Monetary Policy Bazooka Unleashed

4 Min. Read Time

China Central Bank Meeting Overview

At 9 a.m., the People's Bank of China (PBOC) Governor Pan Gongsheng led a press conference along with China Securities Regulatory Commission (CSRC) Chairman Wu Qing and State Administration for Financial Regulation’s head Li Yunze. They announced the following:

- Banks' Reserve Requirement Ratio (RRR) will be reduced by 0.5%, with another cut of 0.25% to 0.5% “at an appropriate time.” This move effectively gives banks another RMB 1 trillion to lend.

- The 7-day reverse repo rate was lowered by 0.20% to 1.50%. This rate determines the medium-term lending facility and bank deposit rate.

- Existing mortgages were reduced by 0.50%, which will “…benefit 50 million households," which represents approximately 150 million people, "and the total annual interest expense per household will be reduced by about 150 billion yuan.”

- The minimum down payment ratio for first and second mortgages was reduced by 15%. He also reiterated that the PBOC created a RMB 300 billion fund to support affordable housing in May.

- RMB 500 billion, with more provided “depending on the future situation,” will be provided to brokerage houses, mutual funds, and insurance companies to buy Mainland-listed stocks through ETFs and large-cap stocks.

- “Guide commercial banks to provide loans to listed companies and major shareholders for repurchasing and increasing holdings of listed company stocks” at a rate of 1.75% interest.

- Increase Tier 1 capital for the six large banks.

- Other measures mentioned included encouraging mergers and acquisitions, promoting long-term capital in the markets, supporting private equity, optimizing the policy of renewing loans for small and medium enterprises, and encouraging venture capital.

Key Observations

- Is this the policy bazooka? It's pretty close.

- The press conference was held at 9 a.m. to ensure investors were aware it was taking place. The PBOC Governor’s speech was straight to the point, outlining in detail what was going to be done.

- The stock market did not really react until the stock market support fund was announced.

- While many banks have cut their China GDP forecast below 5%, the Chinese government has not.

- This represents a clear indication that the Mainland market’s decline is not going to be tolerated.

- Real estate policy support is like turning a supertanker. The mortgage and down payment will help, though it will take time. IT will be important to see how consumers react.

- Will we see more fiscal policy? I believe we will, as indicated by yesterday’s National Development and Reform Commission (NDRC) release on supporting automobile and home appliance purchasing.

- The move comes against a backdrop of very low China equity ownership. The move, just prior to quarter end, will put pressure on managers to allocate. I’ve been shocked at how low China allocations remain amongst US institutional investors.

- Remember how pundits said China wouldn’t make any big policy moves before the US election? WRONG. I don’t think they care who wins.

- It is too early to know whether Hong Kong or Mainland China stocks will benefit more.

