NDRC Reiterates Ministry of Finance Policy Support

4 Min. Read Time

Key News

Asian equities were mixed overnight on Middle East tension escalation, as Taiwan outperformed on strong Q2 growth from US tech and semiconductors while Japan was hit hard on the Bank of Japan's interest rate hike and Yen strengthening.

Hong Kong and Mainland China were hit with profit-taking after yesterday's strong rally following the Ministry of Finance press conference on stimulus plans following the Third Plenum. Also weighing on sentiment was the July Caixin Manufacturing PMI release of 49.8 versus expectations of 51.5 and June’s 51.8. The data indicates the global economy is slowing, bolstering US Fed cut incentives and the necessity of raising China’s domestic consumption.

Yesterday’s National Development and Reform Commission (NDRC) press conference led by Deputy Secretary General Yuan Da garnered very little attention as certain elements of the conference were not released until today. He stated that, “The next step is to actively expand domestic demand” by “the promotion of consumption…such as automobiles and home appliances” funded by government special purpose bonds. Does this mean there is a cannonball coming?

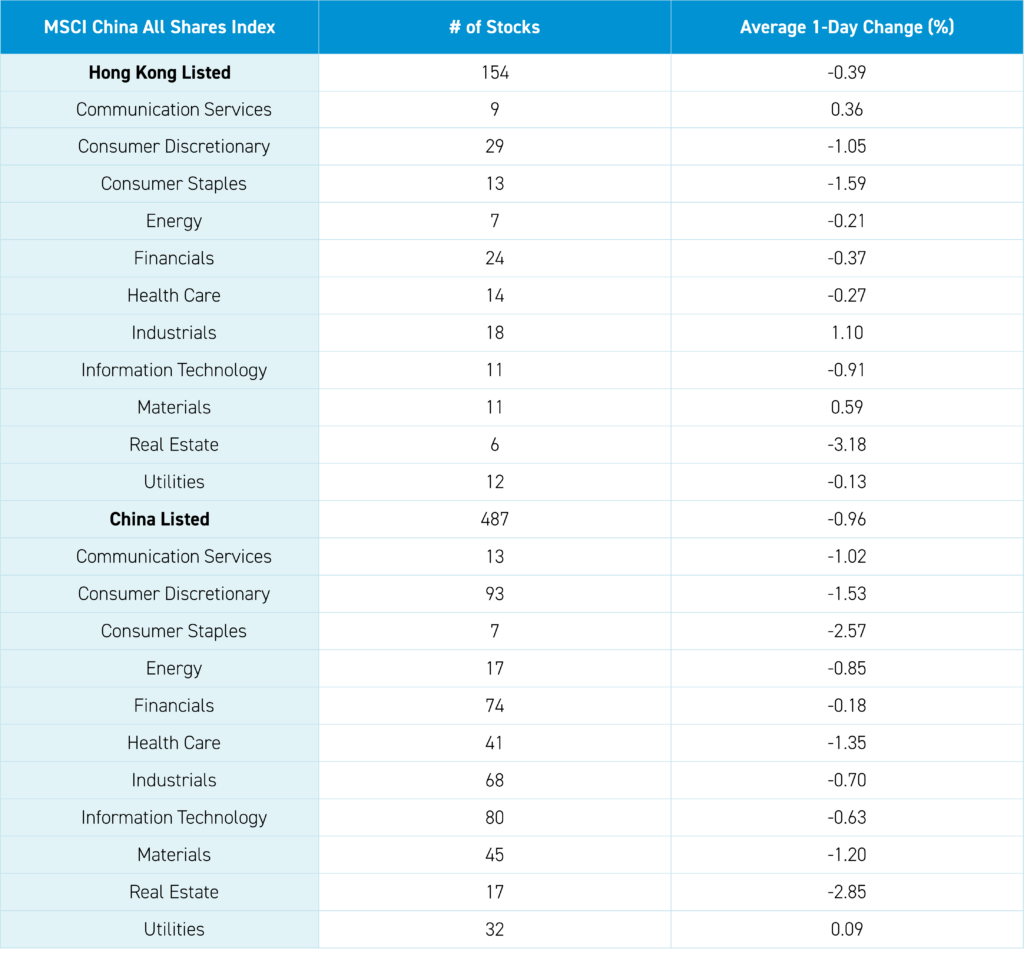

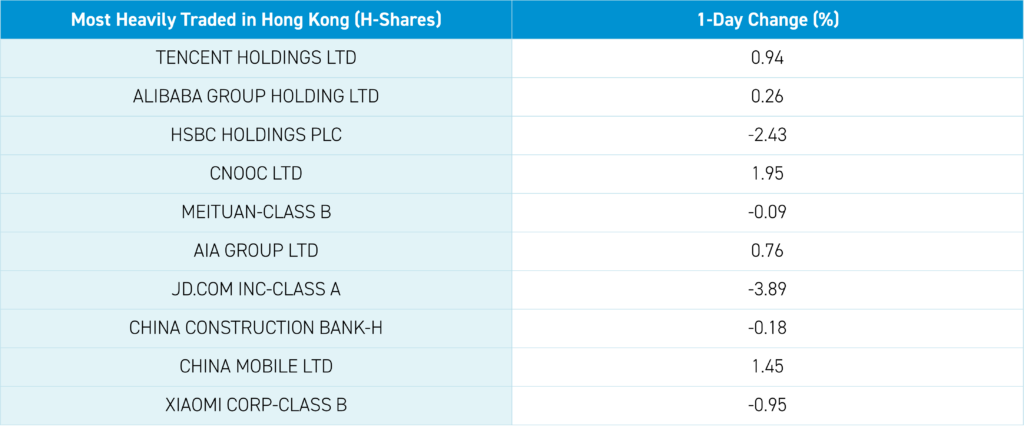

Hong Kong had a better day than it looked as Hang Seng Index heavyweight HSBC fell -2.43%, though the bank stock is not part of MSCI China due to its London domicile, accounting for 60% of the index's fall. Meanwhile, JD.com fell -3.89%, accounting for almost half of the Hang Seng Tech index decline. There was very little news on JD’s fall, except for a Mainland media source stating the company is putting revenue growth over profitability in Q2 on increased competition from PDD. However, JD should benefit from home appliance subsidies. JD’s Q2 financial results will be released on August 15th.

TAL Education (TAL US) beat on revenue, adjusted net income, and adjusted earnings per share (EPS) this morning, pre-market open. Yesterday, online auto seller Autohome (ATHM US) reported Q2 financial results that beat the big three as well, though the US-listed ADR only gained +2.34%. New Orient Education's (EDU US) results look like a miss. BYD fell -0.52% despite announcing a global partnership ex the US with Uber to supply 100,000 electric vehicles (EVs) to global drivers. After the close, the company announced July new energy vehicle (NEV) sales were 342,383 NEVs (EV & Hybrid), which is up +30.6% year over year and +0.21% from June. Has anyone noticed President Trump’s comment on allowing Chinese EV makers to manufacture in the US if they build factories here?

