Trip.com Beats Analyst Expectations

2 Min. Read Time

Trip.com Earnings Overview

Trip.com (TCOM US, 9961 HK) reported Q3 2024 financial results after the US close that beat analyst expectations. Executive Chairman and Co-founder James Jianzhang Liang stated, “In the third quarter of 2024, the China travel market demonstrated remarkable resilience with strong performance in both domestic and cross-border travel. This surge in demand reflects a recovery in consumer confidence and a growing enthusiasm for travel.” When asked if recent stimulus measures boosted travel spending, CFO Cindy Xiaofan Wang responded, “It may be too early to determine the direct impact of the recent stimulus measures, but a healthy economic environment should benefit all industries, including travel.”

- Revenue increased by 16% to RMB 14.75 billion ($2.26 billion) versus estimates of RMB 15.6 billion and Q3 2023’s RMB 13.7 billion.

- Adjusted net income was RMB 5.96 billion ($847 million) versus estimates of RMB 4.7 billion and Q3 2023’s RMB 4.9 billion.

- Adjusted EPS was RMB 8.75 ($1.25) versus estimates of RMB 7 and Q3 2023’s RMB 7.26.

- Cash and cash equivalents on the balance sheet were RMB 86.9 billion ($12.4 billion).

Key News

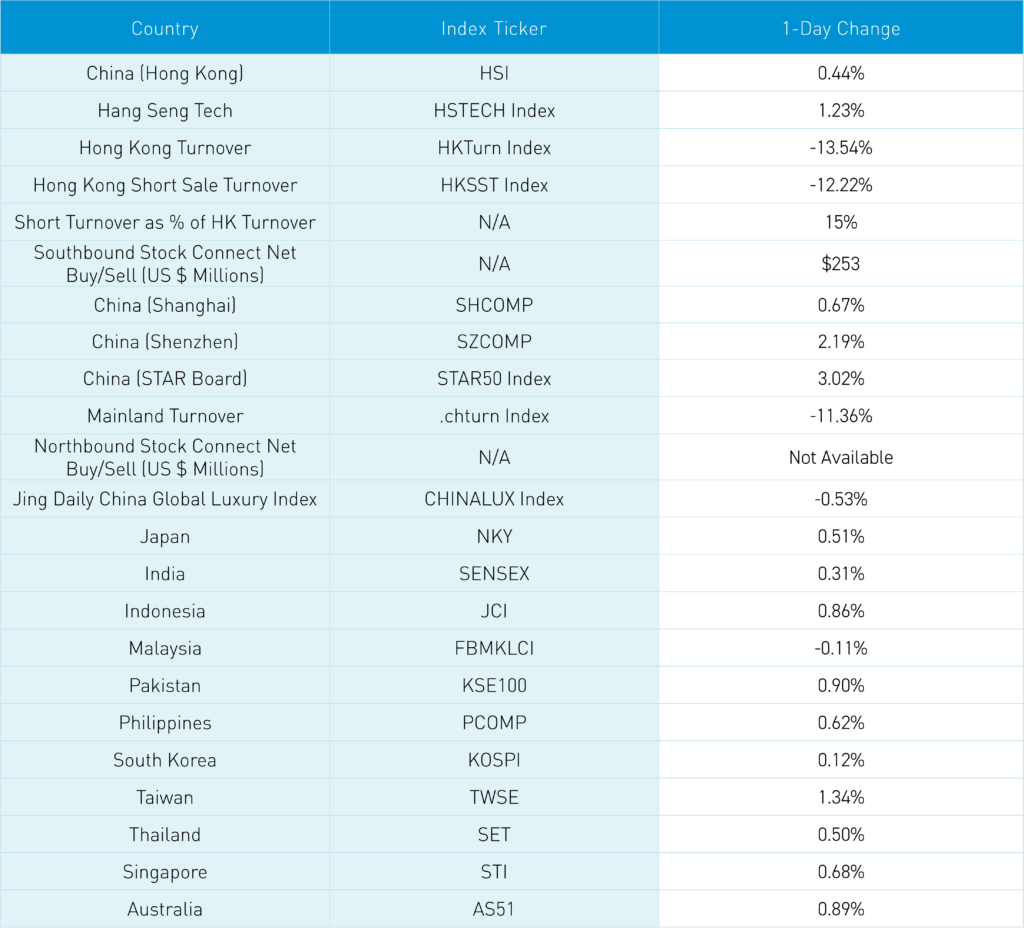

Asian equities showed strength overnight as Hong Kong and Mainland China outperformed.

