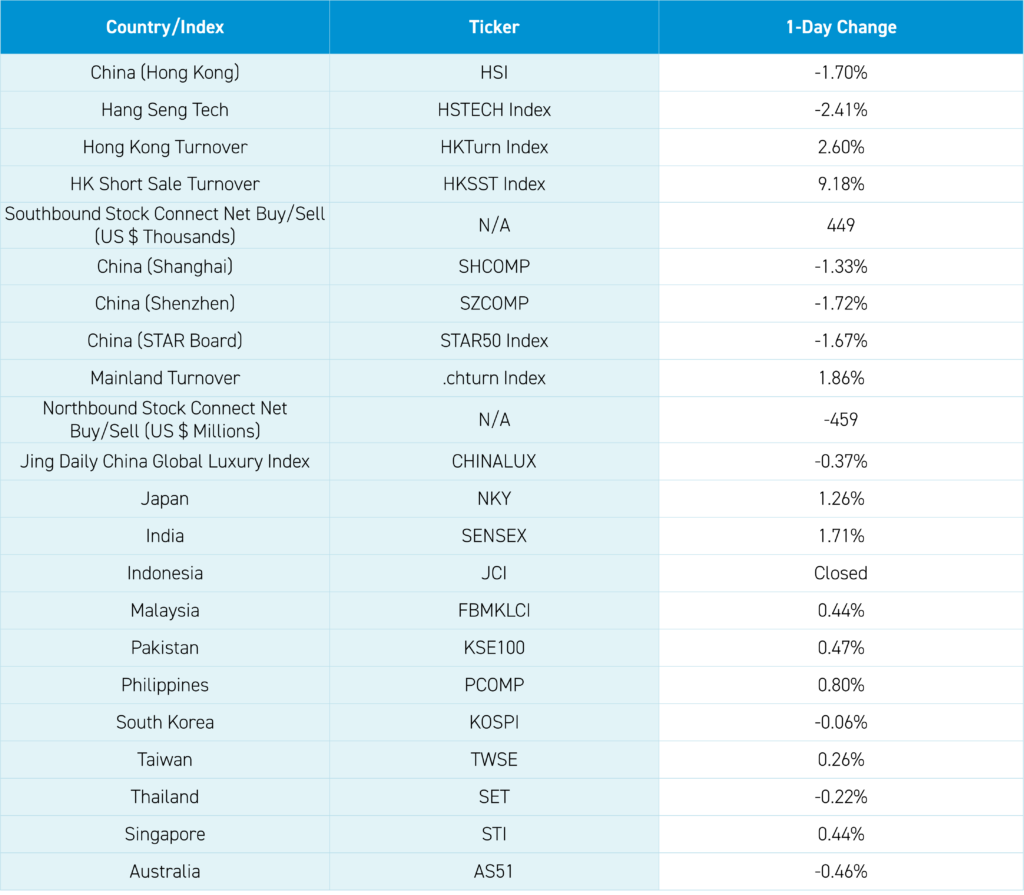

Asian equities were largely higher post-Nvidia’s better-than-expected Q1 financial results, with India outperforming, China and Hong Kong underperforming, and Indonesia still off for Vesak Day.

CNY is off very slightly this week versus the US dollar, with a Mainland media source calling WSJ Fed reporter Nick Timiraos the “Fed megaphone” after his comments on higher for longer, which Goldman Sachs CEO David Solomon echoed.

Hong Kong has been hit with a strong bout of profit-taking as technical analysts would point out that the relative strength index (RSI) breached the 70 level/upper band, indicating an overbought level. With the severity of the pullback, this is rapidly rectifying with the HS Tech RSI now 54 from Monday’s 73 (back on Jan 22, the RSI hit 22). Hong Kong diverged from the Mainland, with only 47 advancing stocks and 444, although Mainland investors bought the dip. The Hang Seng closed below 19,000, while the HS Tech closed below 4,000.

