Hong Kong Gains, Mortgage Refinancing Powers Real Estate, Week in Review

7 Min. Read Time

Week in Review

- Asian equities were mixed but mostly higher this week as Hong Kong outperformed and South Korea underperformed.

- Shares in E-Commerce giant PDD were volatile this week as the company reported Q2 earnings that were slightly below estimates and management delivered an “uncertain” outlook.

- JD.com announced a $5 billion stock repurchase plan following Walmart’s approximately $3 billion share sale last week.

- US National Security Advisor Jake Sullivan met with President Xi and other Chinese leaders this week.

- In this week's video, KraneShares Cultural Analyst Xiabing Su explores the groundbreaking release of Black Myth: Wukong, China's first AAA game that's taking the global gaming industry by storm.

Key News

Asian equities ended a strong week and month on a high note as Hong Kong and Mainland China outperformed.

Today’s China performance is very noteworthy as Chinese stocks are a net sell in MSCI indices, although the market rallied regardless. That is a very strong sign, in my opinion. Stepping back and looking at the big picture, how many investors know this was the 4th positive week in a row for Hong Kong-listed stocks? How many investors know that Hong Kong-listed stocks beat US stocks in the month of August? Probably very few. Was the market volatile this month? 100%.

Today was also important due to a strong rotation into growth stocks, which outperformed, and out of value and dividend stocks, which underperformed. We have also stated that China will not be able to rally without the “good stuff,” i.e., growth stocks that foreign investors gravitate to.

There were multiple catalysts today as the Renminbi appreciated versus the US dollar.

There were reports that the government would allow for early refinancing of $5.4 trillion of mortgages, which would help households and the economy as households’ balance sheets would improve and might help domestic consumption. It also shows the government’s commitment to get the economy going.

Not surprisingly, real estate stocks ripped, making real estate the best-performing sector in both Hong Kong and Mainland China. The move explains the downdraft in banks overnight, though overall, it represents a net positive for China’s market and economy. I still can’t get anyone interested in Asian, US-dollar-denominated high-yield bonds despite tasty yields and good performance versus US high-yield, which would also benefit from the move.

The State Administration for Market Regulation, a government internet regulator, cleared Alibaba of any wrongdoing in a statement that was quite positive on the company. It called the company “a world-class enterprise and enhancing international competitiveness.”

Hong Kong’s most heavily traded stocks by value were Tencent, which gained +1.17%; Meituan, which gained +2.16%; Alibaba, which gained +3.04%; Ping An Insurance, which gained +3.6%; and China Construction Bank, which fell -1.95%.

Internet stocks and electric vehicle (EV) ecosystem stocks were higher, including BYD, which gained +5.98%, JD.com, which gained +3.57%, Kuaishou, which gained +2.28%, Li Auto, which gained +7.79%, Trip.com, which gained +0.87%, and NetEase, which gained +0.63%.

Mainland China had a strong day, led by real estate and growth stocks, as banks underperformed. Northbound Stock Connect saw very high volumes, though we don’t know whether the volume represents buys or sells. The National Team’s favored ETFs also saw heightened volumes overnight.

Today, passive managers globally will be trading at the market’s close so that their funds, ETFs, and/or separately managed accounts (SMAs) will match MSCI’s “refreshed” indexes on Monday (Tuesday in the US due to Labor Day).

MSCI Index Rebalance Key Points

1) Five of Brazil’s US listings (XP, NU, PAGS, STNE, INTR) will be added to MSCI Brazil, MSCI Emerging Markets, and MSCI All Country World Index for the first time. Five other local listed names are being added as well. From MSCI below. “Foreign listings will become eligible for the MSCI Brazil Indexes as part of the August 2024 Index Review, leading to 10 additions to the MSCI Brazil IMI.”

