Services PMI Beats As Premier Li Signals Economic Policy Support

3 Min. Read Time

Key News

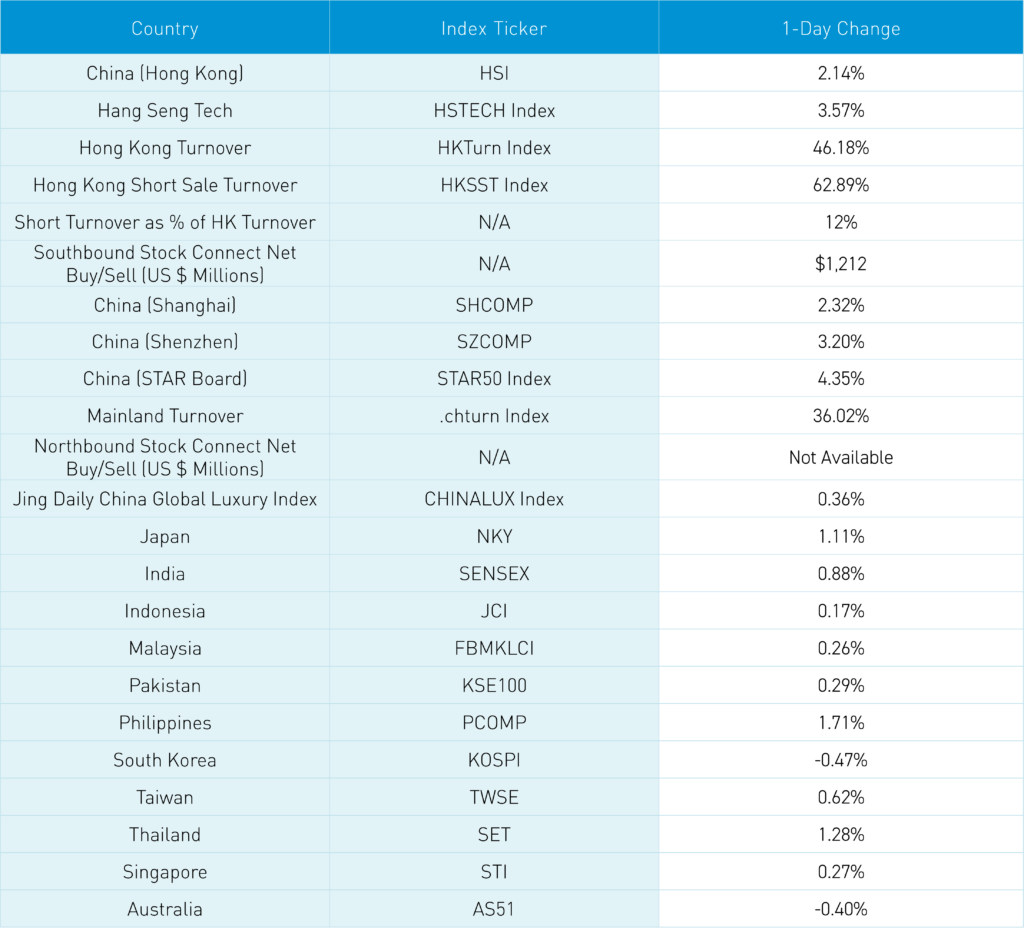

Asian equities had a strong day as Hong Kong and Mainland China significantly outperformed the region, while Japan, the Philippines, and Thailand had good days, and South Korea underperformed.

Starting with today’s macroeconomic tailwinds, though, we’ll get into the microeconomic/stock-specific movers. Yesterday, we wrote about the NPC agenda item on addressing local government’s hidden debts, though that clearly was released after the close as it was front page news going into Tuesday trading. Further positive news came from the mid-morning release of the Caixin Services October PMI, which rose to 53 from September’s 50.3, beating economist expectations of 50.5. As a diffusion index, readings above 50 translate to positive month-over-month improvement. S&P Dow Jones conducts the Caixin survey, so don’t buy into the “they just make the number up” nonsense.

