Hong Kong Leans Into Headwinds

5 Min. Read Time

Key News

Asian equities were lower following President Trump’s threat to increase steel and aluminum tariffs to 50% on June 4th, last week’s escalation of US rhetoric on trade, semiconductors, technology, and international students.

US Defense Secretary Hegseth’s speech at the Shangri-La Dialogue in Singapore (with Chinese government officials in the room, though their defense chief didn’t attend) was overshadowed by concerns about an escalation of the conflict in the Middle East. Japan, Taiwan, and Indonesia underperformed while Mainland China, Thailand, and Malaysia were closed for the Dragon Boat Festival, a special market holiday, and the Yang Dipertuan Agong's Birthday, respectively.

However, it was not all bad news overnight, as, during his Sunday morning CBS interview, Treasury Secretary Bessent mentioned that a Trump-Xi phone conversation on the Geneva trade truce would occur “very soon”. Also, the US Trade Representative extended China tariff exemptions that expired on May 31st to August 31st.

The Hang Seng and Hang Seng Tech indexes hit morning lows of -2.67% and -3.11%, respectively, though rallied to close lower by -0.57% and -0.7%. This occurred without the support of Mainland investors, as Southbound Stock Connect, which usually makes up over 40% of Hong Kong turnover, was closed due to the Mainland market holiday. The Hong Kong market showed some resilience, coming off those intra-day lows, in a positive sign.

Internet stocks were mixed, though electric vehicles (EVs) and hybrids were weaker after the Ministry of Industry and Information Technology (MIIT) referenced the “disorderly price war” amongst auto makers, which follows similar comments from the China Association of Automobile Manufacturers (CAAM) following BYD's 1.88% price cut last week. The auto overcapacity issue appears to be hitting the government’s radar, though I am not sure what they can do about it. The space was weaker despite strong May results. Leap Motor gained +3.34% after selling 45,067 cars, BYD sold 382,500 cars, up +148% year-over-year (YoY), Li Auto fell -2.05% despite selling 40,856 cars, which is up +16.7% YoY, XPeng fell -1.64% despite selling 33,525 cars, up +230% YoY, Xiaomi gained +1.28% after selling 28,000 cars, and NIO was down -2.14% despite selling 23,231 cars, up +13.1% YoY. With all the talk of auto overcapacity, I looked at the pre-tax profit margin of global auto makers: Ferrari (28.3%), Tesla (9.2%), BYD (6.4%), Ford (3.9%), General Motors (4.5%), Stellantis (2.6%), Toyota (13. 4%), and Honda (6.1%).

Banks and oil were weaker, though some consumer plays were strong, including Macau casinos. Real estate was off after distressed developer New World suspended a coupon on a preferred stock that did not trigger default, though it weighed on the space. The average housing price across 100 Chinese cities improved +0.3% month over month (MoM) in May, and rose +2.65% YoY, driven by the top improvers Shanghai, up +1.47%, and Guangzhou, up +1.2%, as 33 cities had rising new home prices while 54 declined. Used home prices declined -0.71% MoM and -7.24% YoY.

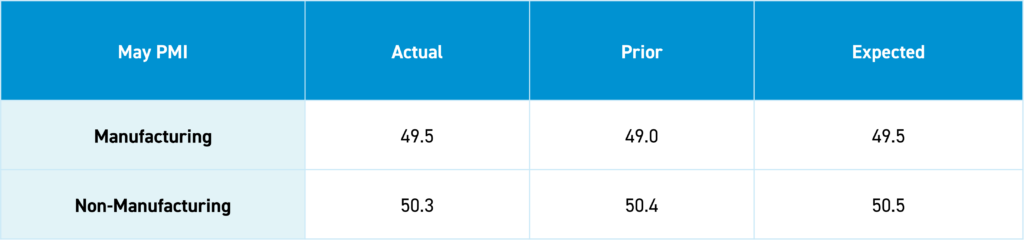

May PMIs were not too bad, especially considering the trade was supposed to be economic Armageddon.

Last Night's Performance

| Country / Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | -0.6% |

| Hang Seng Tech | HSTECH Index | -0.7% |

| Hong Kong Turnover | HKTurn Index | -46.5% |

| Hong Kong Short Sale Turnover | HKSST Index | -31.3% |

| Short Turnover as a % of Hong Kong Turnover | N/A | 17.7% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 140.3 |

