China’s GDP Hits An All-Time High, Week In Review

6 Min. Read Time

Week in Review

- Asian equities had a mixed week, though, after the US CPI print, Hong Kong and Mainland China outperformed.

- China's imports increased +1% in December after falling -4% in November.

- The Ministry of Commerce issued an “Implementation Plan for the Purchase Subsidy of Mobile Phones, Tablets, Smart Watches,” as consumers will receive a 15% discount on new purchases up to RMB 500 as long as the device doesn’t exceed RMB 6,000.

- Comments from policymakers helped fuel a slight market rally as the China Securities Regulatory Commission (CSRC), China’s SEC, vowed to develop more market stabilization mechanisms.

- Mainland investors bought a healthy $1.069 billion today, bringing the weekly total to an impressive $5.486 billion.

China Economic Data Update

- Q4 GDP was 5.4% versus analyst estimates of 5% and Q3’s 4.6%.

- China’s GDP hit an all-time high of RMB 134.9 trillion, exceeding RMB 130 trillion for the first time.

- 2024 GDP is 5% versus the estimated 4.9% and 2023’s 4.8%.

- December Industrial Production was 6.2% versus the estimated 5.4% and November’s 5.4%.

- December's retail sales were 3.7% versus the estimated 3.6% and November’s 3%.

- 2024 Online Retail Sales gained +7.2% year-over-year (YoY).

- December's Fixed Asset Investment was 3.2% versus the estimated 3.3% and November’s 3.3%.

- 2024 Property Investment was -10.6% versus the estimated -10.4% and 2023’s -10.4%.

- 2024 Residential Property Sales were -17.6% versus 2023’s -20%.

- December New Home Prices were -0.08% versus November’s -0.2%.

- December Used Home Prices were -0.31% versus November’s -0.35%.

- China’s population declined -0.99% to 1.408 billion, a decrease of 1.39 million YoY.

- Urbanization rate increased by +0.84% to 67%.

There is no commentary, as the numbers speak for themselves. What’s the positioning of global investors to China’s economic rebound? What’s China's weight in US wealth management models? What does EPFR data tell us about active funds position in China today? What does prime brokerage data tell us about China's position amongst hedge funds (less a select few)?

Insights from the National Bureau of Statistics Q&A with reporters

- The statement acknowledged that “domestic demand is insufficient” and that the economy faces “many difficulties and challenges,” which is a good sign as the government is aware of the issues.

- China’s GDP hit an all-time high of RMB 134.9 trillion, exceeding RMB 130 trillion for the first time. Investors are infatuated with % GDP, though shouldn’t we focus on the value of growth? I’ve long argued that, yes, China’s GDP will not grow by a high percentage, but that’s like Yankee fans saying the Bronx Bombers stink. The Yankees have 27 World Series! Yes, they haven’t won a title since 2009.

- Recent stimulus is working. The “package of policies has effectively boosted social confidence,” as the government recognized “large downward pressure on the economy,” leading the Central Committee to make a “decisive deployment of a package of incremental policies, which greatly boosted confidence, stimulated vitality and promoted economic recovery.”

- CPI’s decline is mainly due to food prices falling, though core CPI “has continued to rise.” Food prices fell by -0.6% YoY. They expect CPI to increase in 2024 due to the “implementation of macro policies”

- “Real estate is a very concerning issue,” which led the Central Committee on September 26th to promote the real estate market to keep it from falling further and stabilize. A host of policies were introduced by government agencies to “improve land, tax, finance, and other policies, canceled the standards of purchase restrictions, sales transactions, price restrictions and ordinary residential and non-ordinary residential, reduced the housing fund loan interest rates, housing loan down payment ratio, existing loan interest rates and the tax rates of exchange of housing, and worked together to launch a policy package.” Prices are “gradually” stabilizing.

- When asked by Reuters how they will boost domestic demand, the response was, “We are confident in China’s economic development in 2025” because “the first priority of economic work in 2025 is to expand domestic demand, especially to boost resident consumption comprehensively.”