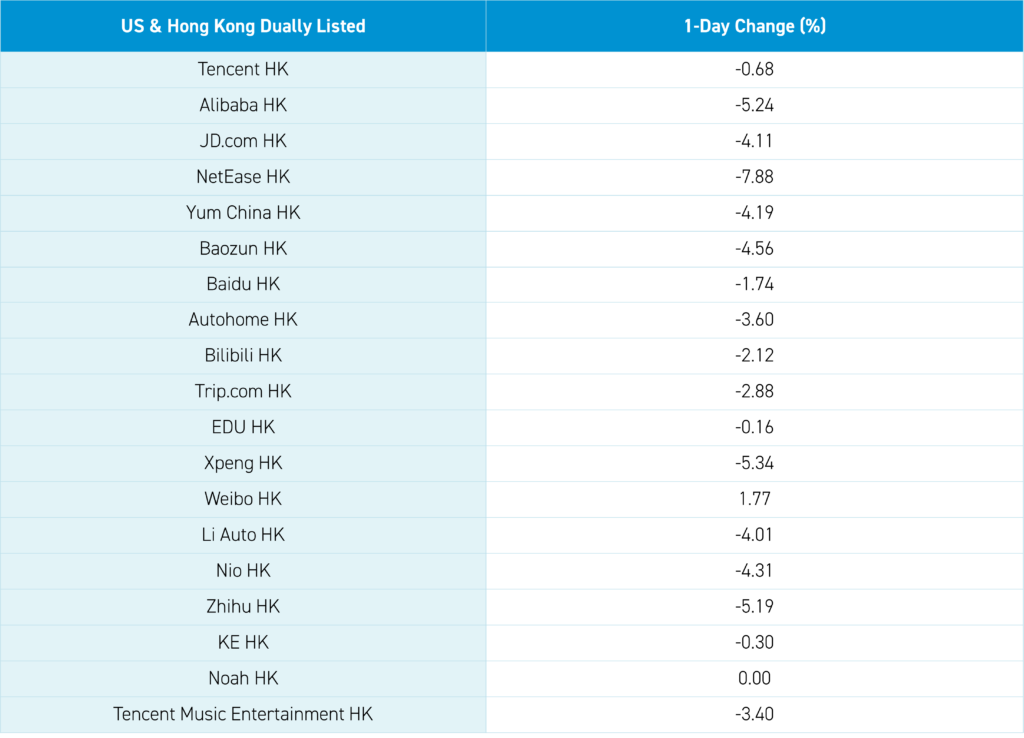

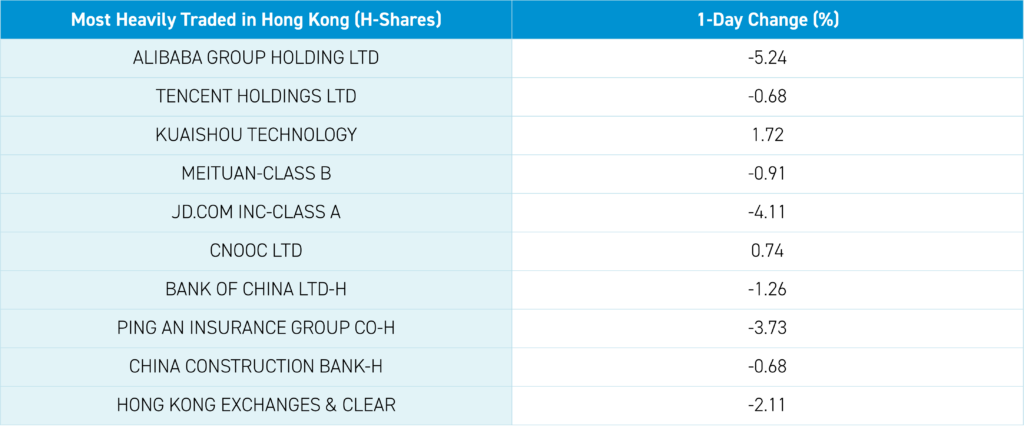

Hong Kong’s most heavily traded stocks were Alibaba, which fell -5.25% after PDD’s strong results indicating their market share gain in addition to price wars in cloud and AI and rumors of a convertible deal, similar to JD’s announcement yesterday, Tencent, which fell -0.68%, Kuaishou Technology, which gained +1.72% after strong results yesterday, Meituan, which fell -0.91%, and JD.com, which fell -4.11%. Convertible deals are dilutive, though if the interest rate is low (0.25% for JD), the financial math works.