Hat tip to my colleague Fernando for pointing out that the Citi China Economic Surprise Index rebounded back into positive territory after a strong improvement since the start of stimulus in late September. Premier Li added to the day’s enthusiasm following his keynote speech at the China International Import Expo in Shanghai, attended by 3,500 exhibitors from 152 countries, according to Reuters, where he stated the government had “ample space for fiscal policy and monetary policy” while reiterating the opening up to foreign investors and the 2024 GDP target of “around 5%”. We’ve heard that Premier Li, the pro-business former Secretary of Shanghai, is taking a larger role in the day-to-day economic policy.

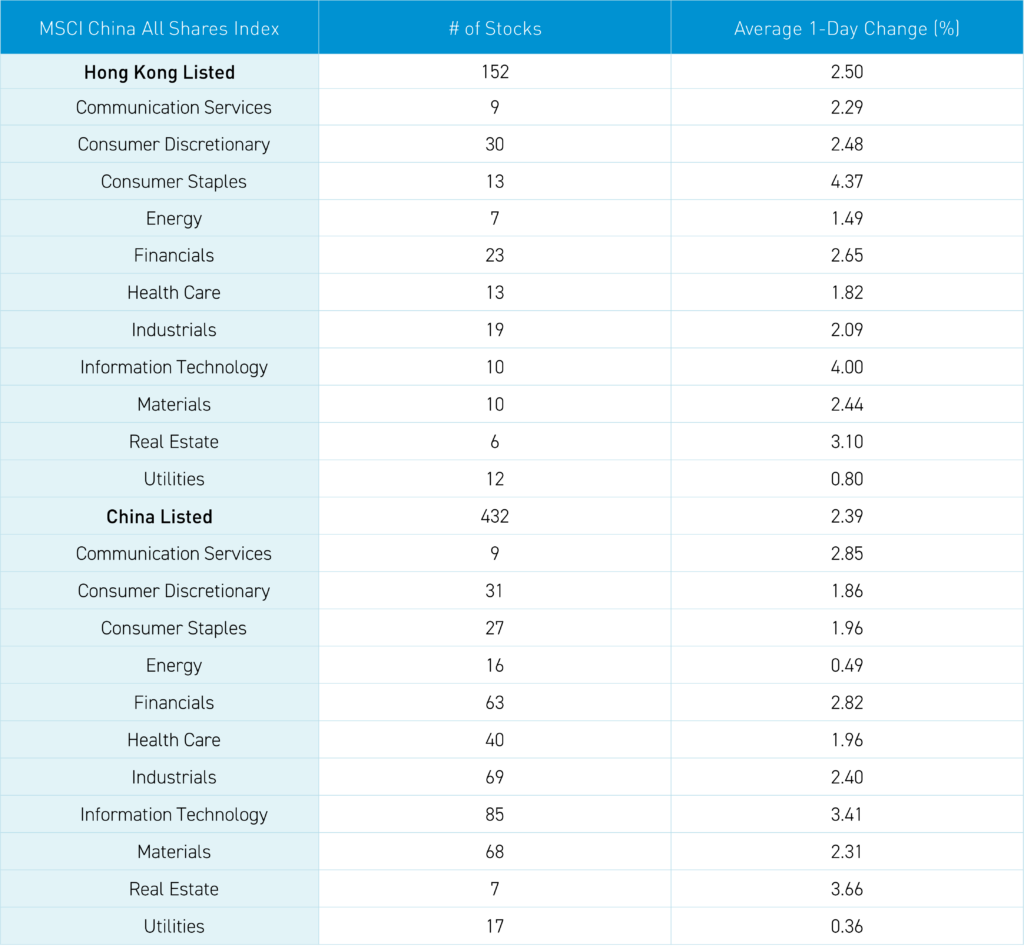

Coincidentally, today is the sixth anniversary of the Shanghai Stock Exchange’s growth stock STAR Board, which Premier Li was instrumental in creating, as it rose by +4.35% overnight. Mainland investors plowed money into Hong Kong stocks and ETFs with a healthy $1.21 billion of net buying via Southbound Stock Connect. Southbound Connect trading accounted for nearly 50% of Hong Kong trading by value. It was a strong day in both Mainland China and Hong Kong, marked by high volumes as all sectors were positive. There was strong breath/advancers beating decliners led higher by growth stocks/sectors, including the insurance sector post-China Life results and diversified finance/brokers.

