NPC Stimulus to Exceed Expectations? Why Smoot Hawley 2024 Isn’t Going to Happen

4 Min. Read Time

Key News

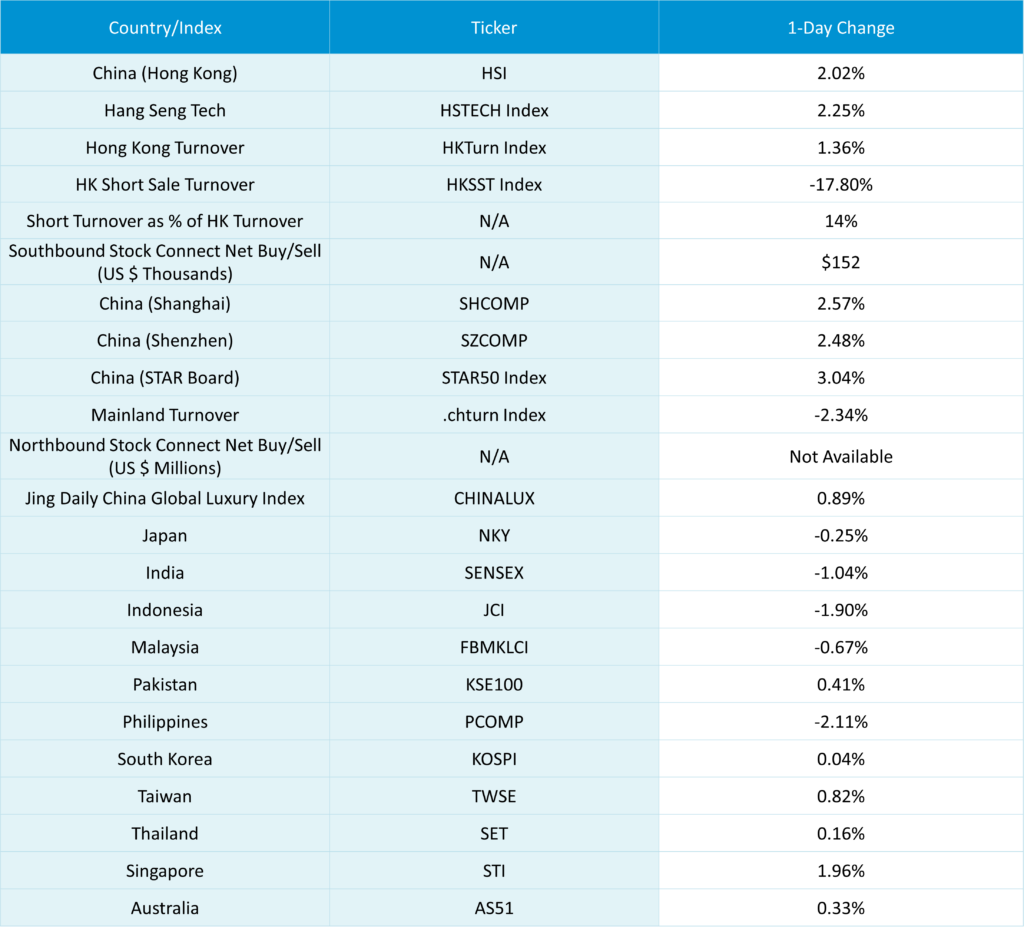

Asian equities were mixed overnight as Singapore, Hong Kong, and Mainland China outperformed while India, the Philippines, and Indonesia underperformed.