Mainland China was off, but not nearly as much as Hong Kong. There was no indication of the National Team buying, looking at its two favored ETFs' trading volumes. There were positives, including yesterday’s strong results from Pinduoduo and Kuaishou.

Mainland China media noted President Biden and President Xi’s welcoming message to the 400 attendees from China and the United States attending the 14th China-US Tourism Leadership Summit in Xi’an. CSRC Vice Chairman Fang Xinghai spoke in London, stating, “Chinese listed companies traditionally have not paid enough dividends. We are now encouraging them to pay more dividends,” according to Reuters. After the close, President Xi “presided over a symposium of enterprises and experts” on economic reforms. It's good to see the economy is garnering attention from the top.

JP Morgan got attention as their China economist and strategist raised the bank's 2024 GDP target to 5.2% from 4.8%. On the lighter side, Rihanna is in Shanghai promoting Fenty Beauty. There were some positives though profit taking ruled the day as our trading buddy would say about the positives: “Market no care, you no care.”

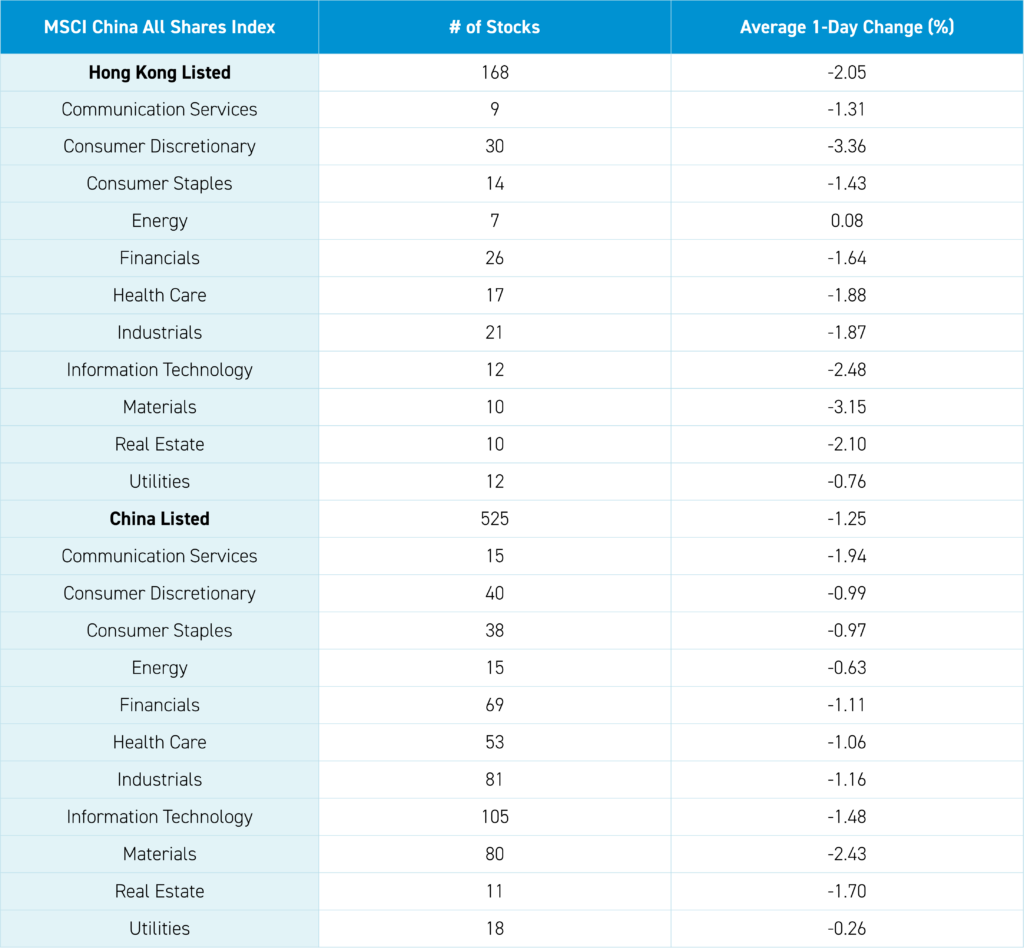

The Hang Seng and Hang Seng Tech indexes fell -1.70% and -2.41%, respectively, on volume that increased +2.6% from yesterday, which is 128% of the 1-year average. 47 stocks advanced, while 444 declined. Main Board short turnover increased +9.15% from yesterday, which is 95% of the 1-year average, as 13% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative, as value and large caps falling less than growth and small caps. Energy was the only positive sector, up +0.08% while Consumer