- Recognized unemployment for migrant workers and young people, which the government is “very concerned about” as “employment is the foundation of people’s livelihood and the source of income,” which is why it is a top priority. Separately, it was reported that Premier Li held a State Council meeting “to study relevant policies and measures to promote employment.”

Key News

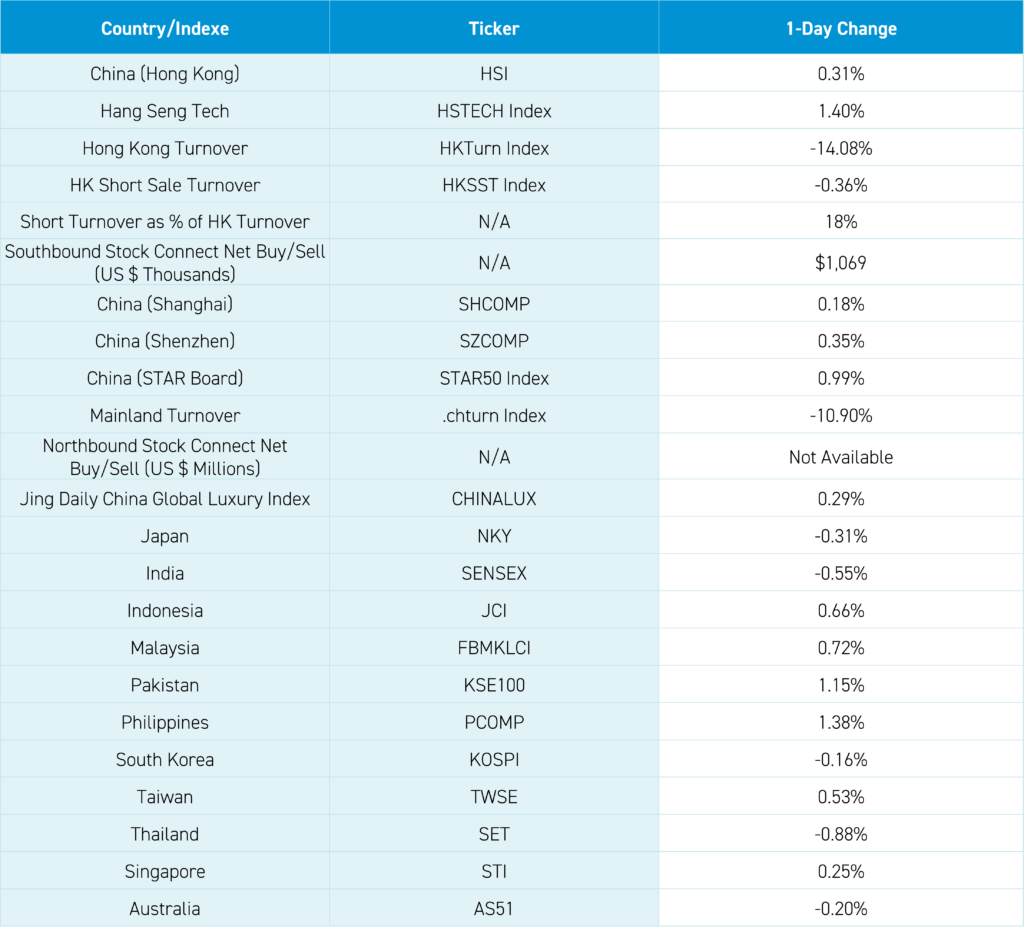

Asian equities ended the week mixed as the Philippines outperformed, though, for the week, Hong Kong and Mainland China outperformed, while Japan and India, beneficiaries of the exodus out of China, were down for the week.

Since Chinese internet stocks bottomed on January 22, 2024, they’ve outperformed MSCI Japan by 20%, MSCI India by nearly 15%, and just lagging behind the S&P 500. After Asia closed, the WSJ reported that President Xi will send Vice President and Confident Han Zheng to attend the inauguration. I agree with the article, “Beijing is likely to follow up on Han’s trip by looking to arrange high-level meetings with the Trump Administration.” If President Xi walked out onto the inauguration stage on Monday, imagine what Chinese stocks would do on Tuesday?!