Hong Kong and Mainland China opened lower but went from lower left to upper right/grinding higher all day on strong volumes, and strong breadth/advancers beat decliners handily. Several key catalysts are at play:

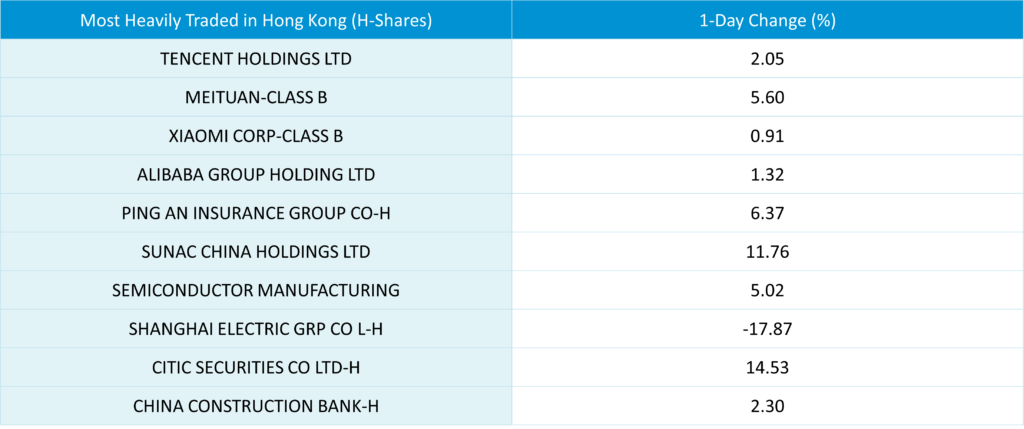

- Chatter that NPC fiscal stimulus could be more significant than anticipated on the low end of between RMB 2 trillion to RMB 6 trillion while the high end of the range of RMB 10 trillion to address local governments’ hidden debts, real estate support, and bank capital injection. Based on the Ministry of Finance press conference on Saturday, October 12th, we estimate approximately RMB 8 trillion. Overnight chatter was an additional RMB 2 trillion focused on consumption, which will also be included. I do not believe this has anything to do with Trump winning and potential tariffs. The Chinese government needs to get domestic consumption as low consumer confidence is bad for any politician. There is also a rumor that the NPC press conference could occur during Chinese market hours to ensure that the stock market reacts. I don’t see a time for the NPC press conference officially set. The rumor increased domestic consumption stocks, including Hong Kong internet, retailers and food/staples, while strong Mainland sub-sectors included liquor stocks, retailers, and restaurants. Hong Kong e-commerce stocks did well, with Alibaba +2.05%, JD.com +1.05%, and Meituan +5.6%, outperforming on its pure China revenue exposure.

- October exports beat +12.7% versus September’s +2.4% and economist expectations of +5%, while imports fell -2.3% versus September’s +0.3% and expectations of -2%. Remember, imports are highly influenced by China’s purchase of commodities and their price since the percentage change is driven by the value of commodities versus the tons imported. With all that said, October commodity imports by tons did decline.

- PBOC Pan Shiyi hosted leaders of foreign financial institutions to reiterate access to China’s financial markets, listen to “opinions and suggestions, and exchanged responses to concerns.” He told the group that China’s economic potential “has not changed,” especially after “the release and implementation of a package of financial incremental policies.” Foreign ownership rules have been relaxed.

- The Shanghai Stock Exchange reported 6.85 million new brokerage accounts opened in October, raising the year-to-date total to 20.31 million. Mainland media noted this was the third-highest monthly total ever. Do you think this is a good sign for markets? Me too. Remember though, the government is saying buy stocks if stocks don’t go up……….

- President Xi sent President Trump a congratulatory letter. With the campaign over, have you noticed several Trump economic advisors tempering tariff talk? Reuters has a good article on US farmers who voted for Trump, voicing concern that their biggest client will shift purchases to Brazil—targeted tariffs on goods receiving Chinese government subsidies? 100%. Broad 60% tariffs? Maybe threatened, but implemented highly unlikely IMO. Broad 60% tariffs would replicate the economic policies from the worst economic period in American history. THE GREAT DEPRESSION. Seriously, dust off your copy of The Grapes of Wrath to remember what that was like. Ask President Hoover and Senators Smoot and Hawley what history thinks of their legacies. (Not surprisingly, none were reelected in 1932, as an FYI).

