Can’t Miss Tariff TV

7 Min. Read Time

Key News

Asian equities had a quiet night on light volumes, as global investors sit on the sidelines in advance of today’s can’t-miss TV: tariff announcements.

The Philippines managed a +1% gain, while Indonesia and Pakistan remain closed for Eid al-Fitr. Hong Kong and Mainland China bounced around the room, posting small gains on light volumes as Mainland China’s volume dipped below the RMB 1 trillion value traded level for the first time since January 13th. Markets were quite resilient, in my opinion, though foreign ownership of the space remains low.

Xiaomi fell -4.19% and was Hong Kong’s most heavily traded stock, trading 3X the value of the second most heavily traded. This is following the fatal crash involving their SU7 electric vehicle (EV). The crash and investigation are giving investors a reason to take profits after the stock had risen +257% since April 2, 2024, to its 52-week high on March 19, 2025. Mainland investors bought the Xiaomi dip today via Southbound Stock Connect. Mainland-listed EV battery maker CATL gained +0.03% after announcing the Xiaomi crash vehicle did not have a CATL battery in it, while also announcing a partnership with Sinopec to develop 500 EV battery swap stations with a goal of 10,000 in total.

Mainland investors bought a healthy $1.5 billion worth of Hong Kong-listed stocks and ETFs, accounting for 43% of Hong Kong turnover.

Hong Kong-listed EV names, other than Xiaomi and BYD, had a good day following yesterday’s March sales data, as Leapmotor gained +12.98% and Geely Auto gained +4.69% after announcing stronger-than-expected sales numbers.

Hong Kong-listed internet stocks were higher after the National Financial Regulatory Administration, the Ministry of Science & Technology, and the National Development and Reform Commission (NDRC) all announced policy support for financial firms to “leverage advanced technologies including cloud computing, big data, and artificial intelligence.”

Alibaba gained +0.15% on reports that its open-source large language model (LLM) is growing in popularity. After the close, Alibaba announced that it repurchased 6 million US-listed shares in Q1, at a cost of $600 million, and 150 million US-listed shares for the year ended 3/31/2025, at a cost of $11.9 billion.

Internet stocks overall had mixed performance overnight. Tencent was flat after buying back 996,000 shares today, Meituan fell -0.06%, Kuaishou gained +2.32%, JD.com gained +0.43%, Trip.com gained +0.08%, NetEase gained +0.43% and Baidu +1.12%.

Healthcare names were lower in both Hong Kong and Mainland China on profit-taking after strong moves in recent sessions. Wuxi AppTec fell -0.94% after selling 50.8 million shares of Wuxi XDC, which fell -6.85%, raising HKD 2.2 billion.

Mainland defensive plays such as banks and insurance outperformed, while energy and technology hardware were off as investors worried about the consequences tariffs could have on the global economy. Precious metals and mining were also off. All told, it was a quiet night, though I doubt tomorrow will be. Hopefully, tariffs do not end up being as bad as anticipated, which could cause a relief rally. Remember, the most crowded trade is not China equities; rather, it is US equities.

