Stocks Slip On Summer Slowdown Before Third Plenum

5 Min. Read Time

Key News

Asian equities started the week lower on light volumes and little news as the summer slowdown appears to be setting in.

Hong Kong and Mainland China underperformed while Malaysia was closed for the Islamic New Year. Both markets were off on light volumes and poor breadth as investors’ expectations for economic policy support from next week’s Third Plenum appear to be low. The dismissive mood comes against the backdrop of slowing purchasing managers’ indexes (PMIs) and economic data, which one would anticipate raises the probability for policy support.

Another factor is the rising probability of a Trump second term as investors pause on increasing risk. For those concerned about Trump’s China policy, we recommend our webinar with Trump’s Ambassador to China Terry Branstad. There is also a summary of the conversation available here.

The People’s Bank of China (PBOC) announced a new arrow for its quiver as intra-day liquidity via repos and reverse repos was announced.

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.32%, Alibaba, which fell -1.51%, Meituan, which fell -1.76%, AIA, which fell -1.55%, and Hong Kong Exchanges -2.04% though internet plays had a few bright spots with Kuaishou +2.23% on an analyst Buy rating, JD.com +0.29% , Trip.com +0.52%, and Baidu, which was flat.

Clean tech was weak on Trump tariff concerns and NIO’s -3.89% decline after their CFO resigned for personal reasons.

Mega-caps were a rare bright spot in the Mainland market, which is an indication of the National Team’s intervention due to their impact on indices. Meanwhile, National Team-favored ETFs did not see a jump in volumes, unlike last week.

Mainland equities have been in a real funk since mid-May. Again, the thumbs-down from local investors should be on the radar for policymakers.

Semiconductors were a rare bright spot due to Will Semiconductor’s +4% gain after its first half 2024 preliminary financial results showed a net income increase of +754% year-over-year in dollar terms. Despite continued buybacks, maybe financial results will be too good for investors to ignore.

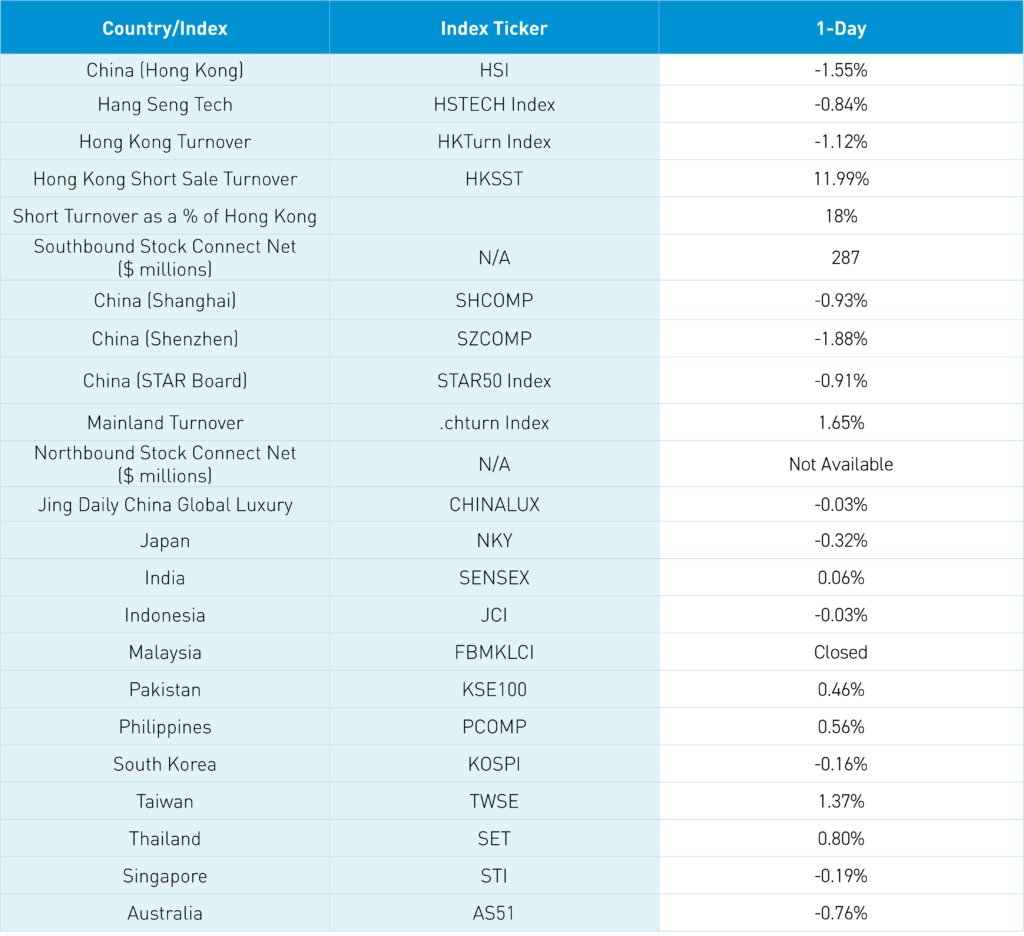

The Hang Seng and Hang Seng Tech indexes fell -1.55% and -0.84%, respectively, on volume that declined -1.12% from Friday, which is 87% of the 1-year average. 81 stocks advanced while 408 declined. Main Board short turnover increased +11.99% from Friday, which is 89% of the 1-year average as 18% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors and sectors were negative. Only telecom services and utilities were positive while pharmaceuticals, media, and consumer services were among the worst-performing subsectors. Southbound Stock Connect volumes were light as Mainland investors bought a net $287 million worth of Hong Kong-listed stocks and ETFs, including ICBC and Sense Time, which saw small net buys.

