Does Economic Data Raise The Probability of Third Plenum Policy Support?

6 Min. Read Time

Key News

Asian equities leaned higher overnight on light volumes and a stronger US dollar as Hong Kong underperformed while Japan was closed for Marine Day, which, according to Google, is meant “to give thanks for the ocean’s bounty”.

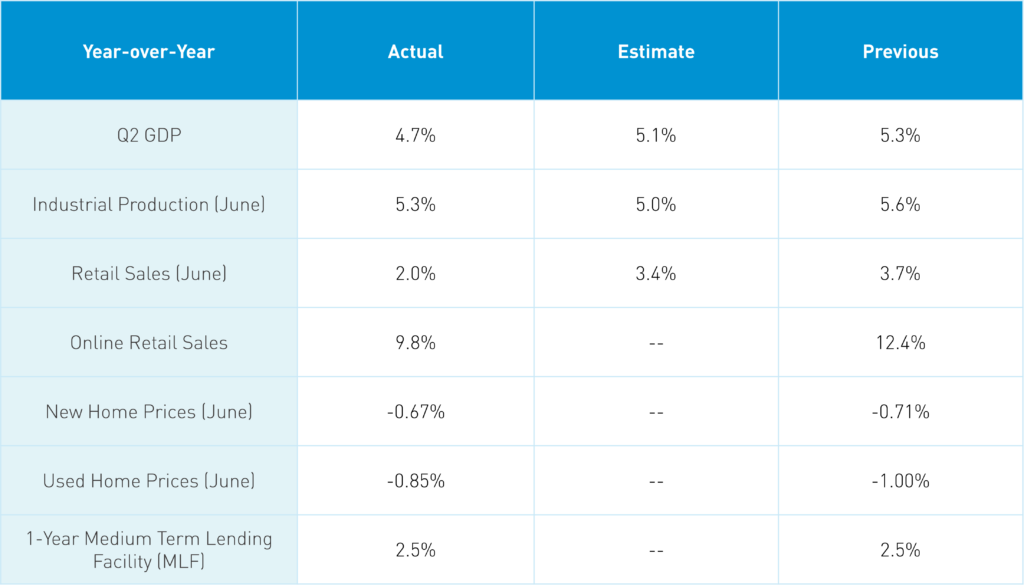

China’s weaker-than-expected economic data release weighed on sentiment in Hong Kong, especially growth stocks. However, the Hang Seng Index managed to stay above 18,000.

The decline in online retail sales growth in June should not be a surprise considering that most 6.18 festival sales actually occurred in May. As you can see, the release wasn’t all bad, though not great. There were also a few silver linings, including that several Tier-1 cities showed improvement in housing sales and prices.

Volumes were very light in Hong Kong, down -23% from Friday and at just 88% of the 1-year average, indicating that investors are waiting for Thursday’s Third Plenum read-out. Expectations going into the economic meeting are very low, though today’s data, along with Friday’s credit data, are likely to raise expectations for further policy support. If you were going to press on the gas, this feels like a good time to do it.

It was difficult to ascertain the consequences of the failed assassination attempt on former President Trump on markets overnight, though several risk-off assets were higher, including the US dollar, gold, and bitcoin. As our webinar with Trump’s China Ambassador Terry Branstad showed, we believe the potential for US-China dealmaking is higher with Trump than with Biden.

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.71%, Alibaba, which fell -2.23%, Meituan, which fell -2.22%, China Construction Bank, which fell -0.71%, and Baidu, which fell -5.58%. Mainland investors bought the dip in Hong Kong-listed socks via Southbound Stock Connect, resulting in a net $624 million worth of net buying, as the Hong Kong Tracker ETF saw large net buying. The Mainland markets were off, though mega-cap stocks outperformed, which mitigated the downdraft despite poor breadth. Along with an uptick in volumes in the ETFs favored by the National Team, one could assume there was an effort to limit today’s losses. CNY and the Asia Dollar Index were off versus the US dollar.

The Hang Seng and Hang Seng Tech indexes fell -1.52% and -2.90%, respectively, on volume that declined -23.68% from Friday, which is 88% of the 1-year average. 84 stocks advanced, while 403 declined. Main Board short sale turnover increased +0.98% from Friday, which is 95% of the 1-year average, as 19% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Large caps and the value factor “outperformed” (i.e. fell less than) small caps and the growth factor. The top-performing sectors were Energy, which gained +0.89%, Utilities, which gained +0.42%, and Materials, which gained +0.15%. Meanwhile, Real Estate fell -2.89%, Consumer Staples fell -2.65%, and Consumer Discretionary fell -2.42%. The top-performing subsectors were semiconductors, energy services, and basic utilities. Meanwhile, food and beverage, healthcare equipment, and retail were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a net $624 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which saw a large net inflow, and the Hang Seng China Enterprise ETF. Which saw a moderate net inflow, China Hong Qiao was a moderate net sell, and CNOOC was a small net sell.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.09%, -0.83%, and -0.35%, respectively, on volume that decreased -12.37% from Friday, which is 73% of the 1-year average. 794 stocks advanced while 4,189 stocks declined. Large caps and value “outperformed” (i.e. fell less than) small caps and growth stocks. The top-performing sectors were Energy, which gained +1.86%, Utilities, which gained +1.09%, and Financials, which gained +0.55%. Meanwhile, Consumer Discretionary fell -1.06%, Technology fell -0.73%, and Health Care and Real Estate were both off -0.52%. The top-performing subsectors were agriculture, coal, and precious metals. Meanwhile, household products, daily chemicals, and forest industry were among the worst-performing. Northbound Stock Connect volumes were moderate, as foreign investors were small net buyers of Mainland stocks, including Zijin Mining, CMOC, and Montage Technology. Meanwhile, BOE Technology was a moderate net sell, and Zhongji Innolight and Midea were small net sells. The US dollar gained overnight versus CNY and the Asia Dollar Index. Copper and steel gained.