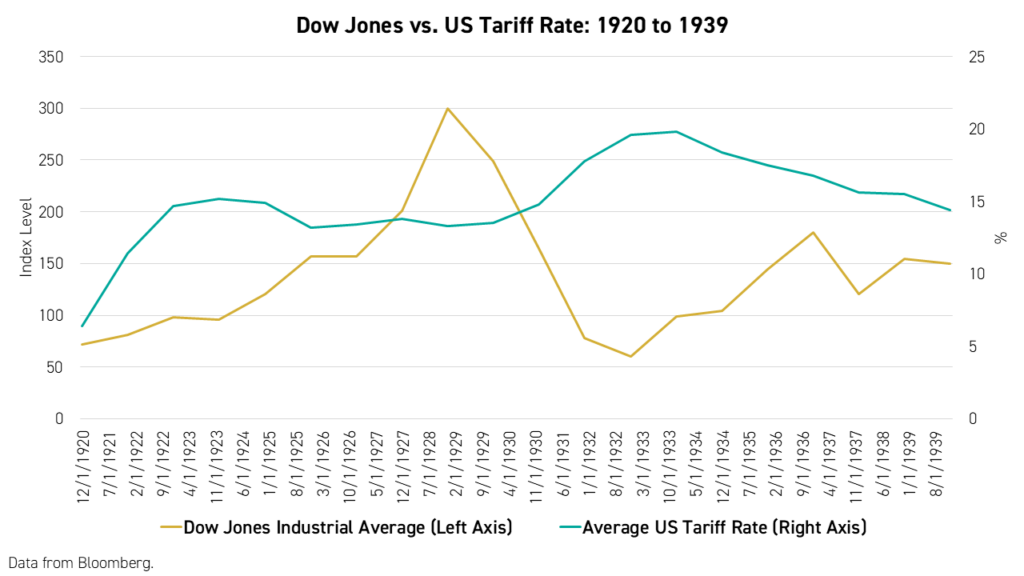

There has been shockingly little discussion of the last time the US government implemented high tariffs: the 1920s and 1930s. I have not read John Steinbeck’s The Grapes of Wrath since high school, but it left a strong impression on me. My father’s experience growing up in the 1930s and 1940s also had a significant impact on our family (save, save, save!, no debt, no loans, no credit cards, spend as little as possible). Below is the Dow Jones Industrial Average versus the average US tariff rate during the 1920s and 1930s. You can come to your own conclusions, though the market seemed to fall in advance of the tariffs being implemented as regime change causes market uncertainty. It is also worth noting that the Smoot Hawley Tariff Act was passed in June 1930, after the 1929 stock market crash. Yes, things are different today. I only bring it up because no one else appears to be.

The Hang Seng and Hang Seng Tech indexes diverged to close -0.02% and +0.35%, respectively, on volume that decreased -13.44% from yesterday, which is 129% of the 1-year average. 177 stocks advanced, while 302 stocks declined. Main Board short turnover decreased -15.5% from yesterday, which is 129% of the 1-year average, as 15% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth, value, and small caps outperformed momentum, dividends, quality, and large caps. The top-performing sectors were Consumer Staples, which gained +1.1%; Financials, which gained +0.87%; and Utilities, which gained +0.65%. Meanwhile, the worst-performing sectors were Information Technology, which fell -2.48%; Materials, which fell -1.84%; and Healthcare, which fell -0.62%. The top-performing subsectors were consumer staples distribution, food, and construction materials, while national defense, household/personal products, and technology hardware were among the worst-performing. Southbound Stock Connect volumes were 3X pre-stimulus levels, as Mainland investors bought a net $1.5 billion worth of Hong Kong-listed stocks and ETFs, led by Xiaomi and Alibaba, which were large net buys, Tencent, Semiconductor Manufacturing International (SMIC), Leapmotor, and Xpeng.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.05%, +0.12%, and -0.16%, respectively, on volume that decreased -14.02% from yesterday, which is 81% of the 1-year average. 2,726 stocks advanced, while 2,184 stocks declined. Momentum, value, dividends, and large caps “outperformed” (i.e. fell less than) the growth factor and small caps. Financials and Information Technology were the only positive sectors, up +0.69% and +0.11%, respectively. Meanwhile, the worst-performing sectors were Healthcare, which fell -1.08%, Utilities, which fell -0.73%, and Materials, which fell -0.67%. The top-performing subsectors were the forest industry, construction machinery, and textile/garment industry. Meanwhile, precious metals, aerospace, and energy equipment were among the worst-performing subsectors. Northbound Stock Connect volumes were near their one-year average. CNY and the Asia Dollar Index both fell slightly versus the US dollar. Treasury bonds rallied. Copper fell, and steel rose.

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 0% |

| Hang Seng Tech | HSTECH Index | 0.4% |

| Hong Kong Turnover | HKTurn Index | -13.4% |

| HK Short Sale Turnover | HKSST Index | -15.5% |

| Short Turnover as a % of HK Turnovr | N/A | 14.7% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 503.9 |

| China (Shanghai) | SHCOMP Index | 0.1% |

| China (Shenzhen) | SZCOMP Index | 0.1% |

| China (STAR Board) | Star50 Index | -0.2% |

| Mainland Turnover | .chturn Index | -14% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0% |

