Alibaba Goes Ballistic, Finance Minister Talks Consumption, Week In Review

7 Min. Read Time

Week in Review

- Asian equities were mostly higher this week as Mainland China and Hong Kong outperformed while Australia and Thailand underperformed.

- It was a busy week for earnings as Alibaba beat estimates on the top and bottom line on strong cloud and E-Commerce results, Baidu beat on search resilience, NetEase beat on bottom line profit only, Bilibili achieved its first profitable quarter, and Vipshop beat on its top line revenue.

- Humanoid robots were a theme in the markets this week, as multiple companies rumored to be developing the technology gained.

- President Trump said he was mulling a grand deal with China and called his relationship with Xi "a great one".

Key News

Asian equities ended a positive week on a high note, led by Hong Kong and Mainland China-listed growth stocks following Alibaba’s financial results, which were reported after the close in Hong Kong yesterday. Meanwhile, India was a rare underperformer for the day and for the week. Could investors be using India as a funding source for a re-allocation to China?

Mainland media is reporting that China’s trade envoy He Lifeng spoke with the US Treasury Secretary Scott Bessent this morning. China’s release stated that "Both sides agreed on the importance of China-US economic and trade relations and agreed to continue communication on issues of mutual concern." Maybe Bessent, not Lutnick, is taking the lead on trade negotiations?

As we stated yesterday, Premier Li presided over a State Council meeting, where he stated that the government would continue its campaign of "consistently promoting consumption and benefiting people's livelihood, vigorously boosting consumption, and expanding domestic demand".

Today, it was reported that Ministry of Finance Chief Lan Fo An was quoted in The People’s Daily stating that China needs to "Implement a more active fiscal policy to promote the continuous recovery and improvement of the economy". He stated that fiscal policy should focus on:

- Increasing the fiscal deficit rate

- Increasing expenditure

- Issuing more government bonds

- "Vigorously optimizing the expenditure structure, promoting consumption and increasing momentum”

- Resolving risks in key areas

- Increasing transfers to local governments

The article dives deeper into each of the points, all of which are very strong signals going into the legislatively important “Dual Sessions”, which is scheduled to begin on March 5th. Maybe the message was received?

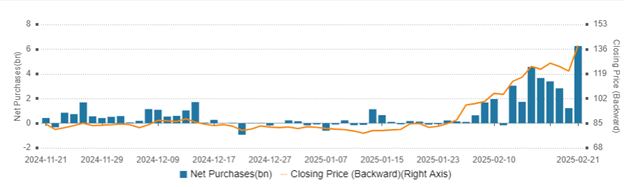

Alibaba’s Hong Kong share class gained +14.56% versus its US listing’s gain of only +8.09% yesterday, on massive value of volume traded, which reached HKD 44.5 billion ($5.7 billion) versus the 1-year average of HKD 5.8 billion ($754 million) and volume of 329 million shares versus the 1-year average of 68 million shares! On an “average” day, Hong Kong’s most heavily traded stock by value would trade around HKD 5 billion. Mainland investors bought an impressive HKD 6 billion worth of Alibaba via Southbound Stock Connect, following the better-than-expected financial results driven by China's E-Commerce, international E-Commerce, and their cloud computing unit, as AI drives adoption.

It is worth noting local investors’ optimism versus their US counterparts. Bilibili’s Hong Kong share class, which also reported after the close yesterday, gained +16.47% overnight versus its US listing’s gain of only +8.76%.

Hong Kong-listed growth names and related AI plays led the market higher, including Tencent, which gained +6.2%, Xiaomi, which gained +5.19%, Meituan, which gained +3.82%, Semiconductor Manufacturing International (SMIC), which gained +7.86%, and Kuiashou, which gained +7.35%.

Meanwhile, Health Care had a strong day, along with insurance and stockbrokers. However, coal, oil, and precious metals were among the rare decliners. Hong Kong’s volumes were 2.5X the 1-year average, owing to $1.81 billion worth of net buying from Mainland investors via Southbound Stock Connect.

Mainland China was also led higher by growth stocks, the STAR Board, and AI-related stocks and subsectors such as semiconductors, telecom, electronic devices, the electric vehicle (EV) ecosystem (BYD gained +5.57% and CATL gained +1.98% on the extension of Shenzhen’s RMB 15,000 EV subsidy), life sciences, and pharmaceuticals. Mainland insurance also had a strong day. Mainland volumes exceeded RMB 2 trillion versus a 1-year average of RMB 1.1 trillion, though breadth was not quite as strong as in Hong Kong.