Key News

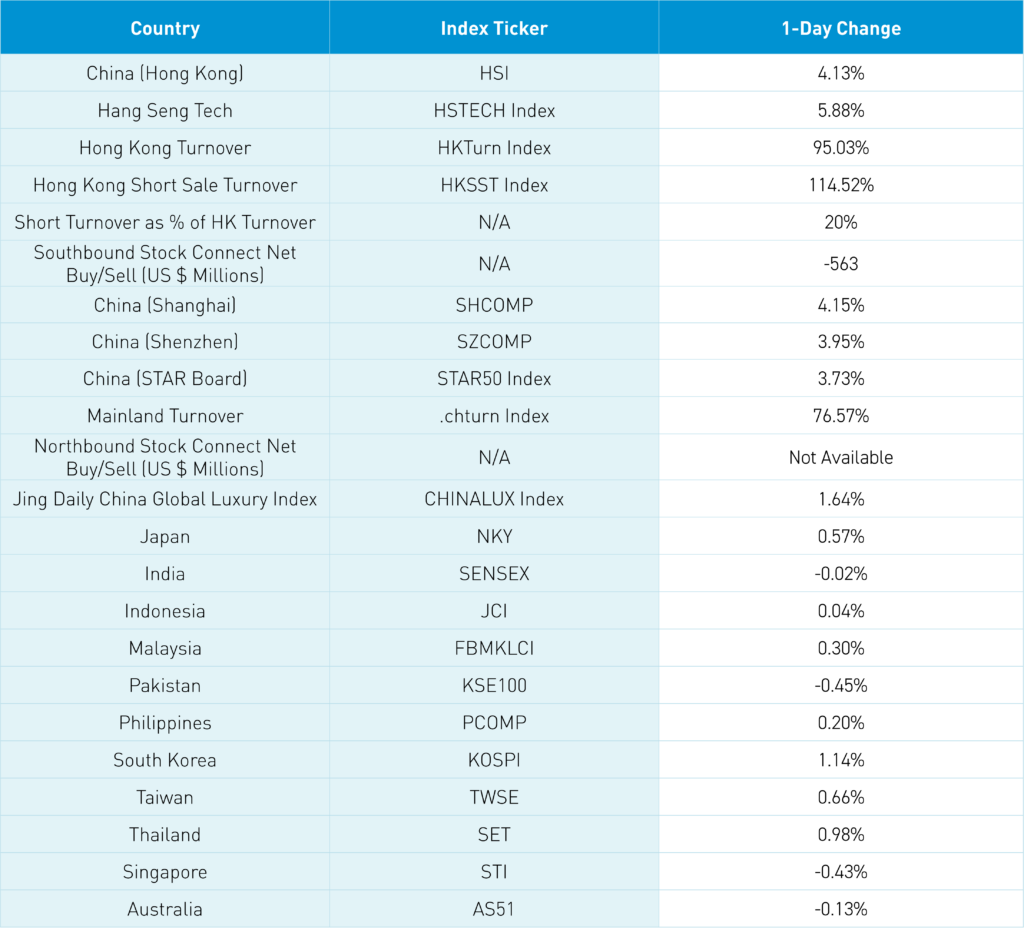

Asian stock markets were largely higher, with Hong Kong and Mainland China outperforming on MASSIVE volumes.

Hong Kong's volume reached 236% higher than the 1-year average volume, while Mainland China reached 124% higher than the 1-year average volume, along with extremely high advancers versus decliners.

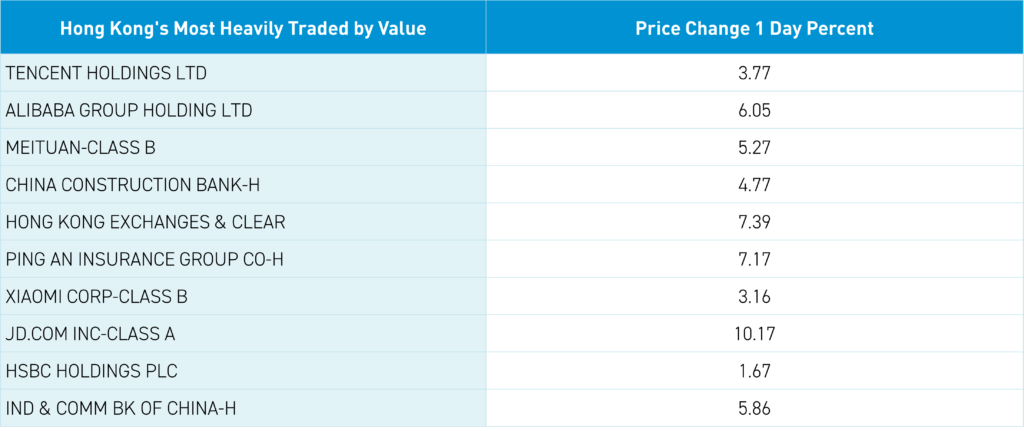

There were very broad rallies as the stimulus has a little something for everyone as brokers will benefit from the equity support. Yes, Southbound Stock Connect was a net sell, as the Hong Kong Tracker ETF was a large net sell, though their market timing track record is awful. Alibaba was another net buy via Southbound Stock Connect with $393 million of net buying, bringing the total to $3.807 billion since being added on September 10th. Tencent bought 2.53 million shares today as their buyback rolls on. All in all, it was a very strong day, as the numbers speak for themselves.