| Japan | NKY Index | 0.3% |

| India | SENSEX Index | 0.8% |

| Indonesia | JCI Index | 0.6% |

| Malaysia | FBMKLCI Index | 0.9% |

| Pakistan | KSE100 Index | 0.2% |

| Philippines | PCOMP Index | 1.1% |

| South Korea | KOSPI Index | -0.6% |

| Taiwan | TWSE Index | 0.1% |

| Thailand | SET Index | 0.4% |

| Singapore | STI Index | -0.4% |

| Australia | AS51 Index | 0.1% |

| Vietnam | VNINDEX Index | 0% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 0.09 |

| Communication Services | 9 | 0.22 |

| Consumer Discretionary | 30 | 0.21 |

| Consumer Staples | 13 | 1.1 |

| Energy | 7 | -0.15 |

| Financials | 23 | 0.87 |

| Health Care | 13 | -0.62 |

| Industrials | 19 | 0.04 |

| Information Technology | 10 | -2.48 |

| Materials | 10 | -1.84 |

| Real Estate | 6 | 0.54 |

| Utilities | 12 | 0.65 |

| Mainland China Listed | 432 | -0.09 |

| Communication Services | 9 | -0.12 |

| Consumer Discretionary | 31 | -0.45 |

| Consumer Staples | 27 | -0.37 |

| Energy | 16 | -0.22 |

| Financials | 63 | 0.68 |

| Health Care | 40 | -1.09 |

| Industrials | 69 | -0.04 |

| Information Technology | 85 | 0.09 |

| Materials | 68 | -0.69 |

| Real Estate | 7 | -0.11 |

| Utilities | 17 | -0.74 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 0 |

| Alibaba HK | 9988 HK Equity | 0.2 |

| JD.com HK | 9618 HK Equity | 0.4 |

| NetEase HK | 9999 HK Equity | 0.4 |

| Yum China HK | 9987 HK Equity | 1.3 |

| Baozun HK | 9991 HK Equity | 0 |

| Baidu HK | 9888 HK Equity | 1.1 |

| Autohome HK | 2518 HK Equity | 1.3 |

| Bilibili HK | 9626 HK Equity | -0.2 |

| Trip.com HK | 9961 HK Equity | 0.1 |

| EDU HK | 9901 HK Equity | 1.8 |

| Xpeng HK | 9868 HK Equity | -0.4 |

| Weibo HK | 9898 HK Equity | -0.1 |

| Li Auto HK | 2015 HK Equity | 1.2 |

| Nio Auto HK | 9866 HK Equity | 1.2 |

| Zhihu HK | 2390 HK Equity | -2.2 |

| KE HK | 2423 HK Equity | 0.9 |

| Tencent Music Entertainment HK | 1698 HK Equity | 0.6 |

| Meituan HK | 3690 HK Equity | -0.1 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| XIAOMI CORP-CLASS B | -4.2 |

| ALIBABA GROUP HOLDING LTD | 0.2 |

| TENCENT HOLDINGS LTD | 0 |

| SEMICONDUCTOR MANUFACTURING | 0.9 |

| BYD CO LTD-H | -1.2 |

| MEITUAN-CLASS B | -0.1 |

| KUAISHOU TECHNOLOGY | 2.3 |

| XPENG INC - CLASS A SHARES | -0.4 |

| GEELY AUTOMOBILE HOLDINGS LT | 4.7 |

| HONG KONG EXCHANGES & CLEAR | 1.7 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| EAST MONEY INFORMATION CO-A | 1.1 |

| BYD CO LTD -A | -1.4 |

| LUXSHARE PRECISION INDUSTR-A | -2.7 |

| KYLAND TECHNOLOGY CO LTD-A | 15.8 |

| NINGBO SHUANGLIN AUTO PART-A | 7 |

| CONTEMPORARY AMPEREX TECHN-A | 0 |

| KWEICHOW MOUTAI CO LTD-A | -0.4 |

| AECC AVIATION POWER CO-A | -10 |

| ZHEJIANG HAIKONG NANKE HUATI | 4.5 |

| JIANGSU HENGRUI PHARMACEUT-A | -1.8 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.27 versus 7.27 yesterday

- CNY per EUR 7.87 versus 7.84 yesterday

- Yield on 10-Year Government Bond 1.79% versus 1.81% yesterday

- Yield on 10-Year China Development Bank Bond 1.82% versus 1.85% yesterday

- Copper Price -0.03%

- Steel Price 0.44%