Growth Stocks Rebound As Banks’ Balance Sheets Face Mortgage Refinancing

3 Min. Read Time

Key News

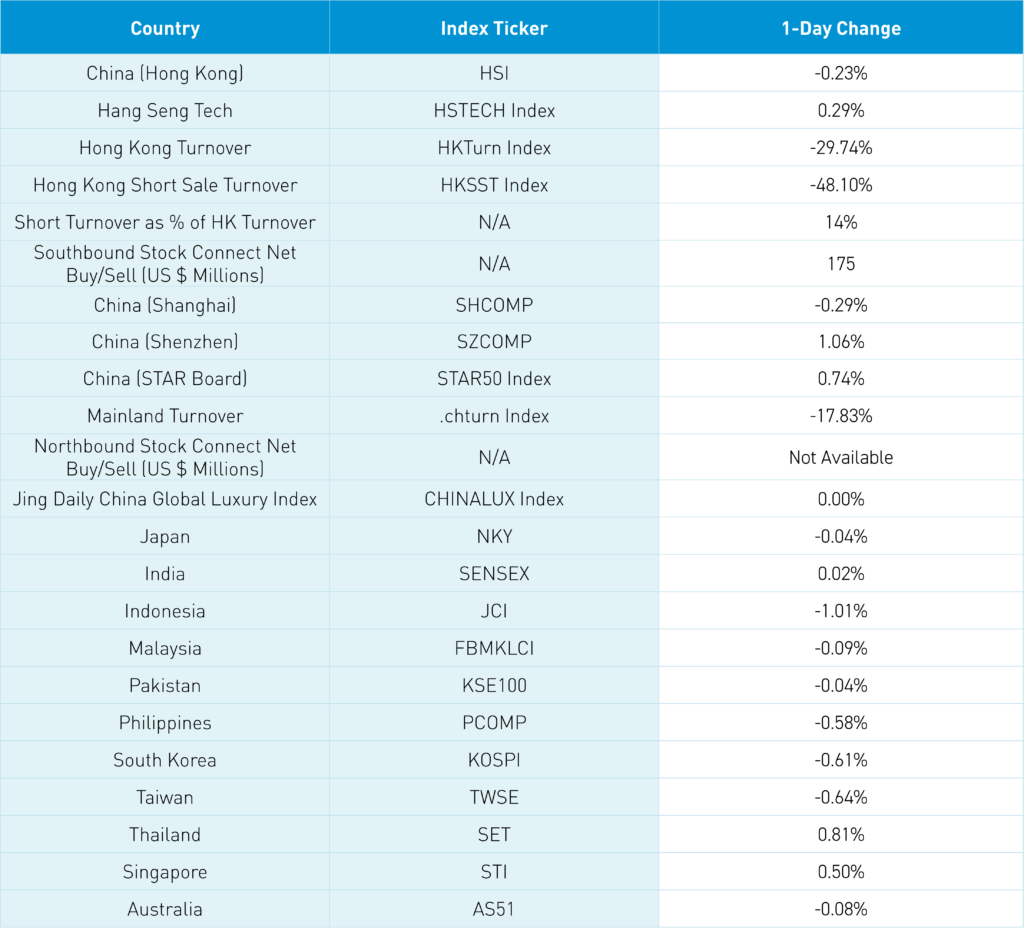

Asian equities were largely lower on light volumes and a stronger US dollar.

Yesterday, Hong Kong and Mainland China were hit on profit-taking after Friday’s strong move, with the Hang Seng down –1.31%, Hang Seng Tech down -1.74%, and Shanghai and Shenzhen markets down -1.1% and -1.91%. Friday’s move was impressive as China was a net sell in MSCI indices as Alibaba’s three-year regulatory review ended.

Bank stock underperformed yesterday and today on the massive proposed RMB 5.4 trillion mortgage refinancing that would benefit households by weighing on banks’ profitability. Western headlines point to weak economic data, though decide for yourself as July’s “official” Manufacturing PMI was 49.1 versus expectations of 49.5 and July’s 49.4, Non-Manufacturing was 50.3 versus expectations of 50.1 and July’s 50.2. Caixin's July China Manufacturing PMI was 50.4 versus expectations of 50 and July’s 49.8. PMIs are a diffusion index with over 50 indicating month-over-month growth and under 50 indicating month-over-month contraction. The “official” PMI is a numerically large survey of large companies conducted by the National Bureau of Statistics while the Caixin survey is a smaller sample size and private companies conducted by S&P.