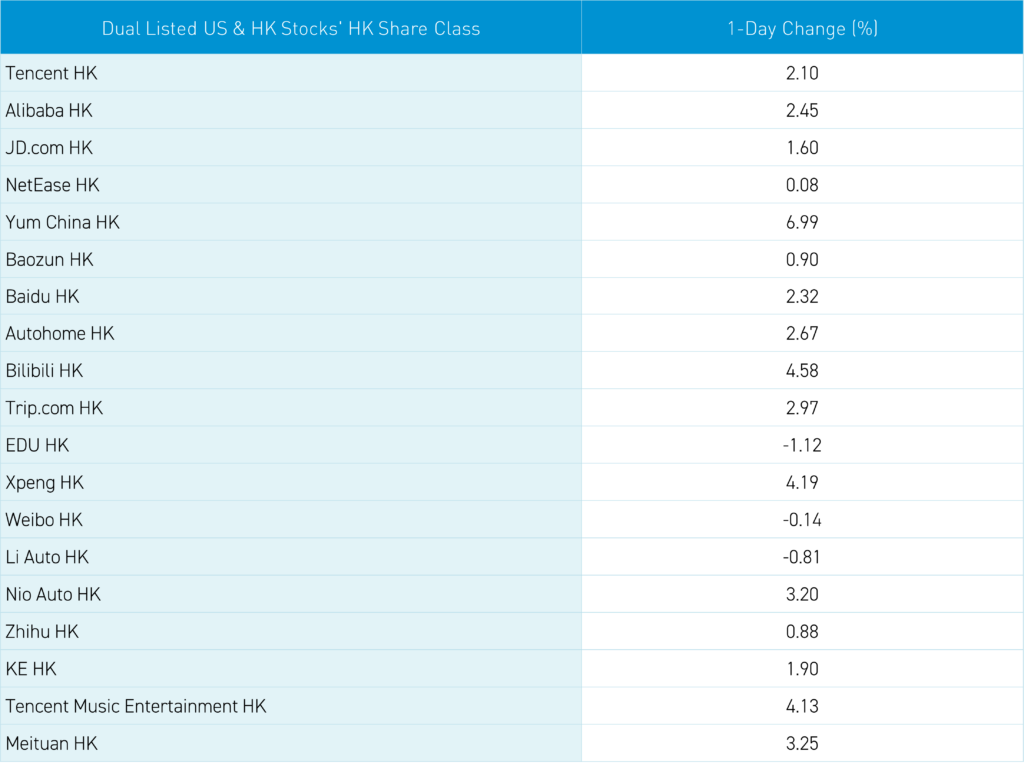

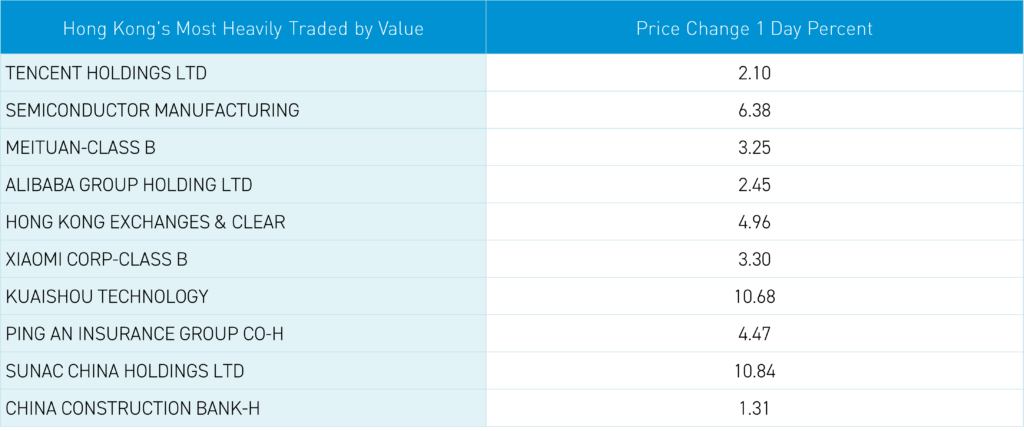

Today, Yum China’s Hong Kong share class rose by +6.99% following their strong Q3 results reported yesterday. Kuaishou jumped by +10.68% after announcing they will offer e-commerce in Brazil, as I suspect some shorts have a tire tread on their backs (i.e., run over). Apple suppliers were higher following chatter that the company will offer glasses similar to Meta’s Ray Ban collaboration. While the world is focused on the US Presidential election, though I would argue who takes the House and Senate is just as important, China’s economy and stock market are grinding higher with little attention. What attention China does get is always negative from Western media. Today’s Mainland market resilience and strong flows into Hong Kong from Mainland China should give investors something to think about, i.e.; I wouldn’t be short as maybe they plow money into the market post-US election results.

The Hang Seng and Hang Seng Tech gained +2.14% and +3.57%, respectively, on volume up +46.18% from yesterday, which is 138% of the 1-year average. 442 stocks advanced, while 62 declined. Main Board short turnover increased by +62.89% from yesterday, which is 102% of the 1-year average, as 12% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small capitalization stocks gained more than value and large capitalization stocks. All sectors were positive, led by consumer staples, up +4.37%, technology, up +4.01%, and real