City Consumer Voucher Rollout Raises Related Stocks

3 Min. Read Time

Key News

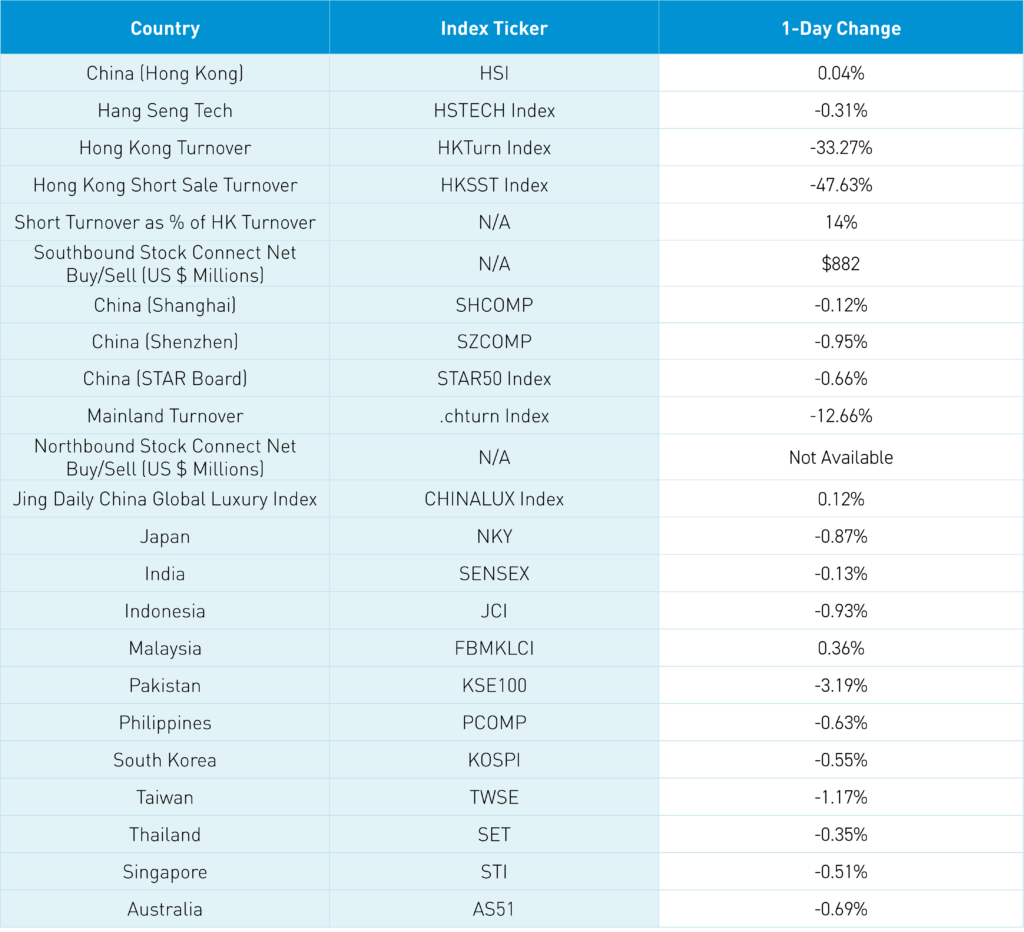

Asian equities were a sea of red except for Hong Kong, which managed to end in the green.

President Trump’s tariff threat on China, Canada, and Mexico (if they don’t address drug and immigration) roiled Asia markets, and the Bessent nomination rally lasted a day.

Stepping up fentanyl ingredient export controls is an area in which the US and China are apt to find common ground, having done so previously, i.e., an easy win. By far the most important item today and arguably this month that you aren’t going to read anywhere else is the increase in Mainland chatter about major cities issuing consumer vouchers and the potential expansion of the trade-in policy beyond autos and home appliances. Consumer stocks such as tourism, restaurants, and liquor outperformed in both Mainland China and Hong Kong on reports major city governments issued consumer vouchers on Sunday to spur consumption during the holiday season. The focus of the vouchers varied by city. Shanghai’s vouchers were geared toward restaurants, hotels, and tourism sites. Meanwhile, Hangzhou and Guangzhou's vouchers were for restaurants. Beijing, on the other hand, issued vouchers for winter sports and tourism.

The National People's Congress (NPC) press conference insinuated that the trade-in policy will likely be expanded, with details potentially coming from the mid-December China Economic Work Conference (CEWC).

Last week, in Asia, a Chinese economist proposed that China should focus on addressing the structural issues that have led to a high savings rate, such as the lack of a social safety net and the inequalities facing the very large migrant worker population. Maybe they do both?

Real estate was a top-performing sector after the China Index Academy reported a strong uptick in transactions last week, up +11.75% month-over-month (MoM) and +6.26% year-over-year (YoY). First-tier cities gained +12.33% MoM and +32.09% YoY, and Shanghai gained +50.1% MoM. Separately, the Shenzhen Real Estate Agency Association announced that 2,132 second-hand homes were sold last week, up +8.8% week-over-week. Raising home prices would help lift consumer confidence and potentially domestic consumption.

