June Trade & Credit Data Beat Expectations

6 Min. Read Time

Key News

Asian equities were mixed overnight, led higher by Thailand and the Philippines, as President Trump’s tariff ire over the weekend was focused on the EU and Mexico.

Hong Kong grinded higher throughout the trading day. Stronger-than-expected export/import data provided a late-day boost, while Shanghai and Shenzhen bounced around the room to end slightly higher. Hong Kong saw large buying from Mainland China via Southbound Stock Connect. Internet stocks were largely higher, as Alibaba gained +0.95%, Tencent gained +0.68%, and Meituan gained +0.75%, though video platform Bilibili fell -0.35%, despite announcing 2025 gaming and advertising revenue growth targets of +20% and +15%.

Pharmaceuticals, biotech, auto, coal, non-ferrous metals, precious metals, and oil all had good sessions, while consumer services, such as hotels and restaurants, were off. The Mainland’s pockets of strength were oil, banks, electricity, telecom, and precious metals. Meanwhile, semiconductors, software, healthcare equipment, and defense were all off.

Battery maker Contemporary Amperex Technology (CATL) fell -1.1% in Mainland trading, despite a deal with Australian miner BHP.

Solar manufacturer Tongwei gained +1.18% after announcing its first half net income loss would be in a range from RMB -3.9 billion to -5.2 billion, despite installed capacity growth due to “the imbalance between supply and demand in the industry, which has not improved significantly, and the product prices of each link have been continuously depressed.” Peer LONGi Green Energy Technology fell -0.55% after announcing its first half net income loss will be between RMB -2.4 billion and RMB -2.8 billion.

Hopefully, overcapacity efforts kick into gear as investors look up China’s government’s new buzzword: anti-involutionary. Involution is when intense competition leads to diminished returns. Solar, steel, cement, autos, and E-Commerce are areas highlighted by the government to face “anti-involutionary” measures. The effect could bring the end of China’s deflationary effect on the global economy as well as its domestic economy. It could also lead to higher margins and profits for listed corporations. It is also very aligned with President Trump’s China demands.

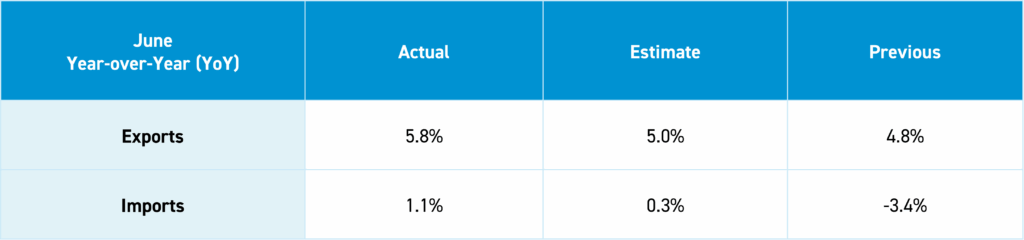

Export/import and credit data release was stronger than expected.

Export/Import Release

Some additional metrics to consider include the following.

- Rare Earth Exports increased +32% month-over-month (MoM), as export volume increased to 7.74 million tons from May’s 5.86 million tons

- Exports to the US declined -16.1% YoY, though were up +32% MoM

- US imports increased to $11.6 billion from May’s $10.8 billion, though are down -8.7% for the first six months of the year compared to the first six months of 2024.

- China’s total trade balance was $114 billion, versus expectations of $112 billion and May’s $103 billion.