Mainland investors only bought $152mm of Hong Kong stocks today, favoring Hong Kong growth stocks while taking quick profits in the Hong Kong Tracker ETF. Southbound turnover accounted for 48% of Hong Kong turnover today!

After the US close yesterday, MSCI released the pro forma for the upcoming Semi-Annual Index Review (SAIR), which takes effect at the close on November 30th. Index and ETF managers must implement additions/deletions by trading at the close on November 30th to ensure their holdings match the index holdings. The United States’ 2,332 stocks will account for 63.9% of All Country World Index, while the 3,272 stocks within Emerging Markets will account for 10.6% of the weight. To be considered a large-cap US stock, the market cap needs to be $39b, though in Europe, $21B, $19B in Japan, and $9.8B in EM.

Since the August SAIR, MSCI Hong Kong has been the best-performing Developed Market country, while China was the #2 best-performing EM country behind Thailand. MSCI China will be 26.8% of the EM index, comprised of 582 stocks, versus the current allocation of 27%, comprised of 598 stocks. Because the Chinese market rallied, the minimum market cap threshold increased, paradoxically leading to the deletion of 20 stocks. India will move up a touch to 156 stocks at a 19.8% weight from the current 151 stocks at a 19.3% weight.

The Hang Seng and Hang Seng Tech gained +2.02% and +2.25% on volume +1.3% from yesterday, which is 177% of the 1-year average. 401 stocks advanced while 106 declined. Main Board short turnover decreased -17.8% from yesterday, which is 160% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging).