Shanghai, Shenzhen, and the STAR Board fell -0.93%, -1.88%, and -0.91%, respectively, on volume that increased +1.65% from Friday, which is 70% of the 1-year average. 455 stocks advanced while 4,563 declined. Large caps and value stocks “outperformed” (i.e. fell less than) small caps and growth stocks. Utilities and energy gained +1.94% and +0.05%, respectively, while real estate fell -2.49%, health care fell -2.32%, and consumer staples fell -1.85%. The top-performing subsectors were motorcycles, power industry, and telecom. Meanwhile, education, shipping, and software were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors were small net sellers of Mainland stocks, including Cypc, Kweichow Moutai, and BYD, which were small net buys and LXJM, HR, and Will Semiconductor were small net sells. Treasury bonds rallied. The US dollar strengthened versus CNY and the Asia Dollar Index. Copper gained while steel fell.

Last Night's Performance

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 154 | -1 |

| Communication Services | 9 | -0.3 |

| Consumer Discretionary | 29 | -1.2 |

| Consumer Staples | 13 | -2.1 |

| Energy | 7 | -0.6 |

| Financials | 24 | -0.8 |

| Health Care | 14 | -3.3 |

| Industrials | 18 | -2.8 |

| Information Technology | 11 | -1.4 |

| Materials | 11 | -0.3 |

| Real Estate | 6 | -2.7 |

| Utilities | 12 | -0.1 |

| China Listed | 487 | -0.9 |

| Communication Services | 13 | -1.8 |

| Consumer Discretionary | 41 | -0.6 |

| Consumer Staples | 32 | -1.8 |

| Energy | 17 | 0.1 |

| Financials | 68 | -0.4 |

| Health Care | 45 | -2.3 |

| Industrials | 74 | -1.1 |

| Information Technology | 93 | -0.7 |

| Materials | 80 | -1.1 |

| Real Estate | 7 | -2.5 |

| Utilities | 17 | 2 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | -0.3 |

| Alibaba HK | 9988 HK Equity | -1.5 |

| JD.com HK | 9618 HK Equity | 0.3 |

| NetEase HK | 9999 HK Equity | -1.4 |

| Yum China HK | 9987 HK Equity | -0.9 |

| Baozun HK | 9991 HK Equity | 7.2 |

| Baidu HK | 9888 HK Equity | 0 |

| Autohome HK | 2518 HK Equity | -3.1 |

| Bilibili HK | 9626 HK Equity | -0.4 |

| Trip.com HK | 9961 HK Equity | 0.5 |

| EDU HK | 9901 HK Equity | -3.6 |

| Xpeng HK | 9868 HK Equity | -2.5 |

| Weibo HK | 9898 HK Equity | 0.5 |

| Li Auto HK | 2015 HK Equity | -1.3 |

| Nio Auto HK | 9866 HK Equity | -3.9 |

| Zhihu HK | 2390 HK Equity | 3.6 |

| KE HK | 2423 HK Equity | -2.4 |

| Noah HK | 6686 HK Equity | 0 |

| Tencent Music Entertainment HK | 1698 HK Equity | -3.4 |

| Meituan HK | 3690 HK Equity | -1.8 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| Tencent Holdings Ltd | -0.3 |

| Alibaba Group Holding Ltd | -1.5 |

| Meituan | -1.8 |

| AIA Group Ltd | -1.6 |

| Hong Kong Exchanges and Clearings | -2 |

| Ping Insurance Group | -2.4 |

| HSBC Hodings PLC | -1 |

| China Construction Bank Corporation | 0.2 |

| Industrial and Commercial Bank | -0.9 |

| CNOOC Ltd | -0.4 |

| Shanghai and Shenzhen'sMost Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| Kweichow Moutai Ltd | -2.3 |

| BAIC BluePark New Energy Technology | 5.3 |

| COSCO Shipping Holdings | -6.1 |

| Lingyi iTech Guangdong | 9.4 |

| Luxshare Precision Industry | 1.7 |

| China Yangtze Power Ltd | 2.1 |

| Zhongji Innolight Ltd | 2 |

| Zijin Mining Group Ltd | -1 |

| Seres Group Ltd | -0.4 |

| Wuliangye Yibin Ltd | -2.4 |

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.27 versus 7.27 Friday

- CNY per EUR 7.88 versus 7.88 Friday

- Yield on 1-Day Government Bond 1.24% versus 1.24% Friday

- Yield on 10-Year Government Bond 2.29% versus 2.28% Friday

- Yield on 10-Year China Development Bank Bond 2.38% versus 2.36% Friday

- Copper Price +0.24%

- Steel Price -1.48%