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | -1.5% |

| Hang Seng Tech | HSTECH Index | -2.9% |

| Hong Kong Turnover | HKTurn Index | -23.7% |

| HK Short Sale Turnover | HKSST Index | 1% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 623.7 |

| China (Shanghai) | SHCOMP Index | 0.1% |

| China (Shenzhen) | SZCOMP Index | -0.8% |

| China (STAR Board) | Star50 Index | -0.3% |

| Mainland Turnover | .chturn Index | -12.4% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | -1.1% |

| Japan | NKY Index | -2.5% |

| India | SENSEX Index | 0.2% |

| Indonesia | JCI Index | -0.7% |

| Malaysia | FBMKLCI Index | 0.7% |

| Pakistan | KSE100 Index | 1.4% |

| Philippines | PCOMP Index | 0.6% |

| South Korea | KOSPI Index | 0.1% |

| Taiwan | TWSE Index | -0.2% |

| Thailand | SET Index | -0.3% |

| Singapore | STI Index | 0.1% |

| Australia | AS51 Index | 0.7% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 154 | -1.7 |

| Communication Services | 9 | -1.8 |

| Consumer Discretionary | 29 | -2.4 |

| Consumer Staples | 13 | -2.7 |

| Energy | 7 | 0.9 |

| Financials | 24 | -1 |

| Health Care | 14 | -2.2 |

| Industrials | 18 | -1.1 |

| Information Technology | 11 | -2.4 |

| Materials | 11 | 0.1 |

| Real Estate | 6 | -2.9 |

| Utilities | 12 | 0.4 |

| China Listed | 487 | 0 |

| Communication Services | 13 | -0.2 |

| Consumer Discretionary | 41 | -1.1 |

| Consumer Staples | 32 | 0.2 |

| Energy | 17 | 1.9 |

| Financials | 68 | 0.5 |

| Health Care | 45 | -0.5 |

| Industrials | 74 | -0.3 |

| Information Technology | 93 | -0.7 |

| Materials | 80 | 0.3 |

| Real Estate | 7 | -0.5 |

| Utilities | 17 | 1.1 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | -1.7 |

| Alibaba HK | 9988 HK Equity | -2.2 |

| JD.com HK | 9618 HK Equity | -4.7 |

| NetEase HK | 9999 HK Equity | 0.6 |

| Yum China HK | 9987 HK Equity | -2.2 |

| Baozun HK | 9991 HK Equity | -0.4 |

| Baidu HK | 9888 HK Equity | -5.6 |

| Autohome HK | 2518 HK Equity | 2.7 |

| Bilibili HK | 9626 HK Equity | 8.1 |

| Trip.com HK | 9961 HK Equity | -1.8 |

| EDU HK | 9901 HK Equity | -2 |

| Xpeng HK | 9868 HK Equity | -4.5 |

| Weibo HK | 9898 HK Equity | -3.1 |

| Li Auto HK | 2015 HK Equity | -4.3 |

| Nio Auto HK | 9866 HK Equity | 0.4 |

| Zhihu HK | 2390 HK Equity | -5.5 |

| KE HK | 2423 HK Equity | -2.1 |

| Noah HK | 6686 HK Equity | 0 |

| Tencent Music Entertainment HK | 1698 HK Equity | -0.2 |

| Meituan HK | 3690 HK Equity | -2.2 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| Tencent Holdings Ltd | -1.7 |

| Alibaba Group Holding Ltd | -2.2 |

| Meituan | -2.2 |

| China Construction Bank Corporation | -0.7 |

| Baidu Inc | -5.6 |

| CNOOC Ltd | -1.5 |

| Industrial and Commercial Bank of China | -0.7 |

| Chinaa Mobile Ltd | -0.3 |

| AIA Group Ltd | -0.4 |

| Ping Insurance Group | -2.2 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| Seres Group Ltd | -5.7 |

| Chongqing Changan Automobiles | 1.3 |

| BAIC BluePark New Energy Technology | -1.8 |

| BOE Technology Group | -7.4 |

| GoerTek Inc | 2.2 |

| Kweichow Moutai Ltd | -0.3 |

| Zhongji Innolight Ltd | -0.4 |

| Industrial & Commercial Bank of China | 2 |

| BYD Ltd | -0.4 |

| Chengtun Mining Group Ltd | 7.3 |

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.26 versus 7.25 yesterday

- CNY per EUR 7.92 versus 7.91 yesterday

- Yield on 1-Day Government Bond 1.31% versus 1.24% yesterday

- Yield on 10-Year Government Bond 2.25% versus 2.26% yesterday

- Yield on 10-Year China Development Bank Bond 2.33% versus 2.34% yesterday

- Copper Price +0.56%

- Steel Price +0.71%