Electric Vehicle Stocks Rally, EU Tariffs Called “Preliminary”

3 Min. Read Time

Key News

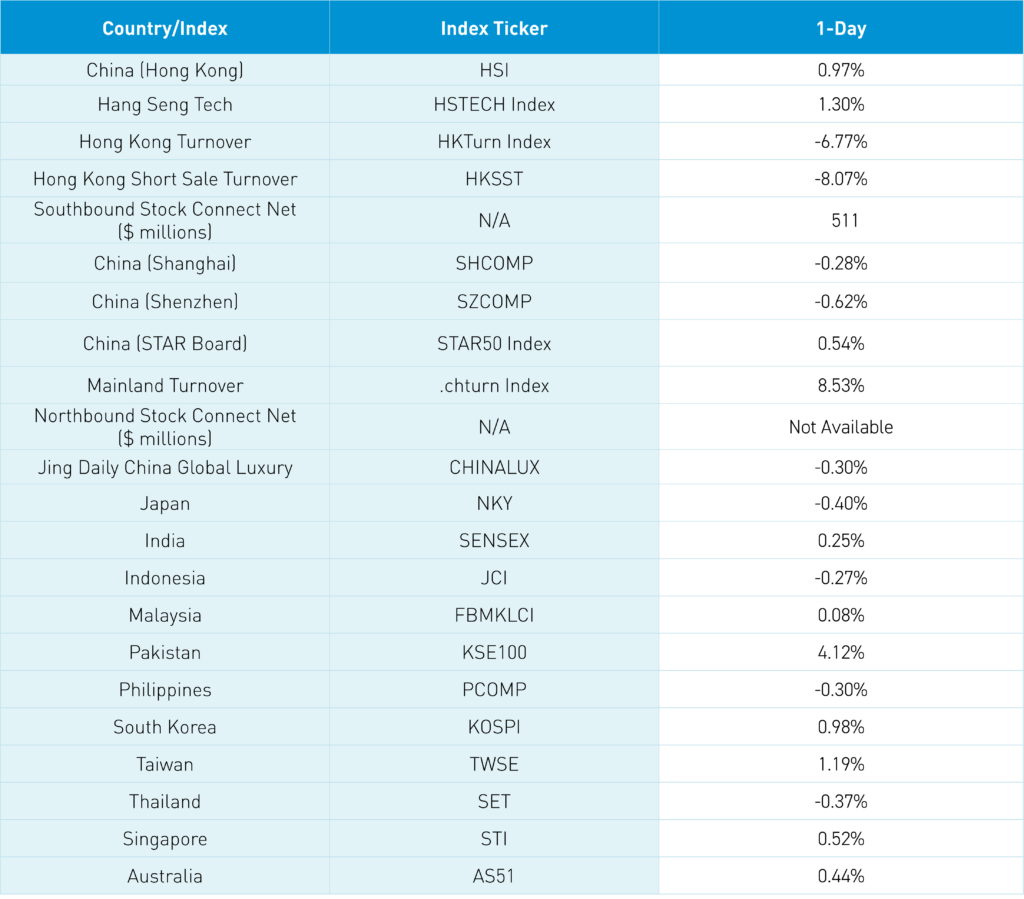

Asian equities celebrated the “light” US inflation print and the US Fed holding rates steady, as Pakistan outperformed the region and is up +23% year-to-date.

Despite headlines, the European Union’s China electric vehicle (EV) import tariffs turned out to be lighter than expected. However, more importantly, they are definitely “preliminary,” i.e., up for negotiation. Maybe a few copies of “The Art of The Deal” were sold in Brussels? The German government will likely fight the tariff proposal because German auto manufacturers have invested heavily in China. Meanwhile, French, Spanish, and Italian automakers have little market share to lose from retaliation. Chinese tariff retaliation would likely be directed at Airbus, French luxury goods, Spanish wine, etc. As mentioned yesterday, making cars requires a large workforce, which is why it has become such a hot-button issue for governments globally. And, yes, without question, China’s government has supported domestic auto companies.

