Alibaba, JD.com, PBOC, & Economic Data Reviewed!

6 Min. Read Time

Alibaba Q2 Earnings Overview

Alibaba's quarterly results were mixed, missing analyst expectations. During the Q&A, the company noted that their new service charge will go into effect in September, which will positively affect financials going forward. The company pointed out in the Q&A that it has a shareholder vote this month to make Hong Kong a primary listing venue along with New York, which would allow the company to go into Southbound Stock Connect. This is a significant catalyst, in my opinion. The company's implementation of AI tools will positively impact financials as AI budgets are “higher, significantly higher” as industries have to invest in AI.

While revenue posted a small year-over-year (YoY) gain, as we expected, the core China E-Commerce business fell -1% YoY, though the company did not blame China’s tepid domestic consumption. Instead, the company emphasized the “stabilizing market share of Taobao and Tmall Group as we returned the business on the growth trajectory.” Unlike the headlines, the company reported their 6.18 (June 18th) sales event “delivered strong online gross merchandise value (GMV) growth year-over-year” while the company’s premium buyer program called 88VIP “increased by double-digits year-over-year, surpassing 42 million during the quarter.” 6.18 discounts due to fierce competition are the likely culprits in net income and earnings per share (EPS) declines. I had thought and hoped that buybacks would help EPS. Other businesses did well, including Cloud, where the company noted a big investment as cash flow declined. Meanwhile, international efforts are going great as Lazada has become profitable recently, along with logistics.

- Revenue +4% to RMB 243.236B ($33.47B) versus analyst expectations of RMB 249B

- Taobao & Tmall (China e-commerce) -1% to RMB 113.373B ($15.601B) from RMB 114.953B

- Cloud Intelligence +6% to RMB 26.549B ($3.653B) from RMB 25.065B

- Alibaba International +32% to RMB 29.293B ($4.031B) from RMB 22.123B

- Cainiao Smart Logistics +16% to RMB 26.811 ($3.689B) from RMB 23.164B

- Adjusted Net Income -9% to RMB 40.691B from RMB 44.922B versus analyst expectations RMB 37.5B

- Adjusted EPS -5% to RMB 2.05 versus analyst expectations RMB 15.24

- The company purchased 613mm shares/77mm ADRs for $5.8B, decreasing the shares outstanding by 445mm/2.3%.

- Cash on the balance sheet is RMB 613.678B from RMB 617.23B

JD.com Q2 Earnings Overview

JD.com's quarterly results beat analyst expectations despite a difficult YoY comparison in electronics and home appliances, as “growth in our general merchandise category, particularly supermarket, remained robust,” according to CFO Ian Su Shan in the press release. Tomorrow’s report will include a deep dive into their conference call, which occurred during Alibaba’s. More to come!

- Revenue +1.2% to RMB 291.397B ($40.098B) from RMB 287.931B versus analyst expectations of RMB 290B

- JD Retail revenue increased +1.5% to RMB 257.072B ($35.374B) from RMB 253.28B

- Electronics & home appliance sales -4.6% to RMB 145.061B ($19.961B), though general merchandise sales +8.7% RMB 88.847B ($12.226B) from RMB 81.724.

- Adjusted Net Income to RMB 14.5B from RMB 8.6 versus analyst expectations RMB 9.7B

- Adjusted EPS +73.7% to RMB 9.36 from RMB 5.39B versus analyst expectations RMB 6.20

- The company bought 136.8mm/68.4 ADRs for $2.1B, which is 4.5% of the outstanding shares.