Yesterday, we discussed why President Trump’s threat of 60% tariffs is unlikely to become a reality, as replicating the ingredients of the Great Depression seems ill-advised. Another factor that might be weighing on investors is the delisting of US-listed Chinese ADRs. President Trump delisted three Chinese telecom ADRs following his first reelection loss in a disorderly, haphazard process that likely hurt individual investors who, unlike institutional investors, were unable to convert these US ADRs into Hong Kong shares. There has been no introduction of ADR legislation, nor is there any indication ADR delisting is a topic. Similar to the approach that China tariffs only weigh on China, would a pro-Wall Street policy include anti-investment banking and trading policy? We will monitor the situation and keep you posted, but there is nothing to indicate that ADR delisting will occur.

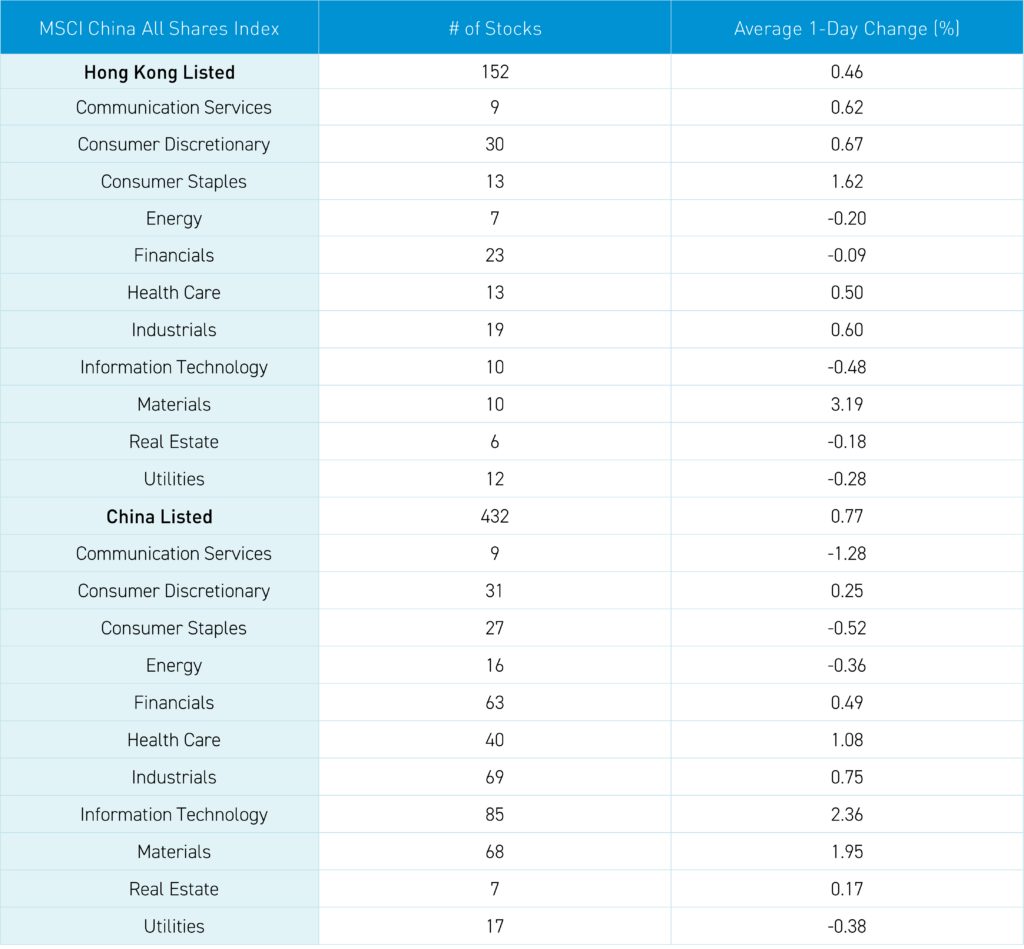

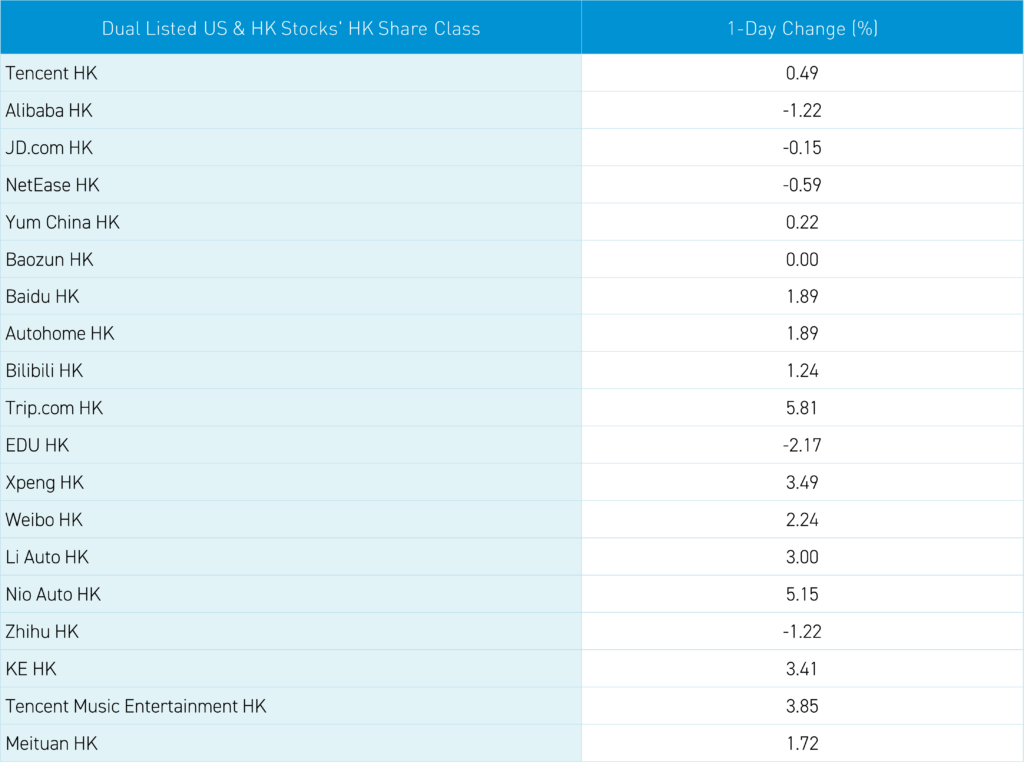

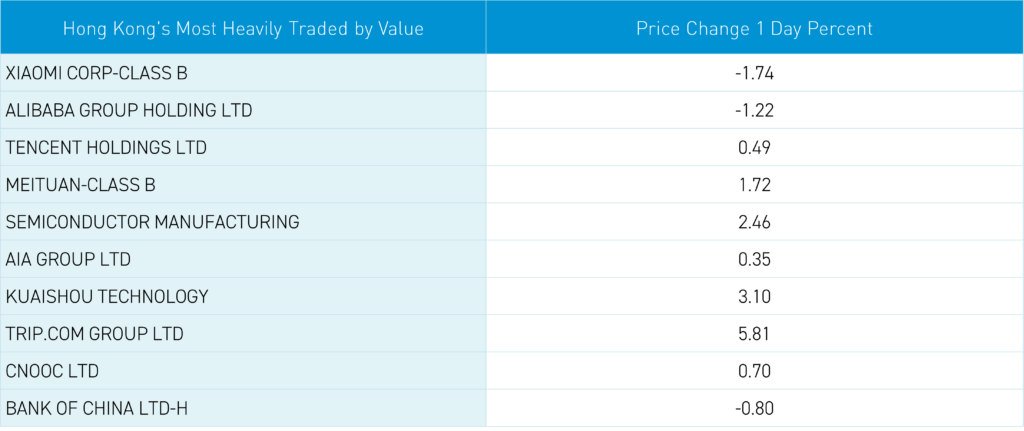