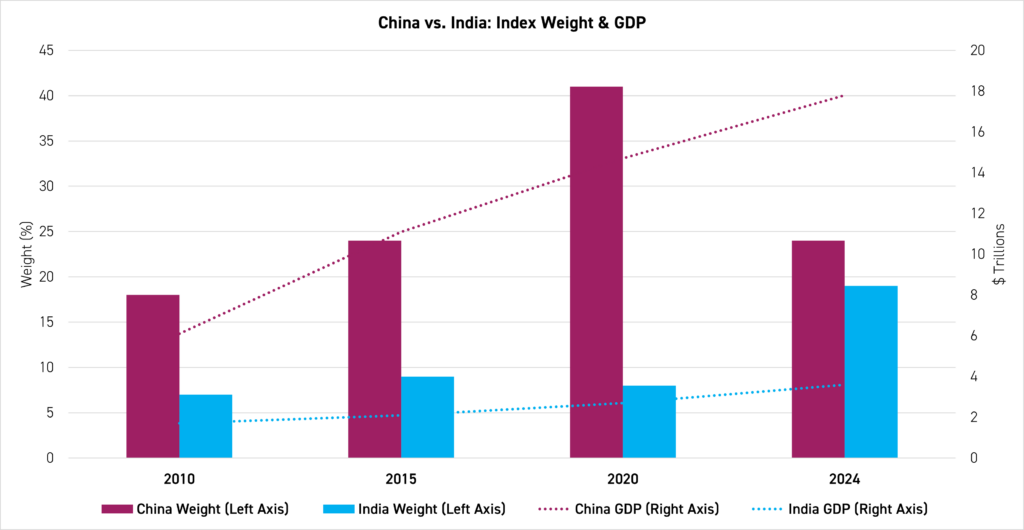

2) India’s HDFC Bank (ticker HDFCB IN for the local, ADR is HDB, $148 billion market cap) weight is increasing, which explains part of India’s rise in Emerging Markets. India has foreign ownership limits that have kept HDFC at a smaller than it probably should be. India is getting larger due to their rally while China’s weight has declined due to Mainland China’s underperformance, which explains the large number of China deletes. India’s rally is driven by local inflows as foreign investors have been selling due to valuations. India has a huge option market that is a factor. MSCI indices have a bit of a momentum element with the winners added and losers deleted. China and India’s GDP to market cap comparison is “interesting”.

The Hang Seng and Hang Seng Tech indexes gained +1.14% and +2.87%, respectively, on volume that increased +60.45% from yesterday, which is 167% of the 1-year average. 349 stocks advanced while 137 declined. Main Board short turnover increased +15.17% from yesterday, which is 117% of the 1-year average as 12% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small caps outperformed value and large caps. The top-performing sectors were Real Estate, which gained +4.97%, Consumer Discretionary, which gained +3.00%, and Consumer Staples, which gained +2.54%. Meanwhile, Utilities fell -0.79%, Financials fell -0.52%, and Health Care, which fell -0.49%. The top-performing subsectors were auto, retail, and media while banks, pharmaceuticals, and power utilities were among the worst-performing subsectors . Southbound Stock Connect volumes were moderate as Mainland investors bought a net $175 million worth of Hong Kong-listed stocks and ETFs, including Tencent, which was a large net buy, Ping An Insurance and Xiaomi, which were moderate net buys. Meanwhile, China Construction bank, Li Auto, and Meituan were small net sells.

Shanghai, Shenzhen, and the STAR Board gained +0.68%, +2.24%, and +2.14%, respectively, on volume that increased +44.45% from yesterday, which is 111% of the 1-year average. 4,631 stocks advanced while 391 declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Real Estate, which gained +4.77%, Technology, which gained +3.53%, and Consumer Discretionary, which gained +3.48%. Meanwhile, Utilities fell -0.22%. The top-performing subsectors were computer hardware, autos, and real estate services. Meanwhile, banking, precious metals, and telecom were among the worst-performing subsectors. Northbound Stock Connect volumes were very high. CNY and the Asia Dollar Index were stronger versus the US dollar. Steel and copper fell.

Last Night’s Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 1.1% |

| Hang Seng Tech | HSTECH Index | 2.9% |

| Hong Kong Turnover | HKTurn Index | 60.4% |

| HK Short Sale Turnover | HKSST Index | 15.2% |

| Short Turnover as a % of HK Turnovr | N/A | 11.7% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 175.1 |

| China (Shanghai) | SHCOMP Index | 0.7% |

| China (Shenzhen) | SZCOMP Index | 2.2% |

| China (STAR Board) | Star50 Index | 2.1% |

| Mainland Turnover | .chturn Index | 44.4% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 0.5% |