Apple and Huawei’s ecosystems were mixed as Trump’s tariff threat offset Tim Cook’s second China visit this month and the launch of Huawei Mate 70, which includes the ability to call via satellite. The Mate 70 costs RMB 5,499 ($827) to RMB 6,999 ($965), while the Mate 70 Pro runs from RMB 6,499 ($896) to RMB 7,999 ($1,103).

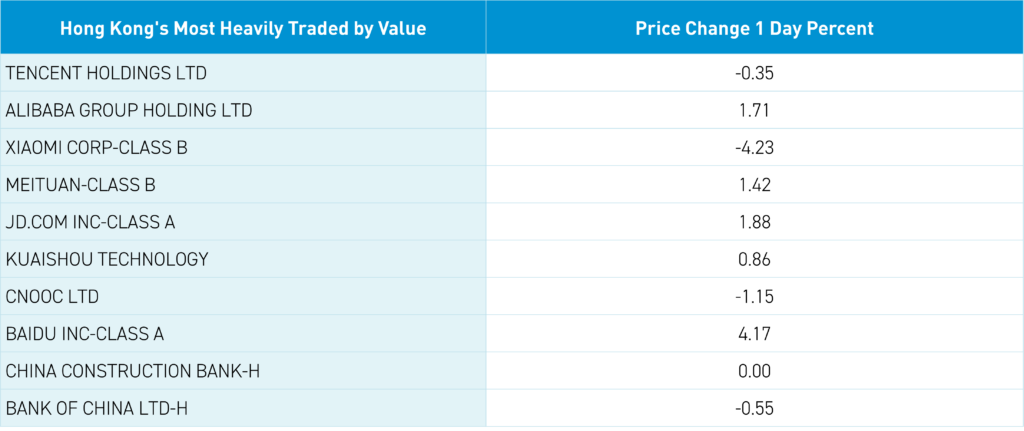

There was some chatter that the bank reserve requirement ratio would be cut again. Hong Kong internet stocks, except for Tencent, which was down -0.35%, and Trip.com, which was down -0.20%, outperformed as Alibaba gained +1.17%, Meituan gained +1.42%, JD.com gained +1.88%, and Baidu gained +4.17%.

Electric vehicle (EV) stocks were weak after Bloomberg News stated that an EV tariff compromise is not a done deal, though a sell-side analyst downgraded the sector. Mainland investors bought a healthy $882 million worth of Hong Kong-listed stocks and ETFs today, though Southbound Connect was only 31% of Hong Kong turnover versus the 40% average. Mainland China gave up day-long gains in a late afternoon slump. National Team ETFs continue to see blow average volumes as Mainland Chinese equities must feel like George Custer (where’s the cavalry?). Volumes were very light following yesterday’s MSCI index rebalance. Great to see several positives occurring under the radar.