Discretionary fell -3.36%, Materials fell -3.15%, and Technology fell -2.48%. Energy was the only positive sub-sector, while retail, materials, and media were the worst. Southbound Stock Connect volumes were moderate/high as Mainland investors bought a net $449 million worth of Hong Kong-listed stocks and ETFs, including Bank of China a large net buy, Kuaishou, CNOOC, and the Hong Kong Tracker ETF. Meanwhile, Tencent and Meituan were small net sells.

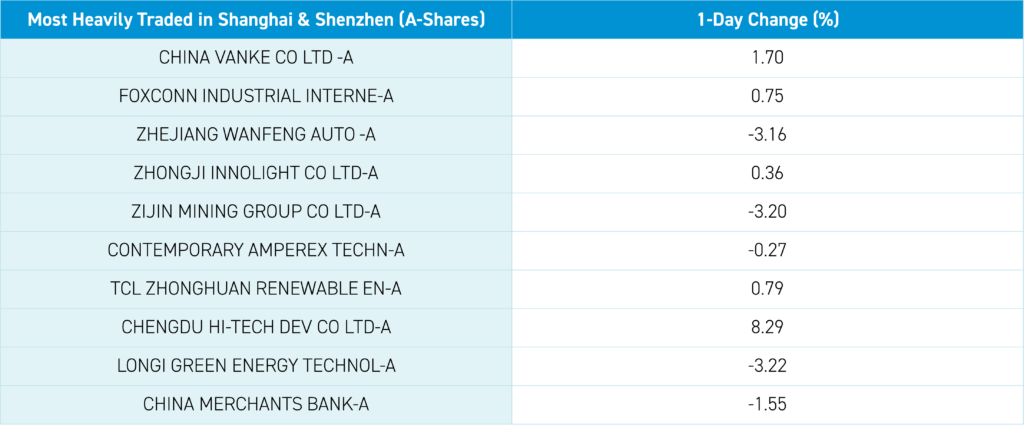

The Shanghai, Shenzhen, and the STAR Board fell -1.33%, -1.72%, and -1.67%, respectively, on volume that increased +1.86% from yesterday, which is 100% of the 1-year average. 461 stocks advanced, while 4,569 declined. All factors were negative with large caps and value “outperforming” growth and small caps. All sectors were negative, including Materials -2.42%, Communication Services, which fell -1.93%, and Real Estate, which fell -1.69%. All subsectors were negative, led lower by education, base metals, and precious metals. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$459 million worth of Mainland stocks, including Cypc, which was a moderate net buy, Kweichow Moutai and Tongwei small net buys while Foxconn, Weichai Power and Will Semiconductor were small net sells. CNY was lower versus the US dollar. Treasury bonds rallied. Copper and steel fell.

Happy birthday to my oldest son Mac!

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.23 yesterday

- CNY per EUR 7.85 versus 7.85 yesterday

- Yield on 10-Year Government Bond 2.30% versus 2.31% yesterday

- Yield on 10-Year China Development Bank Bond 2.41% versus 2.41% yesterday

- Copper Price -3.15%

- Steel Price -0.13%