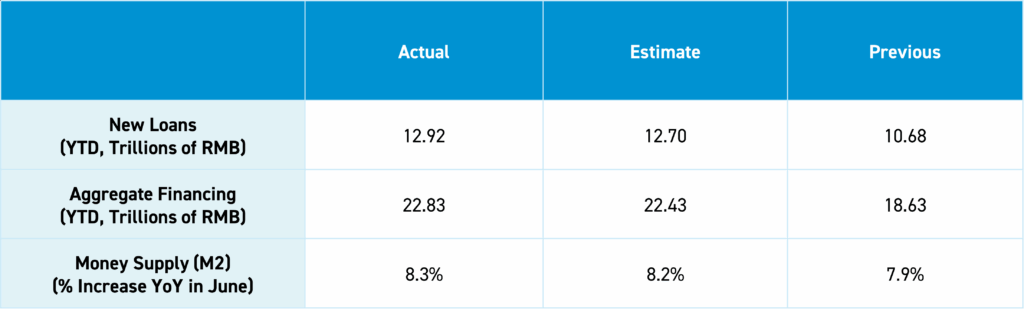

June Credit Data

The People’s Bank of China (PBOC) held a press conference overnight. The release noted “the effect of monetary policy supporting the real economy is relatively obvious”, as social financing, new loans, and M2 data all beat expectations. Since 2020, the bank reserve requirement ratio has been cut twelve times, along with “9 policy rate reductions, lowering 1-year and 5-year LPR by 115 basis points and 130 basis points, respectively.” (The 5-Year Loan Prime Rate determines the mortgage rate). Lower interest rates have lowered the average corporate loan yields by 0.45% to 3.30% and new housing loan rates by 0.60% to 3.10%. Efforts will continue “to implement moderate loose monetary policy… better promote the expansion of domestic demand…”. The release also stated that the market expects interest rate cuts in the second half of the year, as the “misalignment of the monetary policy cycle between China and the United States will be improved”, as spreads narrow.

It is funny that the PBOC and Trump both think Powell should cut US interest rates. GDP, new and second-hand home sales, retail sales, industrial production, and fixed asset investment will all be reported today.

On Friday, I stated that Hank Paulson’s conversation with Vice Premier Ding Xuexiang received significant attention in China. I incorrectly stated that Paulson was a Democrat. Paulson was Secretary of the Treasury under George W. Bush. My bad! He did endorse Hillary Clinton in 2016, despite being a lifelong Republican.

Last Night’s Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 0.3% |

| Hang Seng Tech | HSTECH Index | 0.7% |

| Hong Kong Turnover | HKTurn Index | -35.1% |

| Hong Kong Short Sale Turnover | HKSST Index | -31.9% |

| Short Turnover as a % of Hong Kong Turnover | N/A | 11.5% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 195.3 |

| China (Shanghai) | SHCOMP Index | 0.3% |

| China (Shenzhen) | SZCOMP Index | 0.1% |

| China (STAR Board) | Star50 Index | -0.2% |

| Mainland Turnover | .chturn Index | -14.8% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | -0.9% |

| Japan | NKY Index | -0.3% |

| India | SENSEX Index | -0.3% |

| Indonesia | JCI Index | 0.7% |

| Malaysia | FBMKLCI Index | 0.1% |

| Pakistan | KSE100 Index | 1.7% |

| Philippines | PCOMP Index | 1% |

| South Korea | KOSPI Index | 0.8% |

| Taiwan | TWSE Index | -0.6% |

| Thailand | SET Index | 2% |

| Singapore | STI Index | 0.5% |

| Australia | AS51 Index | -0.1% |

| Vietnam | VNINDEX Index | 0.9% |

| Indicator | Hong Kong | Mainland China |

|---|---|---|

| Today's Volume % of 1-Year Average | 104 | 100 |

| Advancing Stocks | 343 | 2920 |

| Declining Stocks | 137 | 2040 |

| Outperforming Factors | Momentum, EPS Revision, Low Volatility | EPS Revision, Dividend Yield, Value |

| Underperforming Factors | Buyback, Value, Liquidity | Liquidity, Buyback, Quality |

| Top Sectors | Energy, Materials, Staples | Energy, Utilities, Materials |

| Bottom Sectors | Real Estate | Real Estate, Communication, Healthcare |

| Top Subsectors | Construction Materials, Coal, Building | Soft Drink, Precious Metals, Oil/Gas |

| Bottom Subsectors | Consumer Services, Textiles, National Defense | Diversified Financials, Real Estate, Software |