Alibaba's Hong Kong Share Price & Net Buy/Sell Via Southbound Stock Connect

Vipshop Q4 Earnings Overview

Apparel-focused E-Commerce platform Vipshop (VIPS US) reported earnings before the US market opened this morning.

- Revenue was RMB 33.2B ($4.6B) versus estimate of RMB 31.8B and Q4 2023’s RMB 34.7B

- Gross Merchandise Value (GMV) was RMB 66.2B versus Q4 2023’s RMB 66.4B

- Adjusted Net Income was RMB 3B ($407.4mm) versus estimate of RMB 2.753B and Q4 2023’s RMB 3.2B

- Adjusted EPS was RMB 5.70 ($0.78) versus estimate of RMB 5.25 and Q4 2023’s RMB 5.79

- The company repurchased US$43.3 million of its ADSs under its US$1.0 billion share repurchase program adopted in March 2023

- The company expects its total net revenues to be between RMB26.3 billion and RMB27.6 billion, representing a year-over-year decrease of approximately 5% to 0%

The Hang Seng and Hang Seng Tech indexes gained +3.99% and +6.53%, respectively, on volume that increased +38.62% from yesterday, which is 268% of the 1-year average. 314 stocks advanced, while 174 stocks declined. Main Board short turnover increased +40.1% from yesterday, which is 242% of the 1-year average, as 14% of turnover was short turnover (Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and large caps gained more than the value factor and small caps. The top-performing sectors were Consumer Discretionary, which gained +7.89%, Health Care, which gained +6.14%, and Information Technology, which gained +5.96%. Meanwhile, the worst-performing sectors were Energy, which fell -0.94%, Utilities, which fell -0.77%, and Materials, which fell -0.56%. The top-performing subsectors were semiconductors, consumer discretionary distribution, and technology hardware. Meanwhile, coal, paper, and construction materials were among the worst-performing subsectors. Southbound Stock Connect volumes were 4x pre-stimulus levels, as Mainland investors bought a net $1.81 billion worth of Hong Kong-listed stocks and ETFs, led by Alibaba, a very large net buy, Semiconductor Manufacturing, which was a large net buy, Tencent, Meituan, Kuaishou, Hua Hong Semi, and China Mobile. Xiaomi was a moderate a net sell.

Shanghai, Shenzhen, and the STAR Board gained +0.85%, +1.56%, and +5.97%, respectively, on volume that increased +24.81% from yesterday, which is 194% of the 1-year average. 2,702 stocks advanced while 2,298 stocks declined. The growth factor and large caps outperformed the value factor and small caps. The top-performing sectors were Communication Services, which gained +5.27%, Information Technology, which gained +4.39%, and Consumer Discretionary, which gained +1.46%. Meanwhile, the worst-performing sectors were Utilities, which fell -0.47%, Materials, which fell -0.43%, and Energy, which fell -0.25%. The top-performing subsectors were telecom, internet, and computer hardware. Meanwhile, soft drinks, precious metals, and banking were among the worst-performing subsectors. Northbound Stock Connect volumes were well above average. CNY and the Asia Dollar Index fell versus the US dollar. Government bonds sold off as yields increased slightly. Copper fell while steel rose.