- Cash on the books increased to RMB 84.496B from RMB 71.892B

Key News

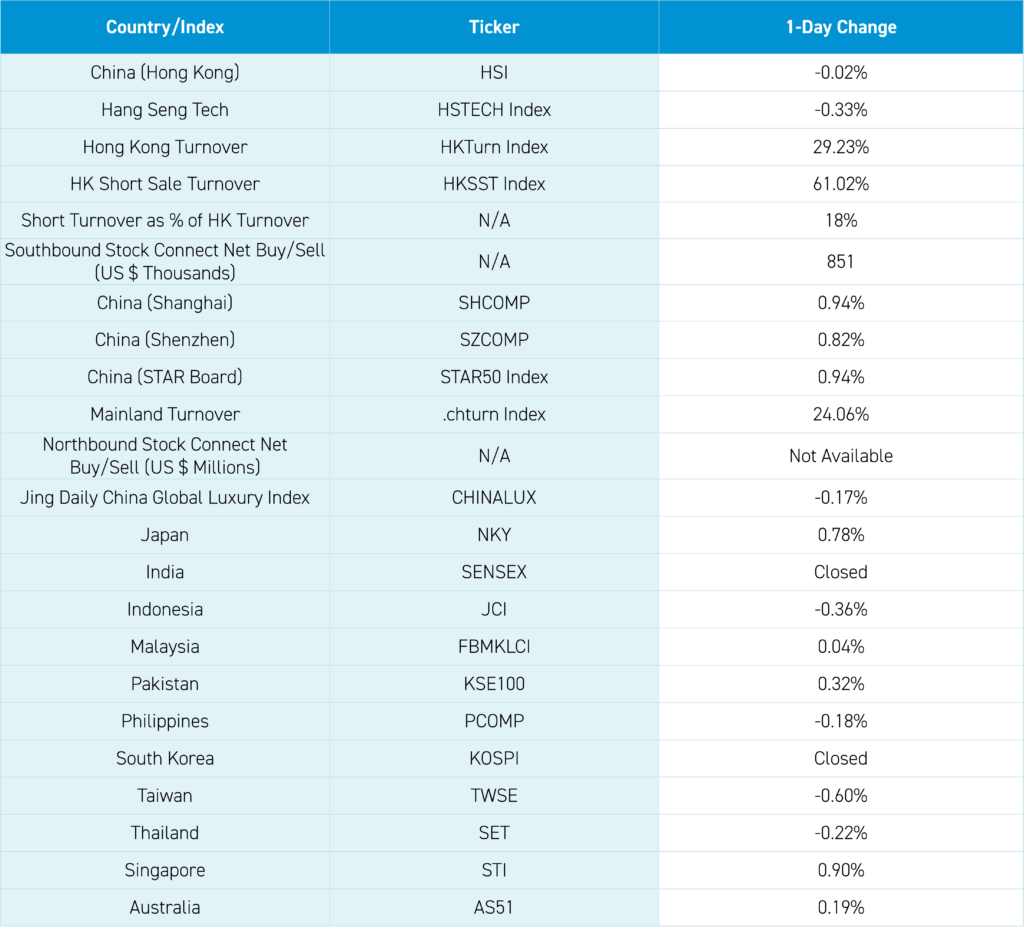

Asian markets were higher after a mild US CPI print, though India closed for Independence Day and South Korea was closed for Liberation Day.

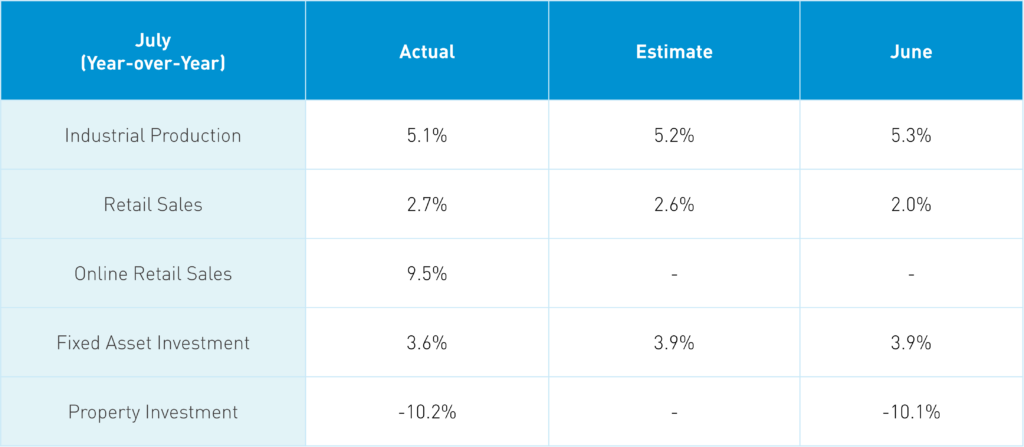

After the close, PBOC President Pan Shinyia was interviewed, and he stated the PBOC had made “three large adjustments in monetary policy.” However, the central bank “will follow the central government and State Council request to further plan new incremental policies.” Real estate policy adjustments have included “the down payment ratio of mortgage loans has now dropped to 15%, which is the lowest in level in history.” The interview demonstrates more policies are coming, which was reaffirmed by today’s mixed economic release.