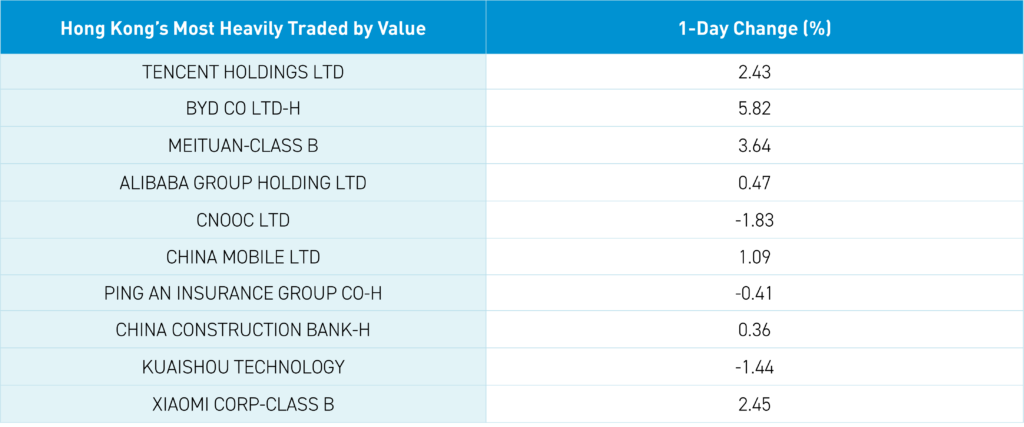

Hong Kong bounced around the room but rallied to close above the 18,000 level. The market was led higher by growth stocks as the most heavily traded stocks by volume were Tencent, which gained +2.43%; BYD, which gained +5.82%; Meituan, which gained +3.64%; Alibaba, which gained +0.47%; and energy giant CNOOC, which gained +1.23%. Hong Kong-listed companies are required to file their daily buybacks after the market closes. Tencent bought back 2.66 million shares today, and Meituan bought back 4.35 million shares. Maybe they should file before the market opens as it might change investor behavior. Mainland investors continue to buy Hong Kong-listed stocks and ETFs with $511 million worth of net buying today via Southbound Stock Connect.

