NPC Preview, China Markets Shake Off Tariffs

9 Min. Read Time

Key News

Asian equities were largely lower, though not significantly lower, due to increased US tariffs on goods from Canada, Mexico, and China, as the US dollar weakened overnight.

Mainland China, Vietnam, and the Philippines posted positive returns, while Japan and Indonesia underperformed. The resilience of Mainland China and Hong Kong stocks through this has been noteworthy. Despite the clickbait apocalyptic headlines, China’s retaliation was quite light: 10% tariffs on soybeans, pork, beef, fruits, and vegetables, 15% tariffs on cotton, wheat, corn, and chickens, along with the addition of 15 companies I’ve never heard of to the export control list.

The US dollar was weaker versus most Asian currencies, including the Renminbi. Could we be witnessing the "Art of the Deal"? China's government responded to Trump's focus on fentanyl by releasing a white paper on their efforts to stem the flow of precursors into the United States and elsewhere. Arguably, the only positive thing Biden did with China was sign an agreement to stem the flow that China claims to have adhered to. Since no one can prove otherwise, why not blame them for not abiding by it? Or, is it an effort to throw them off-balance? We shall see.

Today’s catch-up with US Ambassador Terry Branstad could not be better timed. We will report back tomorrow!

BYD fell by -4.27% in Mainland China and -6.77% in Hong Kong. The stock was a significant drag on the markets after raising $5.5 billion by selling 129 million shares at a 7.8% discount compared to Monday’s closing price. The sale weighed on auto and battery stocks, including CATL, which fell by -3.85%. Interestingly, CATL is building a plant in Portugal, which begs the question, why don't they build one in the US?

Hong Kong and Mainland China energy stocks were lower on OPEC production increases while mega-cap banks were lower, which also weighed heavily on indices. Alibaba fell by -1.99% despite the company’s AI efforts receiving much attention in China. Our friend Matt pointed out that 6.89% of Alibaba’s outstanding shares are now held by Mainland investors via Southbound Stock Connect. Less those items, both markets were broadly higher, as internet names were higher, led by Tencent, which gained +1.61%, JD.com, which gained +0.75%, Trip.com, which gained +1.64%, and Baidu, which gained +1.74%, though Hong Kong volumes were light. Aerospace stocks were strong performers in Hong Kong and Mainland China as they were seen as beneficiaries of the US ceasing to fund Ukraine. For what it’s worth, China abstained from Russia and the US' United Nations vote on Ukraine. Mainland markets opened lower but grinded higher to close in the green, led by growth, technology, semiconductor, and small capitalization stocks. The National Team’s favorite ETFs had below-average volumes.

Ray Dalio’s recent interview on the threat of US government debt on the US economy received a lot of coverage in Chinese financial media. This follows yesterday's note on Warren Buffett criticizing US tariffs as investors wonder why he holds so much cash. We have long stated that an element of American exceptionalism/US equity outperformance is driven by foreign capital flowing into the US. The US dollar’s strength has only added to the appeal of US stocks because they are denominated in US dollars. The US dollar index is up +45% since bottoming in April 2011 giving US stocks a huge tailwind. Could an unintended consequence of the unpredictable Art of the Deal are foreign investors lightening up on US stocks? European stock performance has gotten a lot of attention though Asia has some good outperformers versus the S&P 500’s -0.54% YTD. Worth noting the US dollar index fell -0.81% on Monday and -0.83% this morning. I’m not rooting for US stocks to fall as, personally, I’m heavily invested. Hard not to notice one of the pillars of US stock outperformance might be cracking.

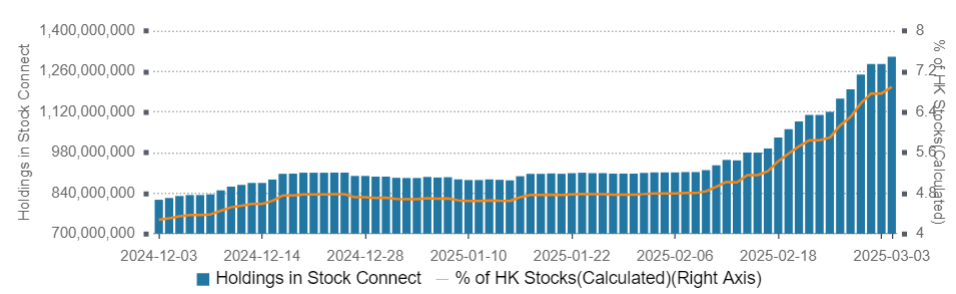

Alibaba Shares held via Southbound Stock Connect.