July Economic Release

It is worth noting that Northbound Stock Connect had its first significant net buy of almost $2B as Mainland ETFs favored by the National Team saw above-average volumes, which helped the Mainland market to post a strong day.

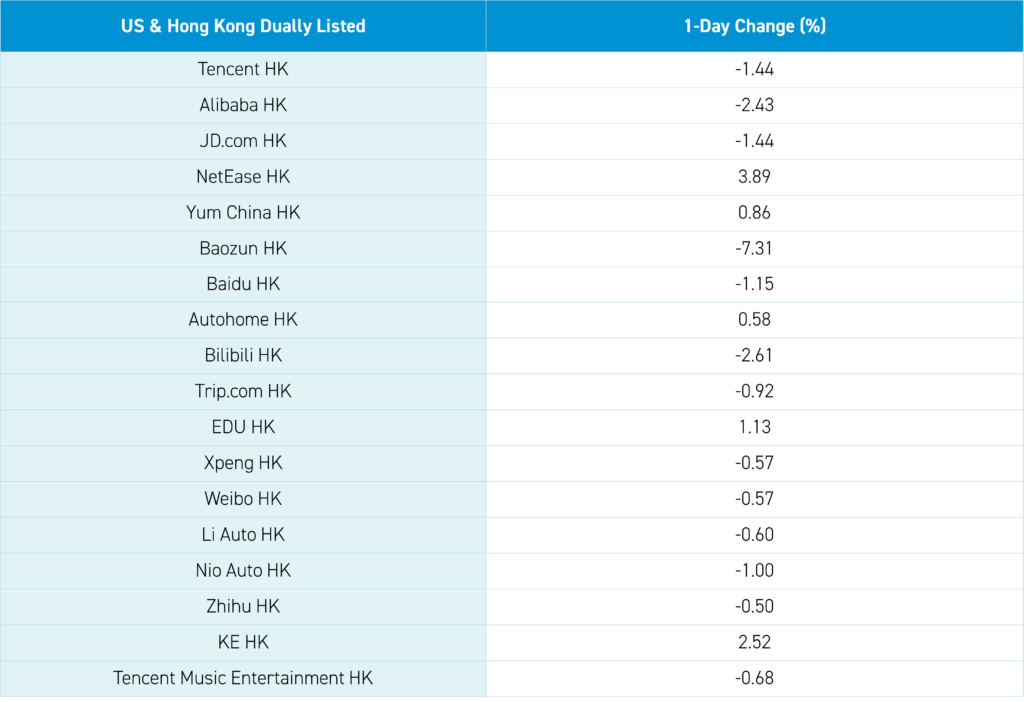

Hong Kong also had strong net buying via Southbound Stock Connect with Tencent, and the Hong Kong Tracker ETF saw large net buys. While Tencent’s unsponsored ADR fell -3.35% in US trading hours yesterday despite better than expected financial results, discussed further below, Tencent fell -1.44% in Hong Kong overnight as Hong Kong’s most heavily traded. Following Tencent, the most heavily traded by value were Alibaba -2.43% in advance of results this morning, Meituan +0.29%, ICBC +2%, and China Mobile +1.37%. NetEase +3.89% on Tencent’s positive comments on online gaming revenue while the media’s taking Tencent’s economic remarks out of context weighed on e-commerce/consumer plays like JD.com -1.44%, Trip.com -0.92%, Bilibili -2.61%, and Baidu -1.15%.