Also, after the close, the Ministry of Commerce and seven other agencies announced that the new car purchase subsidies would be extended in 2025. Electric vehicle (EV)/hybrid purchases get a RMB 20,000 subsidy while gas cars receive RMB 15,000. Let’s see if China EV ADRs pop in US hours.

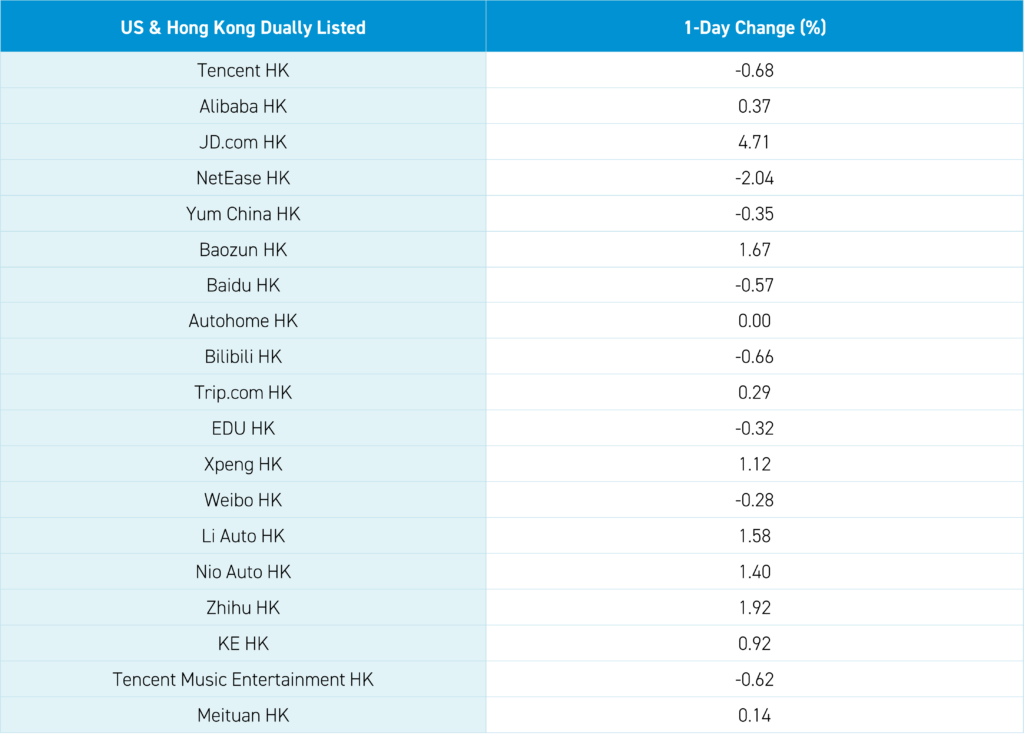

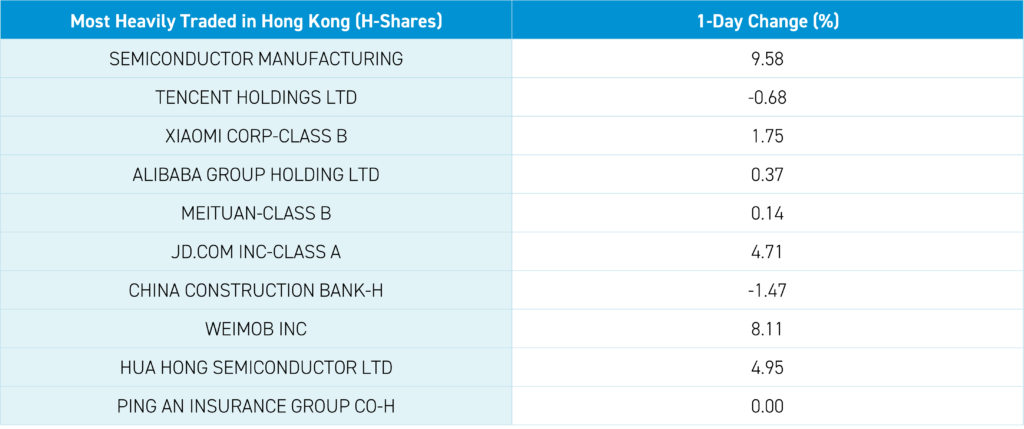

Chinese economic data lifted Hong Kong and Mainland China, though volumes were light, which is too bad. Consumer plays such as Alibaba, gained +0.37%, and JD.com, gained +4.71%, on reports they will offer a gifting option. Meituan gained +0.14%, and Trip.com gained +0.29%, though Tencent fell -0.68% and Netease fell -2.04% after a nice run recently.

