Does The Yen Signal Once-In-A-Decade Market Transformation?

3 Min. Read Time

Key News

Asian equities rebounded as the Yen weakened by -1.88% versus the US dollar overnight after the Bank of Japan's Deputy Governor Shinichi Uchida stated they won’t hike further if there is market turmoil. This implies to me that more hikes are coming at some point.

A higher yen would mean, “The only playbook you can discard is the playbook you’ve had for decades,” according to consultant Stephen Miller in a Bloomberg article. Could that reverberate across other perennial winners, such as the 15-year winning streak of US equities versus non-US equities and the stronger US dollar since 2011? Time will tell, though no one is positioned for a market regime change.

July exports were 7% versus expectations of 9.5% and June’s 8.6%, though imports of 7.2% beat expectations of 3.2% and June’s -2.3%. Notice all the headlines are focused on the exports miss and nothing on the import beat? If it bleeds, it leads, as they say! Weaker exports indicate the global economy is slowing, while domestic demand could be firming, though higher commodity prices would lift imports. The Chinese government will be “adding controls and regulation on the production of three chemicals used to make illicit fentanyl” in what was described by the National Security Council as “the third significant” action in US-China counter-narcotics cooperation.

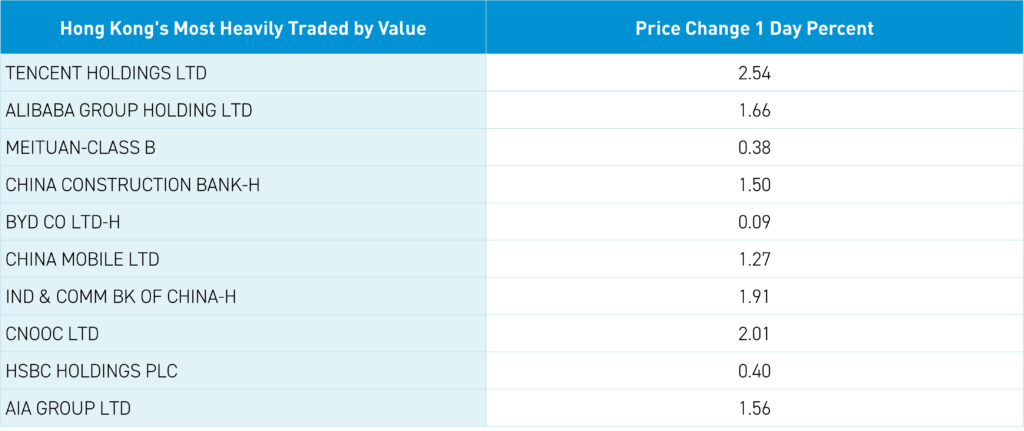

Hong Kong had a good day, with all sectors positive on decent volume and breadth. Mainland investors bought a healthy $1.497 billion of predominantly Hong Kong ETFs and Tencent via Southbound Stock Connect. Hong Kong’s most heavily traded stocks by value were Tencent, up +2.54%, Alibaba, up +1.66%, Meituan, up +0.38%, China Construction Bank, up +1.5%, and BYD, up +0.09%. Tomorrow, we have the State Council press conference on service consumption.

The Mainland market was mixed on foreign selling via Northbound Stock Connect as markets can’t quite shake the doldrums. The National Team appeared to have the day off based on light volumes in their favorite ETFs. The South China Morning Post had an article noting, “despite the repeated determination vowed by Beijing, including in the Politburo’s midyear economic review that underlined consumption as a focus on expanding domestic demand, business and consumer confidence has remained tenuous.” Sounds like firmer fiscal support is needed! Mainland media noted Guangzhou is the first Tier One city, a mega city, to push affordable housing in order to stabilize housing prices. The measures would include those with “quasi-hukou,” i.e., non-city citizens would get full city citizenship with a housing purchase. More to come on this!

Lost in Monday's chaos was the weekend release of July Caixin Services PMI, which beat expectations of 51.5 with a 52.1 and was better than June’s 51.2. Drivers were improving employment and new orders, though input prices improved and overseas demand weakened. Clearly, the release was a non-factor in Monday trading, though it is worthwhile to point out.