Below are targets for this week’s National People's Congress (NPC) with some commentary from yours truly. First a few key points:

- expectations are LOW (my kids would quote Flo Rida’s exceedingly catchy song Low) as many investors aren’t involved in Chinese equities or underweight (i.e. the pain trade is higher!)

- It is interesting that numerous US officials (Bessent, Yellen, Trump) have stated that more needs to be done to raise China’s domestic consumption. Could the Chinese government respond to US tariffs with a bigger than anticipated domestic consumption stimulus? I think there is a better than 50% chance, not because of US jawboning, but the Chinese economy needs support due to the real estate crisis. December’s China Economic Work Conference heavily emphasized consumption, giving a strong clue, just as President Xi's meeting with tech entrepreneurs/private sector was also a clue.

- A senior Chinese government official once stated, (paraphrasing) “We Chinese are not as direct as you Americans. We never tell you what we are thinking though we give subtle signs if you watching.”

I think it is time for some not-so-subtle policy stimulus! Below, I bolded the two most important numbers. There is one caveat, though. Several tranches of debt will be issued for banks, local governments and long term issuance. In aggregate, these could push the budget deficit to over 8%, though we do not yet know exactly where the debt issuance will be, so most are looking at the central government's budget deficit.

- GDP target: the market expects “around 5%”, which is the same as 2024. Anything above would be shocking.

- CPI Target: Market expectations are divided, as some people expect deflationary pressures to persist. A target of 2% would imply significant stimulus, as consumer prices barely budged in 2024.

- Official (Central Government) Budget Deficit: The market expects 4% versus 2024’s 3%. 3% would be disappointing, but 4% would be positive

- Budget Increase: The market expects RMB 2 trillion, per the above.

- Total Government Bond Issuance: The market expects a range from RMB 11 trillion to RMB 13 trillion.

- Special Government Ultra Long-Term Bond Issuance: The marker expects RMB 1.8 trillion to RMB 2 trillion, versus 2024’s RMB 1 trillion.

- Bank Net Capital Injection: The market expects RMB 500 billion.

- The key here will be how much of the increased bond issuance and fiscal expansion will be geared to consumption policies, such as the trade in subsidy

- Monetary Policy: The market expects “moderate easing” or “moderately loose”.

The Hang Seng and Hang Seng Tech indexes diverged to close -0.28% and 0.00% on volume that decreased -10.72% from yesterday, which is 175% of the 1-year average. 234 stocks advanced while 250 stocks declined. Main Board short turnover increased +13.45% from yesterday, which is 195% of the 1-year average, as 17% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps “outperformed” (i.e. fell less than) the growth factor and large caps. The top-performing sectors were Materials, which gained +1.7%, Communication Services, which gained +1.60%, and Consumer Staples, which gained +1.34%. Meanwhile, the worst-performing sectors were Consumer Discretionary, which fell -1.65%, Energy, which fell -1.01%, and Health Care, which fell -0.65%. The top-performing subsectors were aerospace, consumer staples distribution, and household appliances. Meanwhile, auto, petroleum & petrochemicals, and electric equipment were among the worst-performing subsectors. Southbound Stock Connect volumes were light, as Mainland investors sold a net -$154 million worth of Hong Kong-listed stocks and ETFs, led by BYD, which was a large net buy, Semiconductor Manufacturing International (SMIC), a small net buy, the Hong Kong Tracker ETF, a large net sell, the Hang Seng China Enterprise ETF, a large net sell, Xiaomi, Geely Auto, and CNOOC, all small net sells, and Tencent, a very small net sell.

Shanghai, Shenzhen and the STAR Board gained +0.22%, +0.68%, and +1.72%, respectively, on volume that decreased -11.66% from yesterday, which is 124% of the 1-year average. 3,808 stocks advanced while 1,152 stocks declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Information Technology, which gained +1.3%, Materials, which gained +0.45%, and Real Estate, which gained +0.40%. Meanwhile, the worst-performing sectors were Energy, which fell -0.96%, Consumer Staples, which fell -0.56%, and Industrials, which fell -0.41%. The top-performing subsectors were aerospace, semiconductors, and precious metals. Meanwhile, oil & gas, autos, and fine chemicals were among the worst-performing subsectors. Northbound Stock Connect volumes were above average. CNY and the Asia Dollar Index both fell versus the US dollar. Treasury bond prices fell. Copper and steel rose.