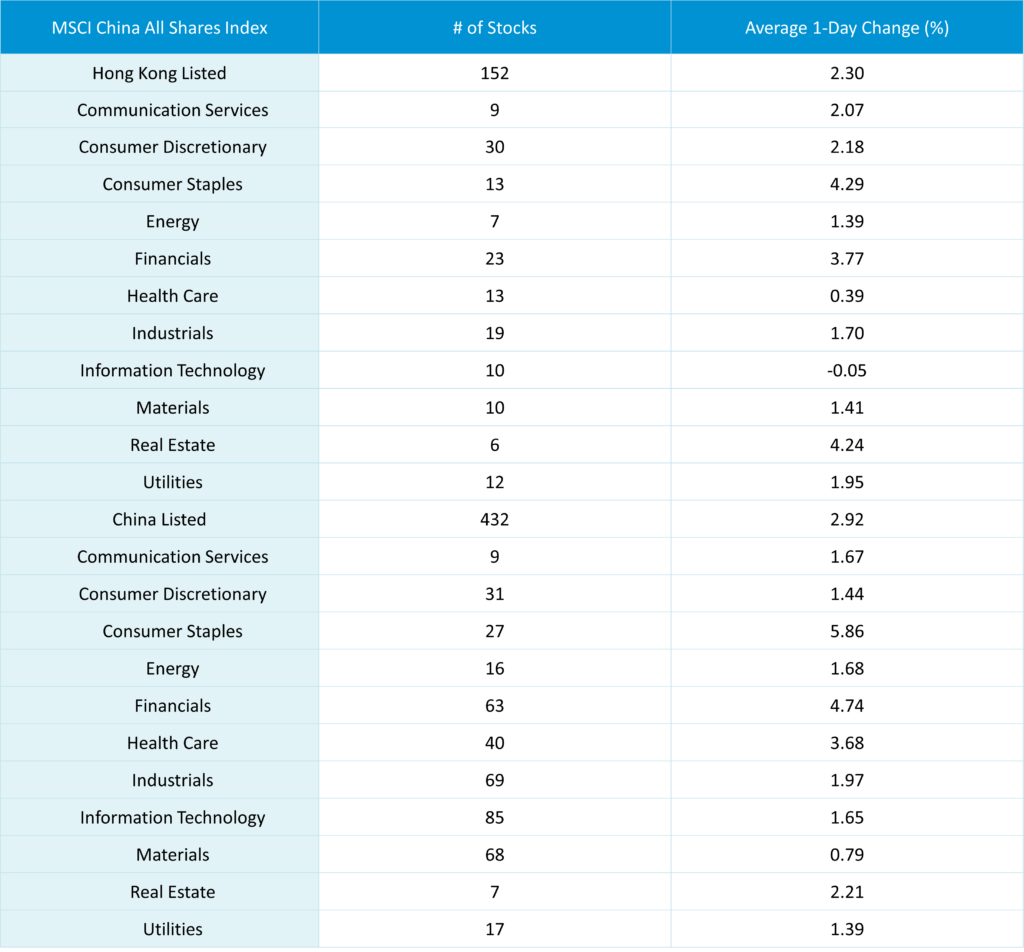

Growth and large caps outperformed value and small caps. All sectors were positive: staples +4.28%, real estate +4.24%, and financials +3.76%. The top sub-sectors were diversified financials, consumer services, and insurance, while real estate and capital goods were the worst. Southbound Stock Connect volumes were high/2X pre-stimulus average as Mainland investors bought $152mm of Hong Kong stocks and ETFs with Tencent, Meituan, and Alibaba moderate net buys, Xiaomi, Suanc, and SH Electric small net buys while Hong Kong Tracker ETF a large net sell.

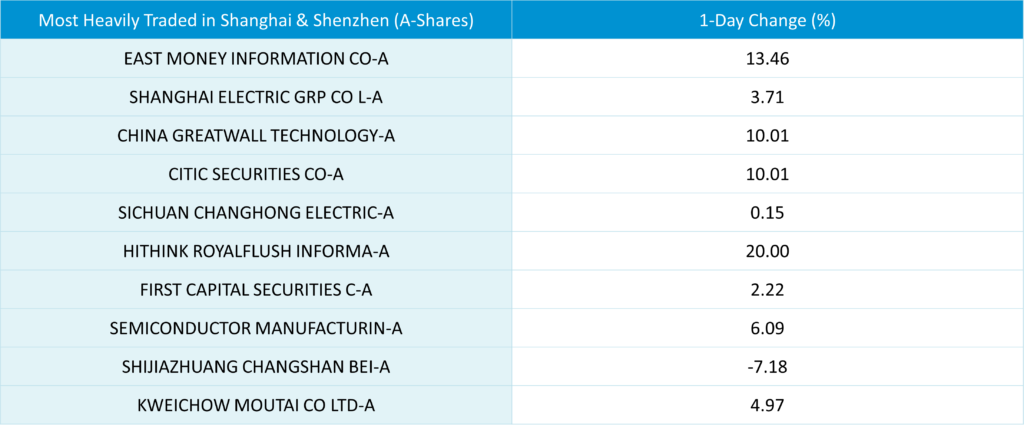

Shanghai, Shenzhen, and STAR Board gained +2.57%, +2.48%, and +3.04% on volume -2.34% from yesterday, which is 275% of the 1-year average. 4,348 stocks advanced, while 716 declined. Value and Large caps outpaced growth and small caps. All sectors were positive: staples +5.83%, financials +4.71%, and healthcare +3.66%. The top sub-sectors were securities, liquor, and insurance, while precious metals, aerospace/defense, and motorcycles were the worst. Northbound Stock Connect volumes were very high/2X pre-stimulus levels. CNY and the Asia dollar index were stronger versus the US dollar. Steel and copper fell.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.16 versus 7.16 yesterday

- CNY per EUR 7.70 versus 7.70 yesterday

- Yield on 10-Year Government Bond 2.11% versus 2.12% yesterday

- Yield on 10-Year China Development Bank Bond 2.19% versus 2.20% yesterday

- Copper Price -1.92%

- Steel Price -0.06%