| China (Shanghai) | SHCOMP Index | Closed |

| China (Shenzhen) | SZCOMP Index | Closed |

| China (STAR Board) | Star50 Index | Closed |

| Mainland Turnover | .chturn Index | Closed |

| Northbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0% |

| Japan | NKY Index | -1.3% |

| India | SENSEX Index | -0.1% |

| Indonesia | JCI Index | -1.5% |

| Malaysia | FBMKLCI Index | -0.7% |

| Pakistan | KSE100 Index | -0.9% |

| Philippines | PCOMP Index | 0.2% |

| South Korea | KOSPI Index | 0% |

| Taiwan | TWSE Index | -1.6% |

| Thailand | SET Index | -1.3% |

| Singapore | STI Index | -0.1% |

| Australia | AS51 Index | -0.2% |

| Vietnam | VNINDEX Index | 0.3% |

| Indicator | Hong Kong | Mainland China |

|---|---|---|

| Today's Volume % of 1-Year Average | 77 | Closed |

| Advancing Stocks | 121 | Closed |

| Declining Stocks | 358 | Closed |

| Outperforming Factors | Growth, EPS Revisions, Momentum | Closed |

| Underperforming Factors | Value, Low Volatility, Liquidity | Closed |

| Top Sectors | Materials, Information Technology | Closed |

| Bottom Sectors | Real Estate, Health Care, Energy | Closed |

| Top Subsectors | Consumer Services, Consumer Durables, Apparel, Healthcare Equipment | Closed |

| Bottom Subsectors | Coal, Household Products, Paper & Packaging | Closed |

| Southbound Connect Buys | Closed | N/A |

| Southbound Connect Sells | Closed | N/A |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 151 | -2.03 |

| Communication Services | 9 | -2.71 |

| Consumer Discretionary | 28 | -2.81 |

| Consumer Staples | 13 | -2.2 |

| Energy | 7 | -0.65 |

| Financials | 23 | -0.55 |

| Health Care | 13 | -0.17 |

| Industrials | 20 | -1.07 |

| Information Technology | 10 | -2.17 |

| Materials | 10 | -1.82 |

| Real Estate | 6 | 0.04 |

| Utilities | 12 | -1.12 |

| Mainland China Listed | 404 | -0.58 |

| Communication Services | 6 | -1.02 |

| Consumer Discretionary | 31 | -1.14 |

| Consumer Staples | 24 | -0.58 |

| Energy | 13 | -0.21 |

| Financials | 64 | 0.08 |

| Health Care | 31 | 0.05 |

| Industrials | 64 | -0.61 |

| Information Technology | 91 | -1.61 |

| Materials | 58 | -0.64 |

| Real Estate | 6 | -0.52 |

| Utilities | 16 | -0.32 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 0 |

| Alibaba HK | 9988 HK Equity | -0.6 |

| JD.com HK | 9618 HK Equity | -0.2 |

| NetEase HK | 9999 HK Equity | 1 |

| Yum China HK | 9987 HK Equity | -1.2 |

| Baozun HK | 9991 HK Equity | -1.5 |

| Baidu HK | 9888 HK Equity | -0.3 |

| Autohome HK | 2518 HK Equity | 0 |

| Bilibili HK | 9626 HK Equity | -2.5 |

| Trip.com HK | 9961 HK Equity | 0.5 |

| EDU HK | 9901 HK Equity | -3.1 |

| Xpeng HK | 9868 HK Equity | -1.6 |

| Weibo HK | 9898 HK Equity | 0.7 |

| Li Auto HK | 2015 HK Equity | -2 |

| Nio Auto HK | 9866 HK Equity | -2.1 |

| Zhihu HK | 2390 HK Equity | -1.6 |

| KE HK | 2423 HK Equity | -2.8 |

| Tencent Music Entertainment HK | 1698 HK Equity | -1.3 |

| Meituan HK | 3690 HK Equity | -1.7 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | -0.6 |

| TENCENT HOLDINGS LTD | 0 |

| BYD CO LTD-H | -1.9 |

| XIAOMI CORP-CLASS B | 1.3 |

| MEITUAN-CLASS B | -1.7 |

| HONG KONG EXCHANGES & CLEAR | -0.1 |

| AIA GROUP LTD | 0.1 |

| PING AN INSURANCE GROUP CO-H | -1.2 |

| CHINA CONSTRUCTION BANK-H | -1.7 |

| POP MART INTERNATIONAL GROUP | 4.4 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| BYD CO LTD -A | -2.4 |

| SHENZHEN FORMS SYNTRON INF-A | 7.3 |

| LAKALA PAYMENT CO LTD-A | 3.4 |

| CONTEMPORARY AMPEREX TECHN-A | -0.7 |

| KUNMING YUNNEI POWER CO-A | -2.5 |

| KWEICHOW MOUTAI CO LTD-A | -1.2 |

| GUANGZHOU HAIGE COMMUNICAT-A | 8 |

| FUJIAN SNOWMAN GROUP CO-A | 3 |

| VICTORY GIANT TECHNOLOGY -A | 2.6 |

| CAMBRICON TECHNOLOGIES-A | -1.5 |

Last Night's Exchange Rates, Prices, & Yields

Mainland China's currency, bond, and commodity markets were closed overnight.