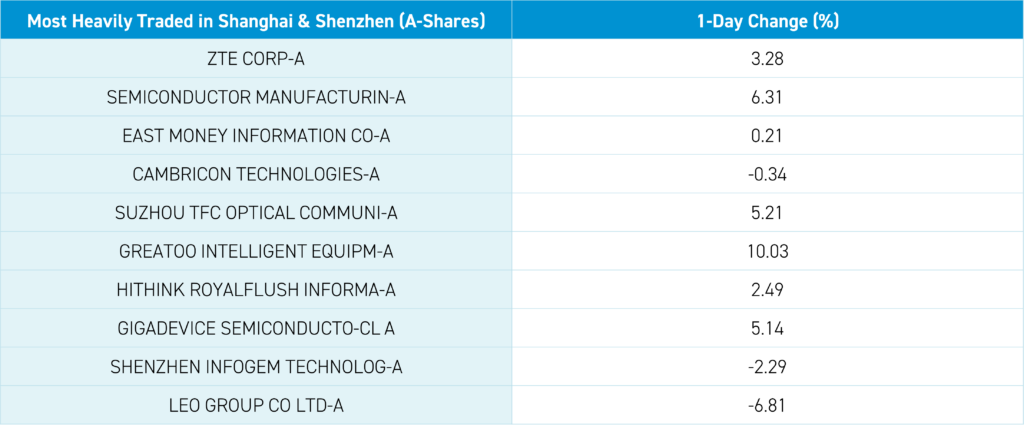

Semiconductor stocks were led higher by SMIC, which gained +9.58%, as the Chinese government looks at US semiconductor subsidies. Tech hardware did not react as strongly to the new consumption subsidies, though ZTE gained +7.53%, Xiaomi gained +1.75%, AAC was flat, and Sunny Optical fell -0.55%.

Banks and energy stocks were weak. Mainland investors bought a healthy $1.069 billion today, bringing the weekly total to an impressive $5.486 billion. Growth outperformed value stocks as Mainland banks and energy were weak, though insurance, heavy weights Kweichow Moutai, which gained +0.58%, food-related stocks, BYD, which gained +1.41%, CATL, which gained +0.63%, and semiconductor stocks had a strong showing. Year-to-date (YTD), Hong Kong and Mainland China are off though let’s see if things get going from here. Per yesterday’s note on my recent Hong Kong/Mainland China trip, real estate is a big issue though the government recognizes it.