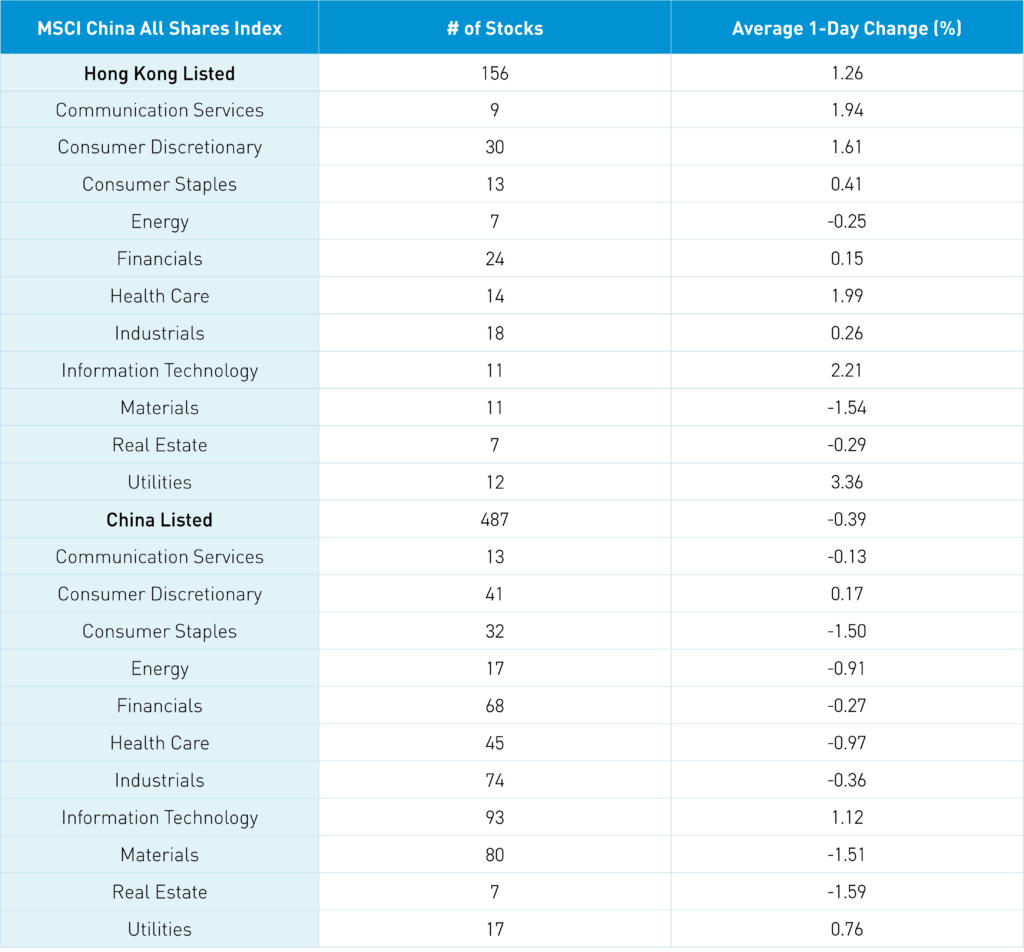

Technology was a top performer in Hong Kong, where the sector gained +2.22%, and in Mainland China, where the sector gained +1.13%. Semiconductors led technology higher after Broadcom’s strong financial results added to AI enthusiasm.

Mainland China fell close to posting small losses on little news. One of China’s National Team’s favorite ETFs, ticker 510300, had a slight pickup in volume last Thursday, Friday, and Tuesday (Monday was a holiday) on market weakness. It is hard to say, but it may be an indication of some more support?

The Hang Seng and Hang Seng Tech indexes gained +0.97% and +1.30%, respectively, on volume that decreased -6.77% from yesterday, which is 105% of the 1-year average. 308 stocks declined while 170 stocks advanced. Main Board short turnover declined -8.07% from yesterday, which is 97% of the 1-year average, as 16% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were positive with growth and small caps outperforming value and large caps. The top-performing sectors were Utilities, which gained +3.35%, Technology, which gained +2.21%, and Health Care, which gained +1.99%. Meanwhile, Materials fell -1.55%, Real Estate fell -0.3%, and Energy fell -0.26%. The top-performing subsectors were autos, utilities, and technical hardware. Meanwhile, materials and household products were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a net $511 million worth of Hong Kong-listed stocks and ETFs, including BYD and Meituan, which were moderate net buys.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.28%, -0.62%, and +0.54%, respectively, on volume that increased +8.53% from yesterday, which is 89% of the 1-year average. 1,776 stocks advanced, while 3,177 stocks declined. The growth factor managed to stay in the green while large caps fell less than small caps. The top-performing sectors were Technology, which gained +1.12%, Utilities, which gained +0.76%, and Consumer Discretionary, which gained +0.17%. Meanwhile, Real Estate fell -1.58%, Materials fell -1.50%, and Consumer Staples, which fell -1.49%. The top-performing subsectors were autos, semiconductors, and communication services. Meanwhile, agriculture, construction machinery, and retail were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors were net sellers of Mainland-listed stocks. CNY and the Asia Dollar Index were off versus the US dollar. The Treasury curve flattened. Steel and copper gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.25 versus 7.24 yesterday

- CNY per EUR 7.82 versus 7.83 yesterday

- Yield on 1-Day Government Bond 1.30% versus 1.30% yesterday

- Yield on 10-Year Government Bond 2.27% versus 2.28% yesterday

- Yield on 10-Year China Development Bank Bond 2.38% versus 2.39% yesterday

- Copper Price 0.43%

- Steel Price 0.19%