estate, up +3.10%. All sub-sectors closed higher, led by diversified financials, semiconductors, and food/beverages. Southbound Stock Connect volumes were 1.5X the average as Mainland investors bought $1.21 billion of Hong Kong stocks and ETFs, as the Hong Kong Tracker ETF was a large net buy, Tencent and Meituan were moderate net buys, Kuaishou and Xiaomi were small net buys, while Sunac was a large net sell, and SMIC, CNOOC, and SH Electric were small net sells.

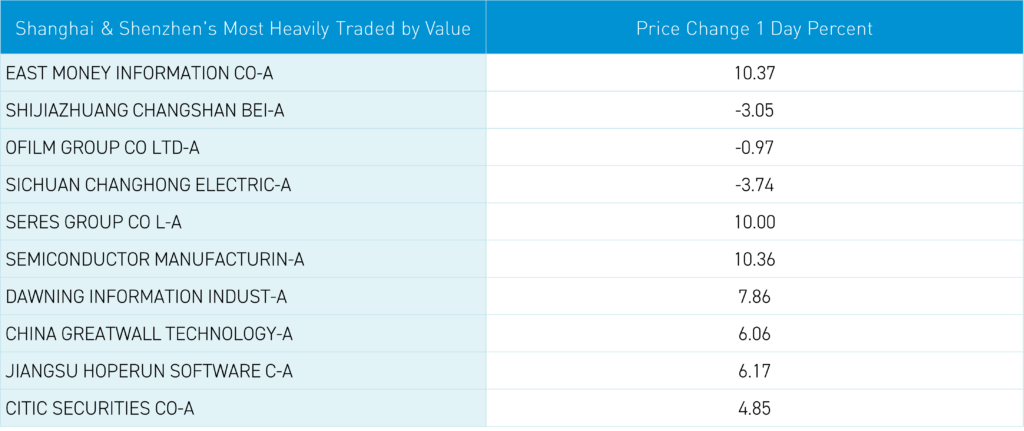

Shanghai, Shenzhen, and the STAR Board gained +2.32%, +3.20%, and +4.36%, respectively, on volume up +36.02% from yesterday, which is 257% of the 1-year average. 4,820 stocks advanced, while 236 declined. Growth and small capitalization stocks rose more than value and large capitalization stocks. All sectors were positive, led higher by real estate, up +3.66%, technology, up +3.42%, and communication services, up +2.85%. All sub-sectors were positive, led higher by aerospace/military, software, and securities. Northbound Stock Connect volumes were high, 2X the average. CNY and the Asia dollar index gained versus the US dollar. Treasury bonds rallied. Copper and steel both rose.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.10 versus 7.10 yesterday

- CNY per EUR 7.74 versus 7.74 yesterday

- Yield on 10-Year Government Bond 2.11% versus 2.13% yesterday

- Yield on 10-Year China Development Bank Bond 2.19% versus 2.21% yesterday

- Copper Price +0.58%

- Steel Price +1.21%