| Southbound Connect Buys | Alibaba, Meituan (Large), Guotai Junan (Small) | N/A |

| Southbound Connect Sells | Healthyway, Xiaomi (Small) | N/A |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 0.7 |

| Communication Services | 9 | 0.61 |

| Consumer Discretionary | 30 | 0.81 |

| Consumer Staples | 13 | 1.29 |

| Energy | 7 | 2.31 |

| Financials | 23 | 0.4 |

| Health Care | 13 | 1.24 |

| Industrials | 19 | 0.63 |

| Information Technology | 10 | 0.1 |

| Materials | 10 | 2.23 |

| Real Estate | 6 | -0.01 |

| Utilities | 12 | 1.12 |

| Mainland China Listed | 432 | 0.18 |

| Communication Services | 9 | -0.86 |

| Consumer Discretionary | 31 | 0.15 |

| Consumer Staples | 27 | 0.12 |

| Energy | 16 | 1.21 |

| Financials | 63 | 0.09 |

| Health Care | 40 | 0 |

| Industrials | 69 | 0.07 |

| Information Technology | 85 | 0.07 |

| Materials | 68 | 0.62 |

| Real Estate | 7 | -1.16 |

| Utilities | 17 | 0.88 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 0.7 |

| Alibaba HK | 9988 HK Equity | 1 |

| JD.com HK | 9618 HK Equity | -0.7 |

| NetEase HK | 9999 HK Equity | 0.2 |

| Yum China HK | 9987 HK Equity | -0.6 |

| Baozun HK | 9991 HK Equity | 2.7 |

| Baidu HK | 9888 HK Equity | -2.7 |

| Autohome HK | 2518 HK Equity | -2.1 |

| Bilibili HK | 9626 HK Equity | -0.3 |

| Trip.com HK | 9961 HK Equity | 0.2 |

| EDU HK | 9901 HK Equity | -0.7 |

| Xpeng HK | 9868 HK Equity | 0.8 |

| Weibo HK | 9898 HK Equity | 0.1 |

| Li Auto HK | 2015 HK Equity | 2.6 |

| Nio Auto HK | 9866 HK Equity | 10.6 |

| Zhihu HK | 2390 HK Equity | -1.3 |

| KE HK | 2423 HK Equity | 0.2 |

| Tencent Music Entertainment HK | 1698 HK Equity | -0.6 |

| Meituan HK | 3690 HK Equity | 0.8 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | 1 |

| TENCENT HOLDINGS LTD | 0.7 |

| GUOTAI JUNAN INTERNATIONAL | -0.2 |

| MEITUAN-CLASS B | 0.8 |

| XIAOMI CORP-CLASS B | 0.8 |

| SEMICONDUCTOR MANUFACTURING | 2.2 |

| PING AN INSURANCE GROUP CO-H | 2.3 |

| CHINA CONSTRUCTION BANK-H | -1.5 |

| POP MART INTERNATIONAL GROUP | 2.3 |

| STAR PLUS LEGEND HOLDINGS-H | -4.7 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| CHINA NORTHERN RARE EARTH -A | 10 |

| EAST MONEY INFORMATION CO-A | 3.1 |

| INNER MONGOLIA BAOTOU STE-A | 1.4 |

| WUXI APPTEC CO LTD-A | 1.9 |

| ZHONGJI INNOLIGHT CO LTD-A | 3.1 |

| BEIJING COMPASS TECHNOLOGY-A | 13.1 |

| BOC INTERNATIONAL CHINA CO-A | -1.6 |

| HENGBAO CO LTD-A | -7.6 |

| BYD CO LTD -A | -1.7 |

| CHINA RARE EARTH RESOURCES-A | -4 |

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.17 versus 7.17 yesterday

- CNY per EUR 8.37 versus 8.38 yesterday

- Yield on 10-Year Government Bond 1.67% versus 1.67% yesterday

- Yield on 10-Year China Development Bank Bond 1.73% versus 1.73% yesterday

- Copper Price -0.31%

- Steel Price -0.06%