Last Night's Performance

| Country/Index | Ticker | 1-Day Change |

|---|---|---|

| China (Hong Kong) | HSI Index | 4% |

| Hang Seng Tech | HSTECH Index | 6.5% |

| Hong Kong Turnover | HKTurn Index | 38.6% |

| HK Short Sale Turnover | HKSST Index | 40.1% |

| Short Turnover as a % of HK Turnovr | N/A | 13.9% |

| Southbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | 0 |

| China (Shanghai) | SHCOMP Index | 0.8% |

| China (Shenzhen) | SZCOMP Index | 1.6% |

| China (STAR Board) | Star50 Index | 6% |

| Mainland Turnover | .chturn Index | 24.8% |

| Nouthbound Stock Connect Net Buy/Sell (US $ Millions) | N/A | Not Available |

| Jing Daily China Global Luxury Index | CHINALUX Index | 1.5% |

| Japan | NKY Index | 0.3% |

| India | SENSEX Index | -0.6% |

| Indonesia | JCI Index | 0.2% |

| Malaysia | FBMKLCI Index | 0.8% |

| Pakistan | KSE100 Index | -0.7% |

| Philippines | PCOMP Index | 0.5% |

| South Korea | KOSPI Index | 0% |

| Taiwan | TWSE Index | 1% |

| Thailand | SET Index | 0% |

| Singapore | STI Index | 0.1% |

| Australia | AS51 Index | -0.3% |

| Vietnam | VNINDEX Index | 0.3% |

| MSCI China All Shares Index | # of Stocks | Average 1-Day Change (%) |

|---|---|---|

| Hong Kong Listed | 152 | 4.97 |

| Communication Services | 9 | 5.83 |

| Consumer Discretionary | 30 | 7.89 |

| Consumer Staples | 13 | 0.21 |

| Energy | 7 | -0.94 |

| Financials | 23 | 1.12 |

| Health Care | 13 | 6.14 |

| Industrials | 19 | 2.05 |

| Information Technology | 10 | 5.96 |

| Materials | 10 | -0.56 |

| Real Estate | 6 | 1.57 |

| Utilities | 12 | -0.77 |

| Mainland China Listed | 432 | 1.23 |

| Communication Services | 9 | 5.26 |

| Consumer Discretionary | 31 | 1.44 |

| Consumer Staples | 27 | 0.57 |

| Energy | 16 | -0.26 |

| Financials | 63 | 0.25 |

| Health Care | 40 | 1.28 |

| Industrials | 69 | 0.99 |

| Information Technology | 85 | 4.37 |

| Materials | 68 | -0.44 |

| Real Estate | 7 | 0.55 |

| Utilities | 17 | -0.48 |

| US & Hong Kong Dually Listed | Ticker | 1-Day Change (%) |

|---|---|---|

| Tencent HK | 700 HK Equity | 6.2 |

| Alibaba HK | 9988 HK Equity | 14.6 |

| JD.com HK | 9618 HK Equity | 5.1 |

| NetEase HK | 9999 HK Equity | 1.2 |

| Yum China HK | 9987 HK Equity | -0.1 |

| Baozun HK | 9991 HK Equity | 7.2 |

| Baidu HK | 9888 HK Equity | 4.7 |

| Autohome HK | 2518 HK Equity | -3.3 |

| Bilibili HK | 9626 HK Equity | 16.5 |

| Trip.com HK | 9961 HK Equity | 0.1 |

| EDU HK | 9901 HK Equity | 1.1 |

| Xpeng HK | 9868 HK Equity | 5.5 |

| Weibo HK | 9898 HK Equity | 8.9 |

| Li Auto HK | 2015 HK Equity | 7.4 |

| Nio Auto HK | 9866 HK Equity | 4.6 |

| Zhihu HK | 2390 HK Equity | 8.3 |

| KE HK | 2423 HK Equity | 4.5 |

| Tencent Music Entertainment HK | 1698 HK Equity | 1.1 |

| Meituan HK | 3690 HK Equity | 3.8 |

| Hong Kong's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| ALIBABA GROUP HOLDING LTD | 14.6 |

| TENCENT HOLDINGS LTD | 6.2 |

| XIAOMI CORP-CLASS B | 5.2 |

| MEITUAN-CLASS B | 3.8 |

| SEMICONDUCTOR MANUFACTURING | 7.9 |

| KUAISHOU TECHNOLOGY | 7.4 |

| HONG KONG EXCHANGES & CLEAR | 7.1 |

| BYD CO LTD-H | 4.6 |

| CHINA MOBILE LTD | 3 |

| LENOVO GROUP LTD | 15.4 |

| Shanghai and Shenzhen's Most Heavily Traded by Value | 1-Day Change (%) |

|---|---|

| EAST MONEY INFORMATION CO-A | 3.3 |

| ZTE CORP-A | 9 |

| TALKWEB INFORMATION SYSTEM-A | 10 |

| IEIT SYSTEMS CO LTD-A | 6.9 |

| DHC SOFTWARE CO LTD -A | 1.7 |

| SEMICONDUCTOR MANUFACTURIN-A | 4.8 |

| HYGON INFORMATION TECHNOLO-A | 15.3 |

| CAMBRICON TECHNOLOGIES-A | 20 |

| CHINA UNITED NETWORK-A | 10 |

| HANGJIN TECHNOLOGY CO LTD-A | -5.7 |

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.26 versus 7.26 yesterday

- CNY per EUR 7.60 versus 7.58 yesterday

- Yield on 10-Year Government Bond 1.72% versus 1.69% yesterday

- Yield on 10-Year China Development Bank Bond 1.73% versus 1.70% yesterday

- Copper Price -0.05%

- Steel Price +1.05%