Tencent’s Unsponsored ADR fell after posting results that were better than expected yesterday. Tencent’s primary listing is in Hong Kong while the US ADR has very light volume in comparison as the Hong Kong stock trades in US dollar is $772 million versus the US ADR trading $101 million. Headlines blared about “macro pain” as their FinTech unit’s revenue growth slowed, which weighed on E-Commerce names during US trading hours. The headlines are slightly detached from what the company said, as the media cherry-picked the negatives while completely ignoring the positives. I find this blatant negative bias disconcerting at best or an outright lie. Read what management said below and decide for yourself.

Chief Strategy Officer James Mitchell stated, “And as a result of that, we have seen the government actually rolling out very proactive policies to encourage consumption. And we felt with these rollouts of such policies, at some point in time the consumer sentiment as well as the economy will start turning. Because, as evidenced in the wealth management service, it's not as like people don't have money. People actually sort of have money, but they choose to save rather than spend. And, if the government policies can actually induce more confidence among the consumers and start revitalizing different parts of the economy that we felt at some point in time consumer sentiment would turn and that would be good for our FinTech business.”

President Martin Lau stated, “In terms of macro, I would say what we saw is actually pretty consistent with the official consumption number, which is -- the second quarter is actually a slowdown from the first quarter. So I think that's the current trend we felt with the government rolling out more proactive policies and more expansionary policies than over time, given the resilience of the overall industry, as well as entrepreneurial environment in China, then we should over time see recovery in terms of the economy as well as consumer consumption. So that's what we believe in. But you know, whether at what time -- it's not a matter of whether, it's a matter of when. And we just sort of have to wait a little bit to see when the policies would actually start yielding results.”