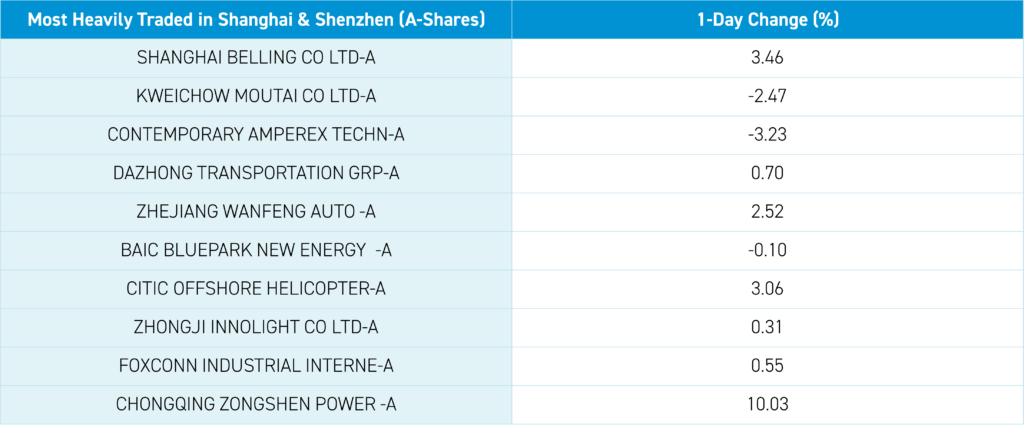

Hong Kong-listed ETFs had very large buying from Mainland investors today, totaling $1.07 billion. What do they see that is causing them to buy? Mainland markets had a weak day except for mega-oil and banks, while foreign growth stock favorites, including Kweichow Moutai, which fell -2.47%, and CATL, which fell -3.23% on net selling via Northbound Stock Connect. Despite the mounting economic stimulus, equity markets can’t ignite animal spirits as Treasury bonds rallied (again), though copper and steel rallied.

Reuters quoted a Goldman Sachs report stating the global hedge funds’ China allocation fell to 6.6% from 15%, the lowest level in five years, while Japan was a large overweight, though the allocation was not given. We believe the unwinding of low investor positioning could help fuel another China equity rally. In addition to weak economic data that has weighed on the Chinese markets since mid-May, MSCI’s quarterly rebalance pro forma will be released next Tuesday night. China’s weight in indices is likely to fall due to China's weakness in the equity market and India's strength. China’s weight could slip within Asia Pacific due to Japan’s equity strength, except for today's performance. Could the MSCI India and Japan weight increase against the backdrop of China's second half economic stimulus market top? We shall see!

Alibaba announced the first-ever AI-powered conversational sourcing engine for global business-to-business (B2B) suppliers both inside and outside of the Alibaba ecosystem. The tool is being rolled out worldwide. Alibaba is a sleeper AI play. Our team was able to experience the depth of their AI tools for merchants and shoppers alike on their visit to Hangzhou. This new tool will certainly help the company's international digital commerce (AIDC) stand out on the global market. The business unit is already experiencing growth rates comparable to PDD's. "I believe our AI-powered conversational sourcing engine will further supercharge the growth of Alibaba International Digital Commerce Group, by transforming the way tens of millions of global small and medium-sized enterprises operate within the 20 trillion-dollar B2B e-commerce industry," said Kuo Zhang, president of Alibaba.com, which is the name given to the B2B unit of AIDC.

