PMIs, Vehicle Sales, & Real Estate Sales Rebound In November

7 Min. Read Time

Key News

Asian equities had a strong day despite a very strong US dollar overnight, as Taiwan, the Philippines, and Pakistan outperformed, and South Korea underperformed again, as the KOSPI and growth-focused KOSDAQ are now off -15% and -28% year-to-date (YTD).

I have not seen any calls for Emerging Markets ex South Korea, though it is giving the FTSE EM index an edge over the MSCI EM index due to the former’s upgrade of South Korea to developed market status.

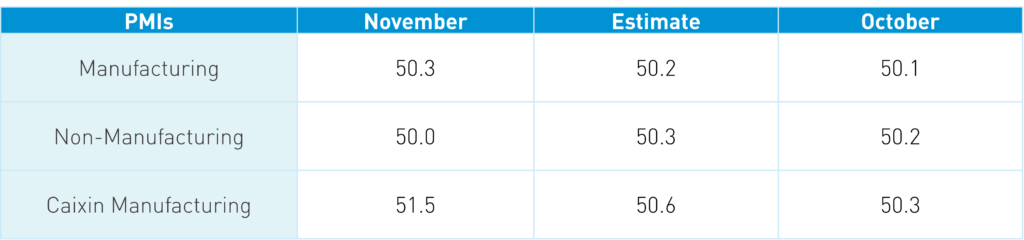

Hong Kong and Mainland China had strong sessions, led by growth stocks following better-than-expected purchasing managers’ indexes (PMIs), November auto sales, and November real estate sales. There was also continued chatter that the Politburo and the China Economic Work Conference (CEWC) will take place earlier than historically. The previously telegraphed US government export semiconductor restrictions were a non-event.

PMI releases were a catalyst and were not driven by tariff front-running as export orders remained below 50, which indicates contraction month-over-month.

Meituan was Hong Kong’s most heavily traded stock by value, falling only -0.77% versus its thinly traded unsponsored ADR, which fell -7.42% on Friday after beating Q3 estimates with revenues up +22% YoY but a conservative Q4. So far this year, Meituan’s Hong Kong stock is up +106%, so there was likely some profit taking place overnight.

Discount retail chain MINISIO gained +18.22% versus a gain of only +8.22% for its US listing on Friday, another validation of our preference for Hong Kong shares over US-listings (ADRs).

Consumption plays, including internet stocks, performed well in Hong Kong and Mainland China, as the Shanghai and Guangzhou governments both issued consumption vouchers to “activate market vitality and boost consumer confidence”.

According to the CRIC Research Center, the big four Tier 1 cities and top 30 cities saw November square meter sales increase 5% and 3%, respectively, from October and 57% and 20%, respectively, year-over-year. This is leading to a pick-up in land sales, though lower-tier cities continue to exhibit sluggish sales.

November new energy vehicle (NEV) sales, which include both electric vehicles and hybrids, were strong, led by BYD’s 506,804 units (BYD gained +2.44%). Meanwhile, Li Auto sold 48,740 units, which is down -5.25% from October (Li Auto fell -2.58%), Xpeng sold 30,895 units (Xpeng gained +5.06%), and NIO sold 20,575 units (NIO gained +2.92%). Also helping the auto subsector was Guangzhou Auto, which gained +25.17% after announcing an electric vehicle partnership with Huawei.

Hong Kong had a very healthy $2.53 billion worth of net inflow, predominantly into the Hong Kong Tracker ETF, from Mainland investors. 51% of Hong Kong's turnover was due to Southbound Connect trading. While Hong Kong had a strong day, Mainland China stocks arguably had a stronger day than Hong Kong stocks, despite China’s Treasury bonds rallying to all-time high prices.

PBOC Governor Pan Gongsheng spoke at a conference, saying the central bank would support the economy, as usual.

Jiangxi and Shandong providences reported refinancing RMB 55.1 billion and RMB 12.9 billion worth of hidden debt, respectively. National Team ETFs had below-average volumes, indicating domestic investors continue to come back into the market.