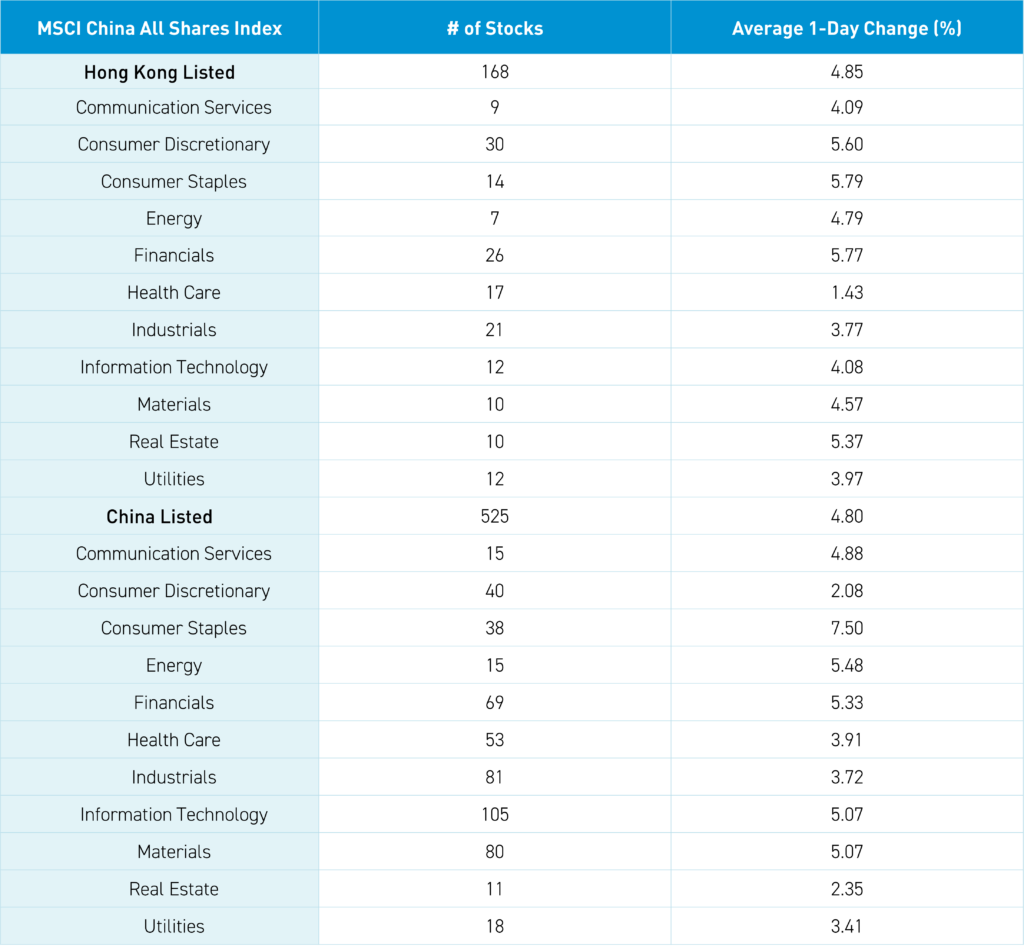

The Hang Seng and Hang Seng Tech indexes ripped higher by +4.13% and +5.88%, respectively, on volume that increased +95% from yesterday, which is 236% higher than the 1-year average. 463 stocks advanced, while 48 declined. Main Board short turnover increased by +115% from yesterday, which is 277% of the 1-year average, as 20% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth stocks outpaced value stocks, while large and small capitalization stocks were up approximately the same. All sectors were positive, led by consumer staples, up +5.79%, financials, up 5.77%, and consumer discretionary, up +5.61%. All subsectors were positive, led by media, diversified financials, and retailing. Southbound Stock Connect volumes were very high as Mainland investors sold -$563 million of Hong Kong stocks and ETFs, with Alibaba another large net buy, Hong Kong Exchanges a moderate/large net buy, and Miniso, a small net buy, while the Hong Kong Tracker ETF was a large net sell, Meituan and Tencent moderate/large net sells.

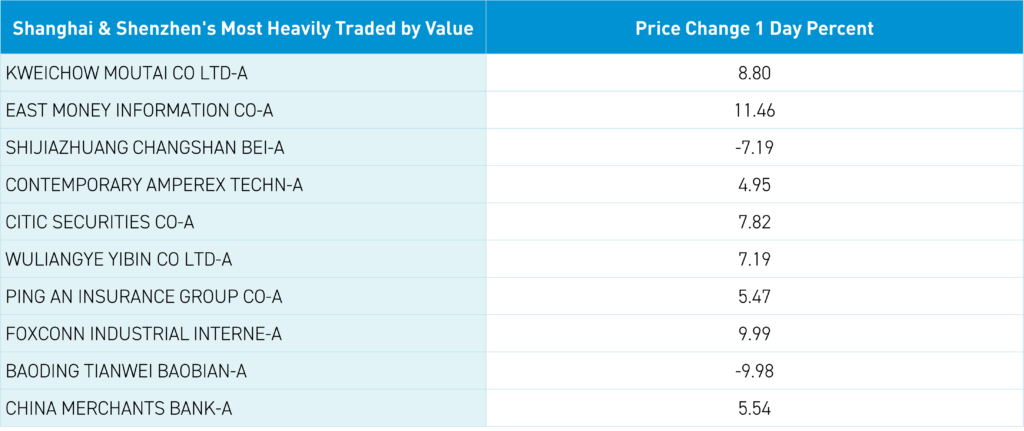

Shanghai, Shenzhen, and the STAR Board gained +4.15%, 3.95%, and +3.73%, respectively, on volume that increased +75% from yesterday, which is 124% of the 1-year average. 4,876 stocks advanced, while 191 stocks declined. Growth stocks outpaced value stocks, while large and small capitalization stocks were up approximately the same. All sectors were positive, led by consumer staples, up +7.5%, energy, up +5.49%, and financials, up +5.33%. The top-performing subsectors were diversified financials, liquor, and brokerage firms, while motorcycle manufacturing was the only negative subsector. Northbound Stock Connect volumes were very high. CNY and the Asia Dollar Index gained. Treasury bonds fell (yields rose). Copper and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.03 versus 7.06 yesterday

- CNY per EUR 7.83 versus 7.84 yesterday

- Yield on 10-Year Government Bond 2.07% versus 2.03% yesterday

- Yield on 10-Year China Development Bank Bond 2.15% versus 2.12% yesterday

- Copper Price +0.93%

- Steel Price +1.09%