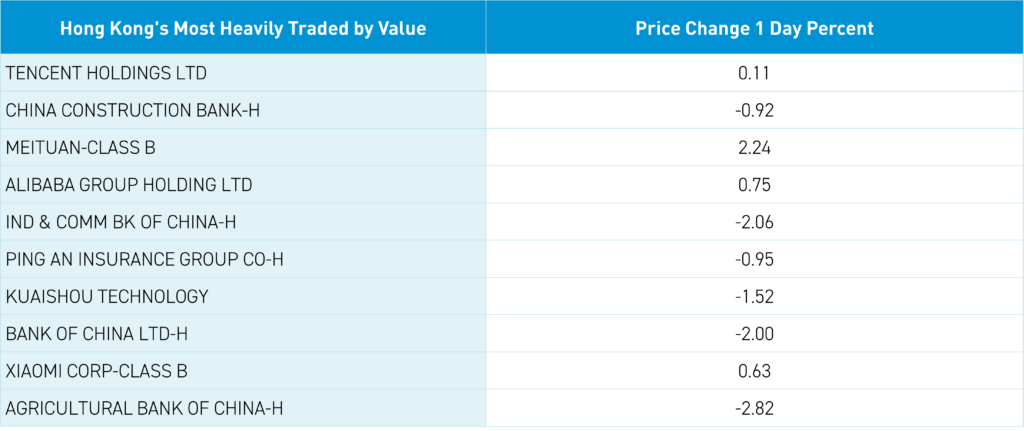

Today, growth stocks rebounded on very light volumes led by Hong Kong’s most heavily traded stocks by value, including Tencent which gained +0.11% (down -1.1% yesterday) despite buying back 2.65 million shares today, China Construction Bank which fell -0.92% (down -1.63% yesterday), Meituan which gained +2.24% (down -1.61% yesterday), Alibaba which gained +0.75% (down -2.39% yesterday), and ICBC which fell -2.06% (down -2.67% yesterday). Mainland growth stocks also rebounded today, with Shenzhen closing higher by +1.06%, though Shanghai, weighed down by the banks, closed just above the psychologically important 2,800 level. There is some chatter that the new iPhone16 isn’t compatible with Tencent’s WeChat, which would make it impossible to sell in China due to the popularity of the app.

Asset management news source Fundfire wrote about US pensions de-risking their portfolios and selling their non-US positions due to their underperformance over the last 15 years. One consultant quoted in the article called the capitulation “fatigue,” especially for “….those that have gone into emerging markets or international small capitalization.” The article notes several large international equity mandates being terminated as the All Country World ex-US equity strategies have seen $49 billion of outflows in the last five years. The article notes that many pensions are reallocating to fixed income due to higher US interest rates, leading to liquidating US equity-focused strategies. Over the last five years, US equity strategies have seen -$385 billion of outflows while fixed income has seen $178 billion of inflow. Is this a sign of a bottom in non-US stocks? We shall see!