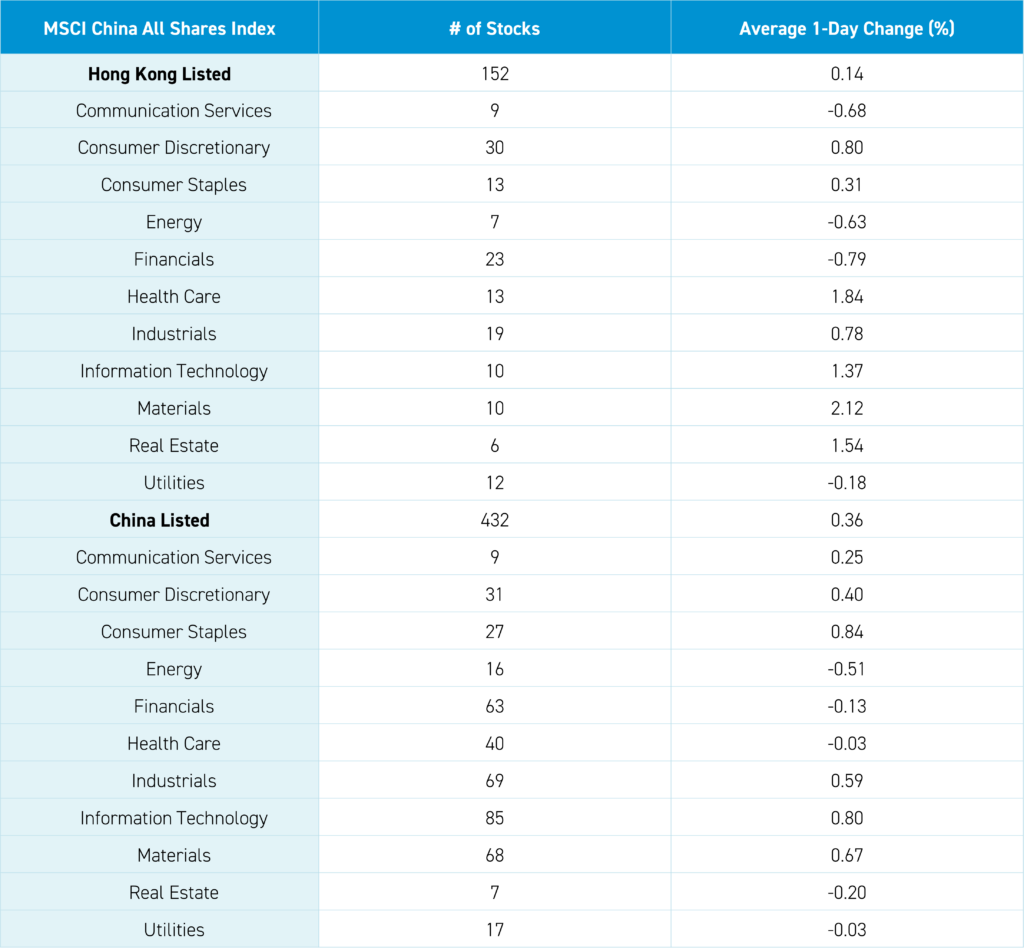

The Hang Seng and Hang Seng Tech gained +0.31% and +1.40%, respectively, on volume down -14.08% from yesterday, which is 90% of the 1-year average. 276 stocks advanced, while 196 declined. Main Board short turnover increased by +18% from yesterday, which is 107% of the 1-year average, as 18% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). Value and small capitalization stocks gained more than growth and large capitalization stocks. The top sectors were materials, up +2.12%, healthcare, up +1.84%, and real estate, up +1.54, while financials fell -0.78%, communication services fell -0.68%, and energy fell -0.63%. The top sub-sectors were semiconductors, consumer durables, and nonferrous metals, while steel, petroleum, and banks were the worst. Southbound Stock Connect volumes were at 1.5X pre-stimulus levels as Mainland investors bought $1.069 billion of Hong Kong stocks and ETFs, with SMIC a large net buy, Tencent a large/moderate net buy, Meituan a moderate net buy, Xiaomi and Weimob were small net buys, ZTE, while Hua Hong Semi and Alibaba were small net sells.

Shanghai, Shenzhen, and STAR Board gained +0.18%, +0.35%, and +0.99%, respectively, on volume down -10.9% from yesterday, which is 105% of the 1-year average. 2,560 stocks advanced, while 2,332 declined. Growth and small capitalization stocks gained more than value and large capitalization stocks. The top sectors were consumer staples, up +0.84%, technology, up +0.8%, and materials, up +0.67%, while energy fell -0.51%, real estate fell -0.2%, and financials fell -0.13%. The top sub-sectors were motorcycles, fertilizer, and soft drinks, while leisure products, retail, and cultural media were the worst. Northbound Stock Connect volumes were just above average. CNY and the Asia dollar index were slightly higher versus the US dollar. The Treasury bond curve steepened. Copper and steel rose.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.32 versus 7.33 yesterday

- CNY per EUR 7.54 versus 7.54 yesterday

- Yield on 10-Year Government Bond 1.66% versus 1.64% yesterday

- Yield on 10-Year China Development Bank Bond 1.68% versus 1.67% yesterday

- Copper Price +0.62%

- Steel Price +1.15%