This weekend’s Wall Street Journal had a good article on Lei Zhang, a China native who attended Yale, worked for David Swensen in the endowment office, and co-founded the private equity firm Hillhouse Capital, which is known for its early-days China internet investments. Other than the article title calling the 52-year-old a “whiz kid”, it is a worthwhile read as it highlights the political pressure on US investors in China today, in addition to internet regulation’s impact on foreign investor confidence and resulting poor performance.

Just last week, Texas governor Greg Abbott reiterated that state agencies should not invest in China, despite the irony that the state of Texas now exports the most to China of any US state, mostly oil and gas.

While US investors might be sidelined, the Wall Street Journal’s article notes that Hillhouse itself has been focused on raising money from “the Middle East and Asia”, which is evidence of our China re-rating thesis. This is the idea that capital flowing back into China will begin with local capital, followed by Asian investors. For these investors, China’s economy is not going anywhere and, if anything, has only grown more important in recent years.

I asked an American CEO and entrepreneur based in Beijing about Trump’s tariffs last week. He responded by saying asking, “Who cares?” and pointing out that the US now represents only 13% of China’s exports.

The Hang Seng and Hang Seng Tech indexes diverged to close +0.65% and +1.20%, respectively, on volume that increased +9% from Friday, which is 113% of the 1-year average. 350 stocks advanced, while 135 stocks declined. Main Board short turnover increased by +47% from Friday, which is 149% of the 1-year average, as 20% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and small caps. The top-performing sectors were Information Technology, which gained +2.76%; Consume Staples, which gained +2.23%; and Industrials, which gained +1.47%. Meanwhile, the worst-performing sector was Energy, which fell -0.35%. The top-performing subsectors were food & beverage, electrical equipment, and steel. Meanwhile, industrial conglomerates and household products were among the worst-performing subsectors. Southbound Stock Connect volumes were very high as Mainland investors bought a very healthy $2.5 billion worth of Hong Kong-listed stocks and ETFs, including the HK Tracker ETF, the China Enterprise ETF, and Alibaba. Meanwhile, Xiaomi, CNOOC, Tencent, and MINISO were net sells.

Shanghai, Shenzhen, and the STAR Board rose +1.13%, +1.76%, and +0.83%, respectively, on volume that increased +5% from Friday, which is 182% of the 1-year average. 4,439 stocks advanced, while 616 stocks declined. The growth factor and small caps rose more than the value factor and large caps. The top-performing sectors were Consumer Discretionary, which gained +2.07%, Real Estate, which gained +1.53%, and Information Technology, which gained +0.97%. Meanwhile, the worst-performing sectors were Energy, which fell -0.64%; Financials, which fell -0.18%; and Consumer Staples, which fell -0.04%. The top-performing subsectors were the forest industry, autos, and retail. Meanwhile, banking, precious metals, and telecom were among the worst-performing subsectors. Northbound Stock Connect volumes were 1.5 above average. CNY and the Asia Dollar Index fell

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 0.7% |

| Hang Seng Tech | HSTECH Index | 1.2% |

| Hong Kong Turnover | HKTurn Index | 9.4% |

| HK Short Sale Turnover | HKSST Index | 49.4% |

| Short Turnover as a % of HK Turnovr | N/A | 20.3% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 1821.2 |

| China (Shanghai) | SHCOMP Index | 1.1% |

| China (Shenzhen) | SZCOMP Index | 1.8% |

| China (STAR Board) | Star50 Index | 0.8% |

| Mainland Turnover | .chturn Index | 4.7% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0.3% |

| Japan | NKY Index | 0.8% |

| India | SENSEX Index | 0.6% |

| Indonesia | JCI Index | -0.9% |

| Malaysia | FBMKLCI Index | 0.1% |

| Pakistan | KSE100 Index | 2% |

| Philippines | PCOMP Index | 2% |

| South Korea | KOSPI Index | -0.1% |

| Taiwan | TWSE Index | 2.1% |

| Thailand | SET Index | 0.7% |

| Singapore | STI Index | 0.3% |

| Australia | AS51 Index | 0.1% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 154 | 0.94 |