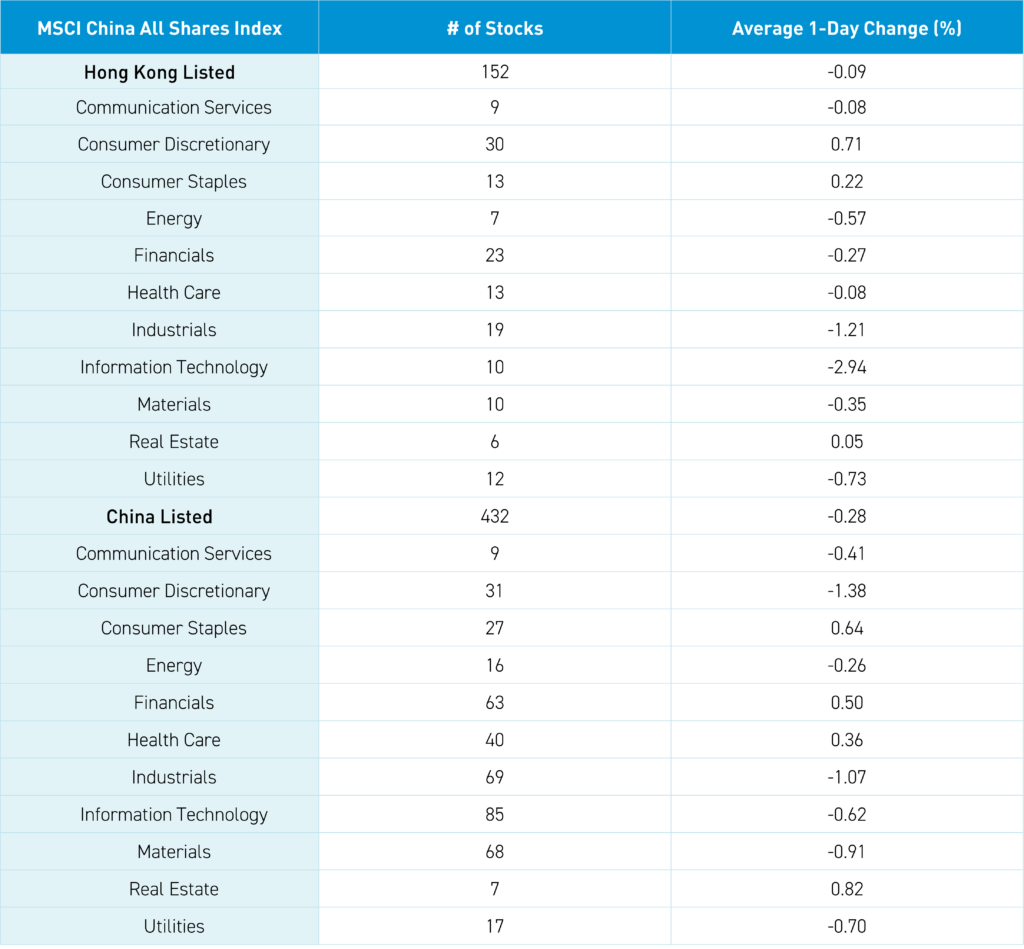

The Hang Seng and Hang Seng Tech indexes diverged to close +0.40% and -0.31%, respectively, on volume that decreased -33% from yesterday, which is 96% of the 1-year average. 217 stocks advanced, while 265 declined. Main Board short turnover decreased by -47% from yesterday, which is 86% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and large capitalization stocks outperformed (i.e. fell less than) the value factor and small capitalization stocks. The top-performing sectors were consumer discretionary, which was up +0.71%, consumer staples, which was up +0.22%, and real estate, which was up +0.05%. Meanwhile, the worst-performing sectors were Information Technology, which fell -2.94%, Industrials, which fell -1.21%, and Utilities, which fell -0.73%. The top-performing subsectors were conglomerates, materials, and food. Meanwhile, technical hardware, media, and household products were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors bought a net $882 million worth of Hong Kong-listed stocks and ETFs, including the Hong Kong Tracker ETF, which was a large net buy, China Mobile, Alibaba, Tencent, Meituan, and Yidu Technology.

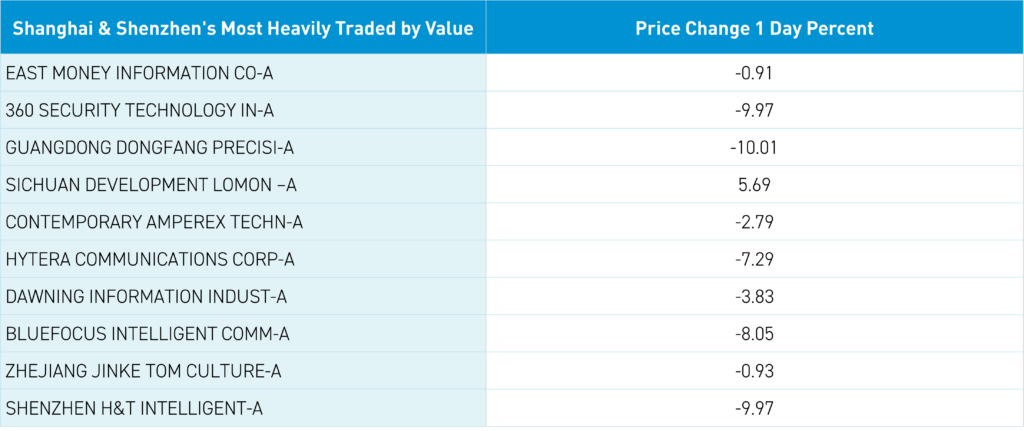

Shanghai, Shenzhen, and the STAR Board all closed lower by -0.12%, -0.95%, and -0.66%, respectively, on volume that decreased -12.66% from Friday, which is 135% of the 1-year average. 1,494 stocks advanced, while 3,490 declined. The value factor and large capitalization stocks fell less than the growth factor and small capitalization stocks. The top-performing sectors were Real Estate, which gained +0.82%, Consumer Staples, which gained +0.64%, and Financials, which gained +0.6%. Meanwhile, Consumer Discretionary fell -1.38%, Industrials fell -1.07%, and Materials fell -0.91%. The top-performing subsectors were office supplies, leisure products, and catering. Meanwhile, education, chemicals, and computer hardware were among the worst-performing. Northbound Stock Connect volumes were just above average. CNY and the Asia Dollar Index fell versus the US dollar. Treasury bonds were flat. Copper fell while steel gained.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.25 versus 7.24 yesterday

- CNY per EUR 7.61 versus 7.62 yesterday

- Yield on 10-Year Government Bond 2.07% versus 2.07% yesterday

- Yield on 10-Year China Development Bank Bond 2.14% versus 2.14% yesterday

- Copper Price -0.15%

- Steel Price +0.09%