The Hang Seng and Hang Seng Tech gained +0.44% and +1.23%, respectively, on volume down -13.54% from yesterday, which is 96% of the 1-year average. 330 stocks advanced, while 143 declined. Main Board short turnover declined by -12.22% from yesterday, which is 93% of the 1-year average, as 15% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small capitalization stocks outperformed value and large capitalization stocks. The top sectors were materials, up +3.18%, consumer staples, up +1.61%, and consumer discretionary, up +0.66%, while technology fell -0.48%, utilities fell -0.28%, and energy fell -0.21%. The top sub-sectors were materials, media, and semiconductors, while business/professional services, household products, and technical hardware were the worst. Southbound Stock Connect volumes were 1.5X pre-stimulus average as Mainland investors bought $253 million of Hong Kong stocks and ETFs, with Tencent a large net buy, Meituan a moderate net buy, XPeng, Xiaomi, Alibaba, and CNOOC small net buys, the Hong Kong ETF Tracker a large net sell, and SMIC a moderate net sell.

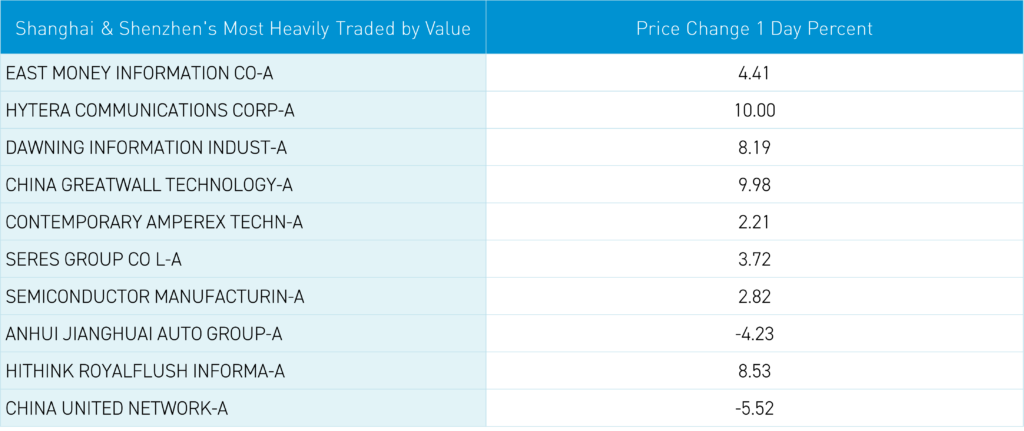

Shanghai, Shenzhen, and the STAR Board gained +0.67%, +2.19%, and +3.02%, respectively, on volume down -11.36% from yesterday, which is 164% of the 1-year average. 4,461 stocks advanced, while 574 declined. Growth and large capitalization stocks outpaced value and small capitalization stocks. The top sectors were technology, up +2.37%, materials, up +1.96%, and healthcare, up +1.09%, while communication services fell -1.27%, consumer staples fell -0.54%, and utilities fell -0.38%. The top sub-sectors were computer hardware, fine chemicals, and industrial machinery, while telecommunication, construction, and automobiles were the worst. Northbound Stock Connect volumes were 2X pre-stimulus levels. Treasury bonds rallied. CNY and the Asia dollar index were basically flat versus the US dollar. Steel and copper rose

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY per EUR 7.64 versus 7.65 yesterday

- Yield on 10-Year Government Bond 2.09% versus 2.11% yesterday

- Yield on 10-Year China Development Bank Bond 2.16% versus 2.17% yesterday

- Copper Price +0.27%

- Steel Price +0.89%