| Communication Services | 9 | 0.77 |

| Consumer Discretionary | 29 | 0.74 |

| Consumer Staples | 13 | 2.23 |

| Energy | 7 | -0.35 |

| Financials | 24 | 1.09 |

| Health Care | 14 | 0.31 |

| Industrials | 18 | 1.47 |

| Information Technology | 11 | 2.76 |

| Materials | 11 | 0.73 |

| Real Estate | 6 | 1.18 |

| Utilities | 12 | 0.18 |

| Mainland China Listed | 487 | 0.45 |

| Communication Services | 13 | 0.19 |

| Consumer Discretionary | 41 | 2.06 |

| Consumer Staples | 32 | -0.04 |

| Energy | 17 | -0.64 |

| Financials | 68 | -0.18 |

| Health Care | 45 | 0.37 |

| Industrials | 74 | 0.74 |

| Information Technology | 93 | 0.96 |

| Materials | 80 | 0.28 |

| Real Estate | 7 | 1.53 |

| Utilities | 17 | 0.67 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 0.5 |

| Alibaba HK | 9988 HK Equity | 0.4 |

| JD.com HK | 9618 HK Equity | 2.4 |

| NetEase HK | 9999 HK Equity | 2.8 |

| Yum China HK | 9987 HK Equity | 1.5 |

| Baozun HK | 9991 HK Equity | -1.9 |

| Baidu HK | 9888 HK Equity | 2 |

| Autohome HK | 2518 HK Equity | 3.4 |

| Bilibili HK | 9626 HK Equity | 3.8 |

| Trip.com HK | 9961 HK Equity | 0.4 |

| EDU HK | 9901 HK Equity | -0.5 |

| Xpeng HK | 9868 HK Equity | 5.1 |

| Weibo HK | 9898 HK Equity | 2.2 |

| Li Auto HK | 2015 HK Equity | -2.6 |

| Nio Auto HK | 9866 HK Equity | 2.9 |

| Zhihu HK | 2390 HK Equity | -2.1 |

| KE HK | 2423 HK Equity | -1.4 |

| Tencent Music Entertainment HK | 1698 HK Equity | 0.7 |

| Meituan HK | 3690 HK Equity | -0.8 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| MEITUAN-CLASS B | -0.8 |

| TENCENT HOLDINGS LTD | 0.5 |

| ALIBABA GROUP HOLDING LTD | 0.4 |

| XIAOMI CORP-CLASS B | 2.9 |

| MINISO GROUP HOLDING LTD | 18.2 |

| BYD ELECTRONIC INTL CO LTD | 11.3 |

| JD.COM INC-CLASS A | 2.4 |

| AIA GROUP LTD | -0.4 |

| BYD CO LTD-H | 2.4 |

| GEELY AUTOMOBILE HOLDINGS LT | 4 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| EAST MONEY INFORMATION CO-A | 0.7 |

| HITHINK ROYALFLUSH INFORMA-A | -2.6 |

| DAWNING INFORMATION INDUST-A | -1.2 |

| SHENZHEN YSSTECH INFO-TECH-A | -3.9 |

| SICHUAN DEVELOPMENT LOMON -A | 10 |

| SHANGHAI ELECTRIC GRP CO L-A | 10 |

| SICHUAN CHANGHONG ELECTRIC-A | 4.6 |

| 360 SECURITY TECHNOLOGY IN-A | -0.8 |

| BLUEFOCUS INTELLIGENT COMM-A | 1.4 |

| ZHEJIANG JINKE TOM CULTURE-A | 6 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.27 versus 7.24 Friday

- CNY per EUR 7.65 versus 7.64 Friday

- Yield on 10-Year Government Bond 1.98% versus 2.02% Friday

- Yield on 10-Year China Development Bank Bond 2.07% versus 2.11% Friday

- Copper Price -0.08%

- Steel Price -0.06%