| Japan | NKY Index | 0.7% |

| India | SENSEX Index | 0.3% |

| Indonesia | JCI Index | 0.6% |

| Malaysia | FBMKLCI Index | 1.5% |

| Pakistan | KSE100 Index | 0.2% |

| Philippines | PCOMP Index | 0.1% |

| South Korea | KOSPI Index | 0.5% |

| Taiwan | TWSE Index | 0.3% |

| Thailand | SET Index | 0.1% |

| Singapore | STI Index | 1.1% |

| Australia | AS51 Index | 0.6% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 154 | 1.3 |

| Communication Services | 9 | 1.17 |

| Consumer Discretionary | 29 | 2.99 |

| Consumer Staples | 13 | 2.52 |

| Energy | 7 | 0 |

| Financials | 24 | -0.54 |

| Health Care | 14 | -0.51 |

| Industrials | 18 | 0.12 |

| Information Technology | 11 | 2.31 |

| Materials | 11 | -0.29 |

| Real Estate | 6 | 4.95 |

| Utilities | 12 | -0.81 |

| China Listed | 487 | 1.83 |

| Communication Services | 13 | 1.97 |

| Consumer Discretionary | 41 | 3.55 |

| Consumer Staples | 32 | 3.06 |

| Energy | 17 | 0.89 |

| Financials | 68 | 0.29 |

| Health Care | 45 | 1.86 |

| Industrials | 74 | 1.63 |

| Information Technology | 93 | 3.61 |

| Materials | 80 | 1.38 |

| Real Estate | 7 | 4.85 |

| Utilities | 17 | -0.15 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 1.2 |

| Alibaba HK | 9988 HK Equity | 3 |

| JD.com HK | 9618 HK Equity | 3.6 |

| NetEase HK | 9999 HK Equity | 0.6 |

| Yum China HK | 9987 HK Equity | 2 |

| Baozun HK | 9991 HK Equity | 9.6 |

| Baidu HK | 9888 HK Equity | 1.8 |

| Autohome HK | 2518 HK Equity | 2.7 |

| Bilibili HK | 9626 HK Equity | 2.5 |

| Trip.com HK | 9961 HK Equity | 0.9 |

| EDU HK | 9901 HK Equity | -1.7 |

| Xpeng HK | 9868 HK Equity | 8.3 |

| Weibo HK | 9898 HK Equity | 2.3 |

| Li Auto HK | 2015 HK Equity | 7.8 |

| Nio Auto HK | 9866 HK Equity | 10.7 |

| Zhihu HK | 2390 HK Equity | -0.1 |

| KE HK | 2423 HK Equity | 6.1 |

| Tencent Music Entertainment HK | 1698 HK Equity | 3.4 |

| Meituan HK | 3690 HK Equity | 2.2 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| TENCENT HOLDINGS LTD | 1.2 |

| MEITUAN-CLASS B | 2.2 |

| ALIBABA GROUP HOLDING LTD | 3 |

| PING AN INSURANCE GROUP CO-H | 3.6 |

| CHINA CONSTRUCTION BANK-H | -2 |

| IND & COMM BK OF CHINA-H | -2.8 |

| BYD CO LTD-H | 6 |

| XIAOMI CORP-CLASS B | 3.3 |

| AIA GROUP LTD | -0.4 |

| JD.COM INC-CLASS A | 3.6 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| KWEICHOW MOUTAI CO LTD-A | 2.1 |

| IND & COMM BK OF CHINA-A | -3.9 |

| PING AN INSURANCE GROUP CO-A | 3.3 |

| BYD CO LTD -A | 6.2 |

| CONTEMPORARY AMPEREX TECHN-A | 2 |

| LUXSHARE PRECISION INDUSTR-A | 5.9 |

| SERES GROUP CO L-A | 6.4 |

| WULIANGYE YIBIN CO LTD-A | 3.6 |

| AGRICULTURAL BANK OF CHINA-A | -4 |

| FOXCONN INDUSTRIAL INTERNE-A | 6.5 |

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.09 versus 7.09 yesterday

- CNY per EUR 7.86 versus 7.87 yesterday

- Yield on 10-Year Government Bond 2.17% versus 2.17% yesterday

- Yield on 10-Year China Development Bank Bond 2.27% versus 2.27% yesterday

- Copper Price: -0.23%

- Steel Price: -0.55%