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | -0.3% |

| Hang Seng Tech | HSTECH Index | 0% |

| Hong Kong Turnover | HKTurn Index | -10.7% |

| HK Short Sale Turnover | HKSST Index | 13.5% |

| Short Turnover as a % of HK Turnovr | N/A | 17.1% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 0 |

| China (Shanghai) | SHCOMP Index | 0.2% |

| China (Shenzhen) | SZCOMP Index | 0.7% |

| China (STAR Board) | Star50 Index | 1.7% |

| Mainland Turnover | .chturn Index | -11.7% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0% |

| Japan | NKY Index | -1.2% |

| India | SENSEX Index | -0.1% |

| Indonesia | JCI Index | -2.1% |

| Malaysia | FBMKLCI Index | -1% |

| Pakistan | KSE100 Index | 0.7% |

| Philippines | PCOMP Index | 0.4% |

| South Korea | KOSPI Index | -0.2% |

| Taiwan | TWSE Index | -0.7% |

| Thailand | SET Index | -0.9% |

| Singapore | STI Index | -0.5% |

| Australia | AS51 Index | -0.6% |

| Vietnam | VNINDEX Index | 0.2% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | -0.15 |

| Communication Services | 9 | 1.59 |

| Consumer Discretionary | 30 | -1.65 |

| Consumer Staples | 13 | 1.34 |

| Energy | 7 | -1.02 |

| Financials | 23 | -0.11 |

| Health Care | 13 | -0.65 |

| Industrials | 19 | 0.98 |

| Information Technology | 10 | -0.38 |

| Materials | 10 | 1.69 |

| Real Estate | 6 | -0.31 |

| Utilities | 12 | -0.49 |

| Mainland China Listed | 432 | 0.17 |

| Communication Services | 9 | 0.38 |

| Consumer Discretionary | 31 | -0.39 |

| Consumer Staples | 27 | -0.55 |

| Energy | 16 | -0.95 |

| Financials | 63 | 0.23 |

| Health Care | 40 | 0.23 |

| Industrials | 69 | -0.4 |

| Information Technology | 85 | 1.31 |

| Materials | 68 | 0.45 |

| Real Estate | 7 | 0.4 |

| Utilities | 17 | 0.1 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 1.6 |

| Alibaba HK | 9988 HK Equity | -2 |

| JD.com HK | 9618 HK Equity | 0.8 |

| NetEase HK | 9999 HK Equity | 2.2 |

| Yum China HK | 9987 HK Equity | 1.2 |

| Baozun HK | 9991 HK Equity | 2 |

| Baidu HK | 9888 HK Equity | 1.7 |

| Autohome HK | 2518 HK Equity | -1.9 |

| Bilibili HK | 9626 HK Equity | 1.6 |

| Trip.com HK | 9961 HK Equity | 1.6 |

| EDU HK | 9901 HK Equity | -1.4 |

| Xpeng HK | 9868 HK Equity | -3 |

| Weibo HK | 9898 HK Equity | 1.1 |

| Li Auto HK | 2015 HK Equity | -3.2 |

| Nio Auto HK | 9866 HK Equity | -4.6 |

| Zhihu HK | 2390 HK Equity | -2.5 |

| KE HK | 2423 HK Equity | 0.8 |

| Tencent Music Entertainment HK | 1698 HK Equity | 4.5 |

| Meituan HK | 3690 HK Equity | -0.9 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| BYD CO LTD-H | -6.8 |

| ALIBABA GROUP HOLDING LTD | -2 |

| XIAOMI CORP-CLASS B | -0.8 |

| TENCENT HOLDINGS LTD | 1.6 |

| SEMICONDUCTOR MANUFACTURING | 0.3 |

| MEITUAN-CLASS B | -0.9 |

| GEELY AUTOMOBILE HOLDINGS LT | -5.7 |

| HSBC HOLDINGS PLC | 0.9 |

| HONG KONG EXCHANGES & CLEAR | -0.7 |

| LI AUTO INC-CLASS A | -3.2 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| BYD CO LTD -A | -4.3 |

| TALKWEB INFORMATION SYSTEM-A | -0.3 |

| ALL WINNER TECHNOLOGY CO L-A | 16.2 |

| CONTEMPORARY AMPEREX TECHN-A | -3.8 |

| CAMBRICON TECHNOLOGIES-A | -1.1 |

| GREATOO INTELLIGENT EQUIPM-A | 7.1 |

| ZTE CORP-A | 2.4 |

| SHENZHEN EVERWIN PRECISION-A | 8.2 |

| EAST MONEY INFORMATION CO-A | 0.1 |

| HANGZHOU IRON & STEEL CO-A | 3.1 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.27 versus 7.29 yesterday

- CNY per EUR 7.64 versus 7.64 yesterday

- Yield on 10-Year Government Bond 1.71% versus 1.70% yesterday

- Yield on 10-Year China Development Bank Bond 1.72% versus 1.72% yesterday

- Copper Price +0.17%

- Steel Price -1.11%