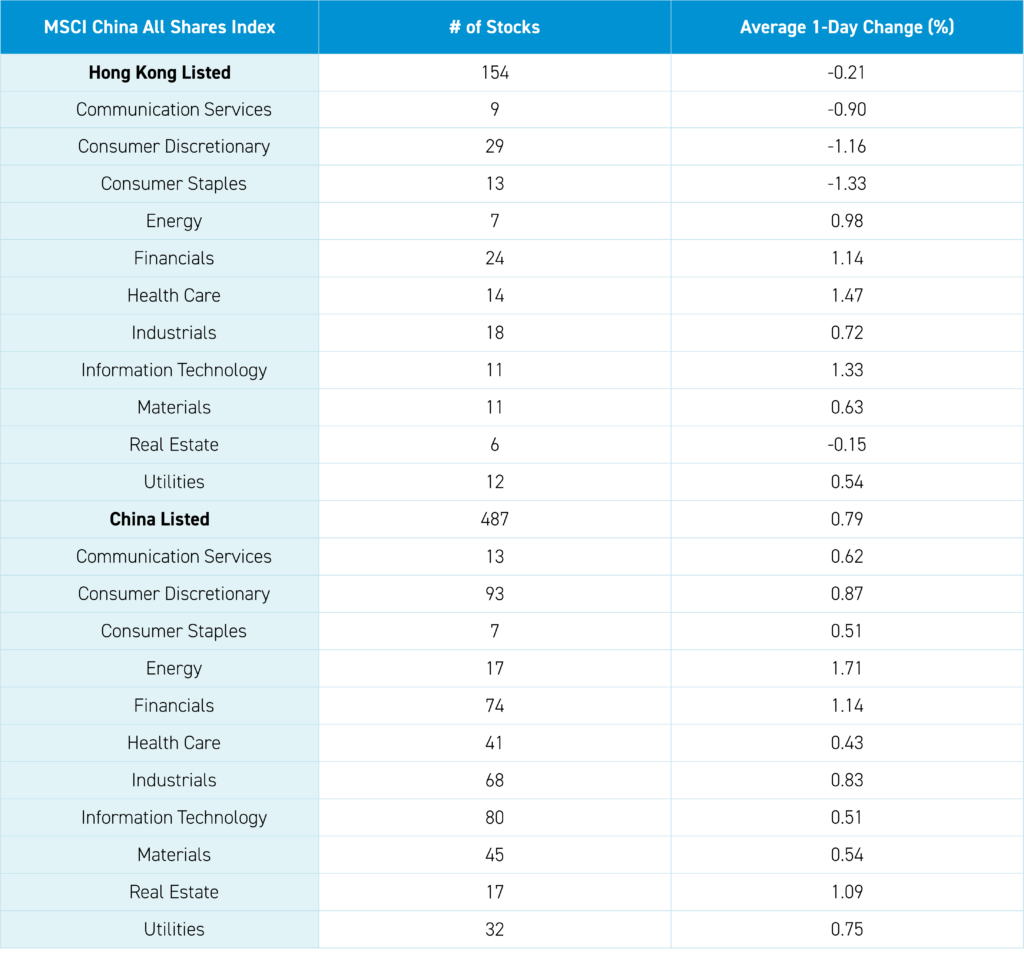

The Hang Seng and Hang Seng Tech indexes fell -0.02% and -0.33%, respectively, on volume +29.23% from yesterday, which is 86% of the 1-year average. 263 stocks advanced, while 190 declined. Main Board short turnover increased +61%, which is 91% of the 1-year average, as 18% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Large caps and value fell less than small caps and growth. The top-performing sectors were Health Care, which gained +1..47%, Technology, which gained +1.33%, and Financials, which gained +1.14%. Meanwhile, Consumer Staples fell -1.33%, Consumer Discretionary fell -1.16%, and Communication Services fell -0.9%. The top-performing subsectors were telecom services, banks, and technical hardware. Meanwhile, retail, software, and food/beverages/tobacco were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a healthy $851 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF and Tencent, which were large net buys.

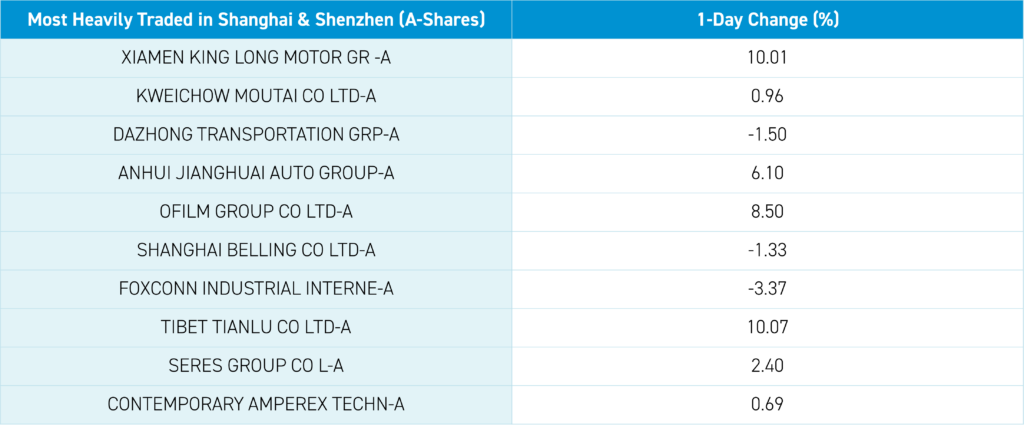

Shanghai, Shenzhen, and the STAR Board gained +0.94%, +0.82%, and +0.94% on volume that increased +24.06% from yesterday, which is 91% of the 1-year average. 2,549 stocks advanced, while 1,337 declined. Value and large caps outperformed growth and small caps. All sectors were positive, including Energy, which gained +1.72%, Financials, which gained +1.15%, and Real Estate, which gained +1.11%. The top-performing subsectors were internet, coal, and construction machinery. Meanwhile, motorcycles, daily chemicals, and business services were among the worst-performing. Northbound Stock Connect volumes were light as foreign investors were large buyers of Mainland stocks, including Ping An, China Merchants Bank, and CITIC Securities, which were moderate/light net buys. Meanwhile, East Money was a moderate net sell, Midea Group was a moderate/small net sell, and Foxconn a small net sell. CNY and the Asia Dollar Index fell versus the US dollar. The Treasury curve flattened. Copper gained while steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.15 versus 7.14 yesterday

- CNY per EUR 7.88 versus 7.87 yesterday

- Yield on 10-Year Government Bond 2.20% versus 2.19% yesterday

- Yield on 10-Year China Development Bank Bond 2.27% versus 2.24% yesterday

- Copper Price: +0.29%

- Steel Price: -0.77%