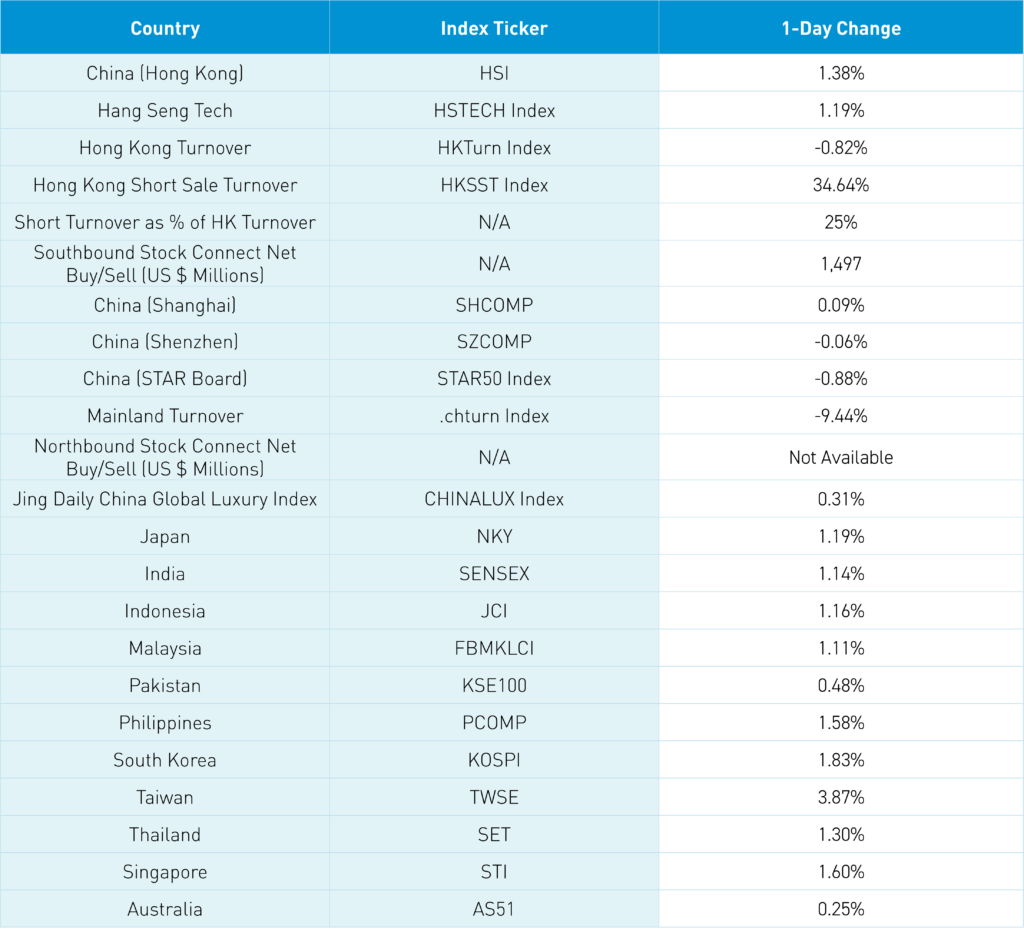

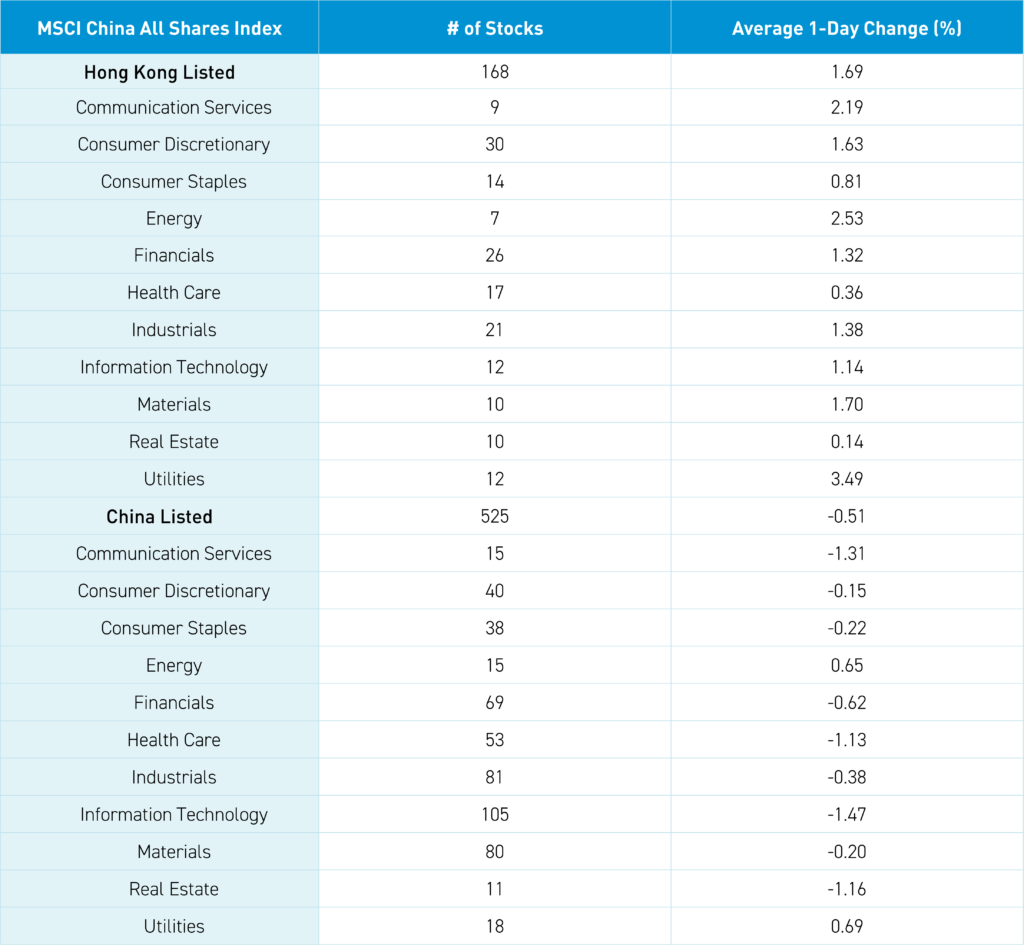

The Hang Seng and Hang Seng Tech gained +1.38% and +1.19% on volume -0.82% from yesterday, which is 94% of the 1-year average. 348 stocks advanced, while 124 declined. Main Board short turnover increased by +34.64% from yesterday, which is 135% of the 1-year average, as 25% of turnover was short turnover (HK short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Large caps and momentum outperformed today. All sectors were positive, led by utilities, up +3.49%, energy, up +2.53%, and communication services, up +2.18%. The top sub-sectors were media, utilities, and energy, while food/staples were the only negative. Southbound Stock Connect volumes were light as Mainland investors bought a healthy $1.497 billion of Hong Kong stocks, with the Hong Kong Tracker ETF having a massive net buy, Tencent, HS China Enterprise ETF, and HS Tech large net buys.

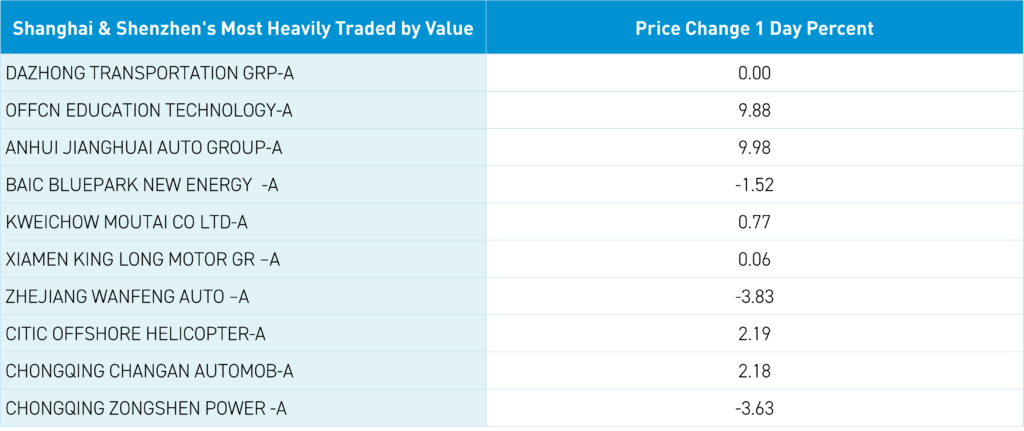

Shanghai, Shenzhen, and STAR Board were mixed +0.09%, -0.06%, and -0.88%, respectively, on volume down -9.44% from yesterday, which is 73% of the 1-year average. 2,219 stocks advanced, while 2,587 declined. Large and value outperformed small and growth. Utilities and energy were the only positive sectors up +0.69% and +0.66%, while technology fell -1.46%, communication services fell -1.3%, and real estate fell -1.16%. The top sub-sectors were motorcycle, education, and communication equipment, while computer hardware, catering/tourism, and agriculture were the worst. Northbound Stock Connect volumes were light as foreign investors were net sellers of Mainland stocks, with Kweichow Moutai a small/moderate net buy while BYD and CATL were small net sells. CNY and the Asia dollar index fell versus the US dollar index. Treasury bonds rallied. Copper gained while steel fell.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.18 versus 7.15 yesterday

- CNY per EUR 7.83 versus 7.80 yesterday

- Yield on 10-Year Government Bond 2.14% versus 2.14% yesterday

- Yield on 10-Year China Development Bank Bond 2.19% versus 2.21% yesterday

- Copper Price: +0.45%

- Steel Price: -0.69%