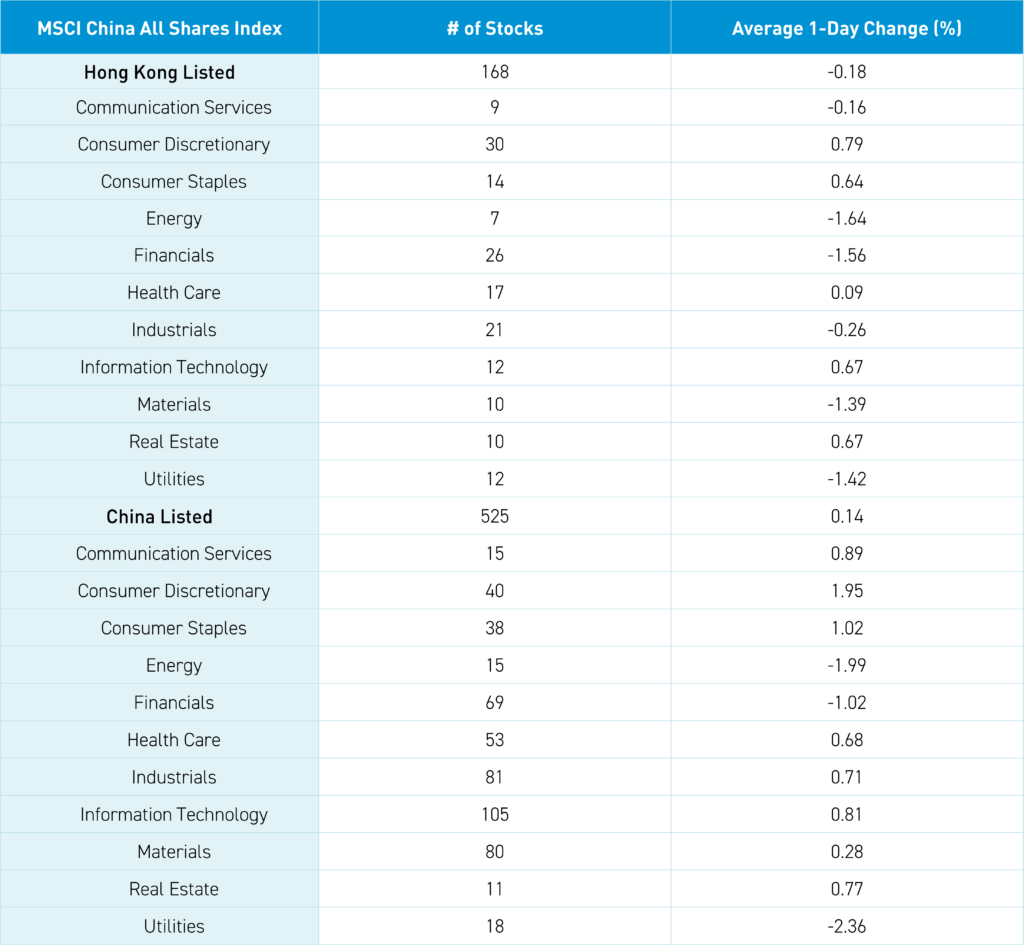

The Hang Seng and Hang Seng Tech diverged -0.23% and +0.29%, respectively, on volume down -29.74% from yesterday, which is 77% of the 1-year average. 217 stocks advanced while 247 declined. Main Board short turnover fell by -48% from yesterday, which is 66% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Growth and small capitalization stocks outperformed value and large capitalization stocks. The top sectors were consumer discretionary, up +0.79%, technology, up +0.68%, and real estate, up +0.67%, while energy fell -1.63%, financials fell -1.55%, and utilities fell -1.47%. The top sub-sectors were retailing, consumer durables, and semiconductors, while technical hardware, banks, and utilities were the worst. Southbound Stock Connect volumes were light as Mainland investors bought $175 million of Hong Kong stocks and ETFs with Tencent a small net buy.

Shanghai, Shenzhen, and the STAR Board diverged -0.29%, +1.06%, and +0.74%, respectively, on volume down -17% from yesterday, which is 73% of the 1-year average. 3,486 stocks advanced, while 1,331 declined. Growth and small capitalization stocks outperformed value and large capitalization stocks. The top sectors were consumer discretionary, up +1.94%, consumer staples, up +1.01%, and communication services, up +0.88%, while utilities fell -2.37%, energy fell -2%, and financials fell -1.03%. The top sub-sectors were education, office supplies, and software, while oil/gas, power industry, and banking were the worst. Northbound Stock Connect volumes were moderate/light. CNY and the Asia dollar index were off versus the US dollar. Treasury bonds rallied. Copper and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.09 Friday

- CNY per EUR 7.86 versus 7.86 Friday

- Yield on 10-Year Government Bond 2.14% versus 2.17% Friday

- Yield on 10-Year China Development Bank Bond 2.24% versus 2.27% Friday

- Copper Price: -0.47%

- Steel Price: -1.69%