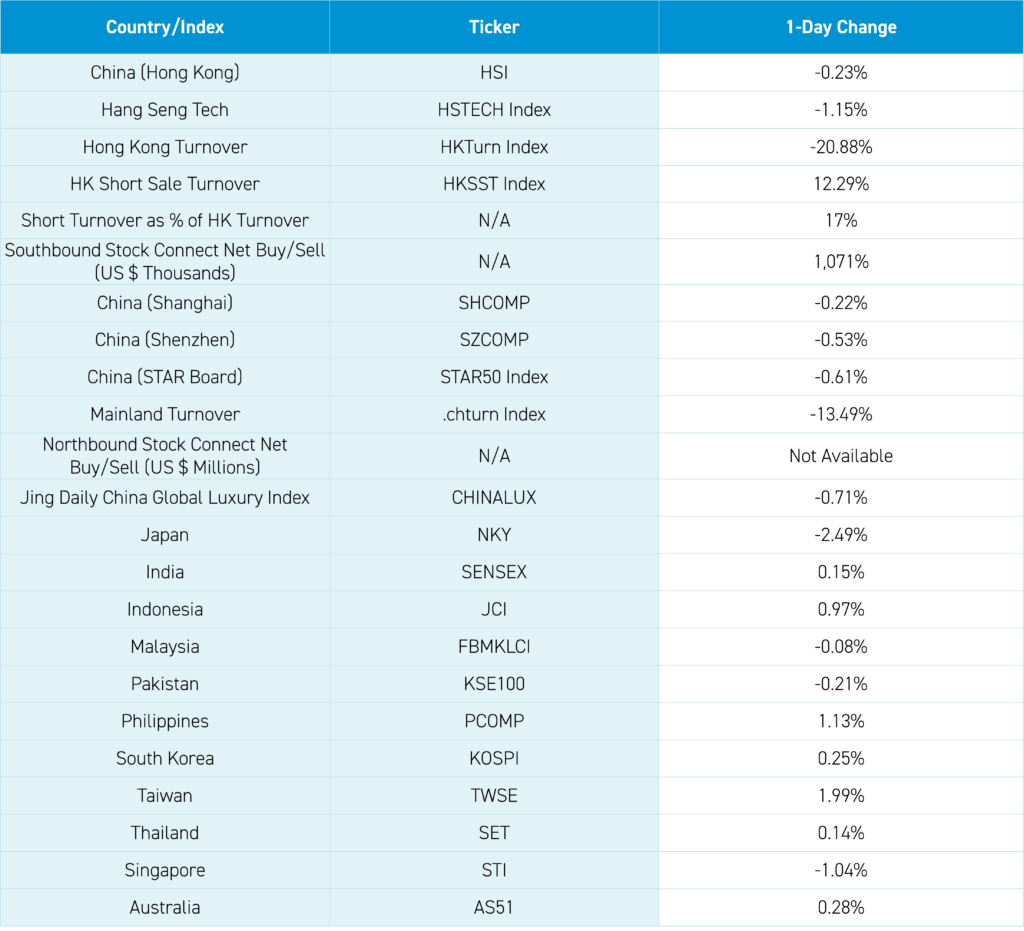

The Hang Seng and Hang Seng Tech indexes both closed lower by -0.23% and -1.15%, respectively, on volume that declined -20.88% from yesterday, 92% of the 1-year average. 162 stocks advanced, while 309 declined. Main Board short turnover increased +12.29% from yesterday, 96% of the 1-year average, as 17% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Value and large caps “outperformed”, i.e. fell less than, small caps and the growth factor. The top-performing sectors were Industrials, which gained +1.10%, Materials, which gained +0.58%, and Communication Services, which gained +0.35%. Meanwhile, Real Estate fell -3.18%, Consumer Staples fell -1.59%, and Consumer Discretionary fell -1.06%. The top-performing subsectors were Utilities, Telecom, and Transportation. Meanwhile, food & beverage, tobacco, and real estate were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a net $1.071B of Hong Kong stocks, with the Hong Kong Tracker ETF a very large net buy, HS China Enterprise ETF, HS Tech ETF, and Tencent large net buys.

Shanghai, Shenzhen, and the STAR Board fell -0.22%, -0.53%, and -0.61%, respectively, on volume that decreased -13.49% from yesterday, which is 96% of the 1-year average. 2,083 stocks advanced, while 2,674 declined. Value and large caps “outperformed”, i.e. fell less than, small caps and the growth factor. Utilities +0.09% was the only positive sector, while real estate -2.85%, staples -2.56%, and discretionary -1.52%. The top sub-sectors were education, highway, and land transportation, while chemicals, liquor, and construction machinery were the worst. Northbound Stock Connect volumes were moderate as foreign investors sold Mainland stocks with Wuxi AppTec, Citic, and Cambricon small net buys, while BYD, Wanha, and SCC were moderate net sells. CNY and the Asia dollar index fell versus the US $. Treasury bonds rallied. Copper and steel gained.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.22 yesterday

- CNY per EUR 7.81 versus 7.81 yesterday

- Yield on 10-Year Government Bond 2.13% versus 2.15% yesterday

- Yield on 10-Year China Development Bank Bond 2.20% versus 2.22% yesterday

- Copper Price: +1.83%

- Steel Price: +1.02%